Received 31 January 2022; Revised 20 May 2022, 10 June 2022; Accepted 20 June 2022.

This is an open access paper under the CC BY license (https://creativecommons.org/licenses/by/4.0/legalcode).

Mari Avarmaa, PhD, Senior Lecturer, Head of Department, TalTech School of Business and Governance, Department of Business Administration, Akadeemia tee 3, Tallinn 12618, Estonia; e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

Lasse Torkkeli, PhD, Visiting Researcher, TalTech School of Business and Governance, Department of Business Administration, Akadeemia tee 3, Tallinn 12618, Estonia Principal Lecturer, LAB University of Applied Sciences, Yliopistonkatu 36, 53850 Finland ; e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

Laivi Laidroo, PhD, Associate Professor, TalTech School of Business and Governance, Department of Economics and Finance, Akadeemia tee 3, Tallinn 12618, Estonia; e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

Ekaterina Koroleva, MA, Doctoral Student, TalTech School of Business and Governance, Department of Business Administration, Akadeemia tee 3, Tallinn 12618, Estonia; e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

Abstract

PURPOSE: The purpose of this study is to investigate the role of actors and ecosystem conditions in the development of the FinTech ecosystems in Tallinn and Moscow. METHODOLOGY: The study develops a framework for investigating entrepreneurial ecosystems, combining ecosystem actors with ecosystem conditions. The framework is implemented through a comparative case study of FinTech ecosystems in Tallinn and Moscow, with data drawn from 35 semi-structured interviews and processed by means of thematic analysis. The primary data is supplemented with data from secondary sources. FINDINGS: The findings show how the ecosystem conditions and actors are interdependent in the FinTech ecosystems. Tallinn is an example of a strong entrepreneurial culture with its small market, advanced technological infrastructure, and talent, which leads to the dominance of the FinTech start-ups and the emergence of an active FinTech cluster organization. In Moscow, the institutional context, concentration of financial capital, and its large home market with a loyal customer base limit start-ups’ ability to grow and form the ecosystem. IMPLICATIONS: The study contributes to the literature on entrepreneurial ecosystems and emerging technologies by integrating the streams of research on entrepreneurial ecosystems and FinTech ecosystems, combining FinTech actors with entrepreneurial ecosystem conditions. It also highlights the implications of variations of entrepreneurial culture, characteristics of the domestic demand and formal institutions in the development of ecosystems. It demonstrates that ecosystem conditions are likely to contribute to the emergence of the dominant actor in a particular ecosystem. Our results also suggest that when aiming to develop the FinTech ecosystem in a city, the support given to FinTech cluster organizations is essential. Facilitating university–industry cooperation through the cluster organizations or direct partnerships can contribute to the development of FinTech ecosystems. ORIGINALITY AND VALUE: To our knowledge, this is the first study to illustrate how specific entrepreneurial ecosystem conditions lead to configurations with different types of ecosystem actors, and to illustrate how specific ecosystem conditions impact the way in which actors develop and operate and how the ecosystem configuration is structured. These have been notable omissions in extant entrepreneurial ecosystem research until now. The present study also illustrates sectoral variations in entrepreneurial ecosystems while highlighting the distinct features of emerging ecosystems. It also contributes to the emerging literature on FinTech ecosystems through a comparative empirical perspective, thereby enhancing understanding of local conditions necessary for developing and maintaining FinTech ecosystems in different contexts.

Keywords: FinTech, financial technology, entrepreneurial ecosystem, FinTech actors, ecosystem elements

INTRODUCTION

The 2008 global financial crisis, accompanied by mistrust of the banking industry, the rapid evolution of technology, and the related general shift of consumer behavior, paved the way for the emergence of FinTech (Arner, Barberis, & Buckley, 2015; Mohan, 2020; Wójcik, 2021). The term “FinTech” encompasses a combination of finance and technology, carrying a broad range of definitions in academic and popular literature (see reviews by Giglio, 2022; Milian, Spinola, & Carvalho, 2019; Sun, Li, & Wang, 2022). It is often understood as applying modern technologies, such as the Internet, mobile computing, and data analytics, to enable, innovate, or disrupt financial services. (Gimpel, Rau, & Röglinger 2018; Gomber, Koch, & Siering 2017) Some authors treat FinTech as a whole sector – a new financial industry that applies technology to improve financial activities (Schueffel, 2016). Alternatively, the term is used to denote companies, mainly start-ups, combining finance and modern technology (Dorfleitner, Hornuf, Schmitt, & Weber, 2017; Pushmann, 2017). To encompass the mentioned definitions, in the current paper FinTech is defined as “a set of innovations and an economic sector that focus on the application of recently developed digital technologies to financial services” Wójcik (2021, p. 3). A FinTech ecosystem is a combination of FinTech actors and entrepreneurial ecosystem5 elements or ecosystem conditions, in line with Stam (2015).

The emergence of the FinTech phenomenon has brought along a remarkable amount of research (for literature review, see Iman & Tan, 2020; Kavuri & Milne, 2019; Milian et al., 2019; Takeda & Ito, 2021). As digitalization has enabled FinTech start-ups to penetrate the financial services market, it is necessary for scholars to clarify the competitive and collaborative dynamics of the various actors in FinTech (Alaassar, Mention, & Aas, 2021; Gazel & Schwienbacher, 2021; I. Lee & Shin, 2018). As a response, the FinTech ecosystem concept has recently been introduced to FinTech studies. Efforts to conceptualize FinTech ecosystems started with the model suggested by I. Lee and Shin (2018), concentrating on FinTech actors and their interrelations that has been used as a basis for several empirical studies (Castro, Rodrigues, & Teixeira, 2020; Svensson, Udesen, & Webb, 2019; Zhang-Zhang, Rohlfer, & Rajasekera, 2020). However, the mentioned model lacks a theoretical basis and is limited to describing the actors of a FinTech ecosystem. While the promise of the entrepreneurial ecosystem (EE) framework for studying Fintech has been noted lately (Wójcik, 2021), studies on the topic have also focused mainly on actors rather than the contextual elements of the ecosystem (Alaassar et al., 2021) or on single events such as Brexit (Sohns & Wójcik, 2020). While Alaassar et al. (2021) used the EE concept to observe the interactions between FinTech start-ups and other ecosystem actors, the interplay between ecosystem conditions and actors still requires further scrutiny (Iman & Tan, 2020). As calls have been made for international comparative case studies on FinTech (Kavuri & Milne, 2019), and emerging FinTech ecosystems (Muthukannan, Tan, Gozman, & Johnson, 2020) specifically, the purpose of this study is to investigate the role of actors and ecosystem conditions in the development of the FinTech ecosystem in Tallinn and Moscow. Although the study maps the status of these FinTech ecosystems in 2020, the analysis reflects developments over a longer time period leading up to that moment.

The findings show how EE conditions of domestic demand, entrepreneurial culture, talent, knowledge, institutions, and infrastructure, are interrelated with the role of FinTech actors, fostering or inhibiting the development of ecosystems. Through these results, the present study contributes to the emerging EE and FinTech literature in several ways. First, while extant literature has focused on start-ups (e.g., Alaassar et al., 2021), we show how specific ecosystem conditions can lead to configurations where other types of actors are dominant. Second, we illustrate how EE conditions, such as culture, demand and institutions, impact how certain actors develop and operate and how the ecosystem configuration is structured. Third, the present study adds to the understanding of sectoral variations in EEs while highlighting distinct features of emerging ecosystems, such as insufficient finance, minor role of universities and accelerators. Fourth, the present study develops a framework for investigating ecosystems merging the two lines of research on FinTech ecosystems, combining FinTech actors with EE conditions. We also contribute to the empirical studies of FinTech ecosystems (Alaassar et al., 2021; Hendrikse, van Meeteren, & Bassens, 2020; Muthukannan, Tan, Chian Tan, & Leong, 2021; Muthukannan et al., 2020; Sohns & Wójcik, 2020) through comparative empirical analysis with data from Estonian-Russian perspectives, thereby enhancing the understanding of local conditions necessary for increasing the likelihood of developing and maintaining an emerging FinTech ecosystem.

The rest of the paper is organized as follows. The second section explores the literature on entrepreneurial ecosystems and the FinTech phenomenon, leading to the analytical framework for the current study. The third section of the paper proceeds to explain the design of the study, research methods of data collection and analysis. The fourth and fifth sections summarise and discuss the findings of the comparative case study.

LITERATURE REVIEW

Literature has defined an ecosystem as “an interdependent network of self-interested actors jointly creating value” (Bogers et al., 2019, p. 1). Originating from natural sciences, the ecosystem concept has a growing significance in the field of business studies (Audretsch, Cunningham, Kuratko, Lehmann, & Menter, 2019; Tsujimoto, Kajikawa, Tomita, & Matsumoto, 2018; Vlados & Chatzinikolaou, 2019), considering it from a wide range of perspectives, such as networks (Rosenbloom & Christensen, 1994), platforms (Cusumano & Gawer, 2002) or multi-sided markets (Evans, 2003). The EE perspective provides a theoretical framework for analyzing the underlying dynamics of how new venture formation occurs and is more plentiful and growth-oriented in certain geographical locations than others (Brown & Mason, 2017). Some of the main characteristics of the EE concept is the centrality of the entrepreneur as the key actor (Auerswald & Dani, 2017; Spigel & Harrison, 2018; Stam, 2015), the focus on networks and linkages (Auerswald & Dani, 2017), the importance of entrepreneurial processes and ability to access resources (Sarma & Marszalek, 2020; Spigel & Harrison, 2018), the cross-industry nature (Auerswald & Dani, 2017; Spigel & Harrison, 2018), and the role of social and economic contexts surrounding entrepreneurial processes (Nicotra, Romano, Del Giudice, & Schillaci, 2018). Application of the EE concept to FinTech is useful in acknowledging the broader ecosystem where FinTech actors belong and paying attention to the influence of the ecosystem elements. However, due to the centrality of venture creation, there might not be a sufficient focus on the dynamics related to other actors, such as financial institutions.

Empirical research on FinTech ecosystems has emerged only recently and remains in its infancy (Basole & Patel, 2018; Zhang-Zhang et al., 2020). Most studies have focused on a single ecosystem, investigating a specific aspect or component of the ecosystem (Wójcik, 2021). There is a set of studies investigating the impact of certain policy initiatives or political events on a FinTech ecosystem (Hendrikse et al., 2020; Muthukannan et al., 2020; Sohns & Wójcik, 2020). Another stream of empirical research focuses on FinTech ecosystems built around one or two companies (Leong, Tan, Xiao, Tan, & Sun, 2017; Zhang-Zhang et al., 2020). Some research (Basole & Patel, 2018; Muthukannan et al., 2020) also deals with FinTech ecosystems that operate on a global scale. The geographical scope of studies has often been limited to a single ecosystem, e.g., Singapore, Brussels, London, or Sweden (Alaassar et al., 2021; Hendrikse et al., 2020; Sohns & Wójcik, 2020; Svensson et al., 2019). There are also a few studies on FinTech ecosystems relying on empirical data from several countries (e.g., Castro et al., 2020; Palmié, Wincent, Parida, & Caglar, 2020). While these developments in empirical research on FinTech ecosystems are promising, they tend to focus on a single ecosystem, a specific component, intervention or initiative, without paying sufficient attention to its overall composition and interactions.

Two main types of frameworks have been used in the studies on FinTech ecosystems. One set of studies (Castro et al., 2020; Hendrikse et al., 2020; Svensson et al., 2019; Zhang-Zhang et al., 2020) focuses on FinTech actors and their roles and interrelations, relying on the prominent FinTech ecosystem model proposed by I. Lee and Shin (2018) or creating similar models of their own. While such focus on actors is crucial to understand the functioning and specifics of a FinTech ecosystem, earlier models tend to both neglect the context in which the actors operate and lack a theoretical foundation. The second set of studies (Alaassar et al., 2021; Sohns & Wójcik, 2020) applies frameworks utilized in entrepreneurship research (Brown & Mason, 2017; Isenberg, 2011; Spigel, 2017; Stam, 2015), where an ecosystem refers to a set of interdependent actors and factors that are governed in such a way as to enable productive entrepreneurship (Stam, 2015). This approach enables to observe not only FinTech actors but also contextual elements, such as culture, market, infrastructure, and human capital.

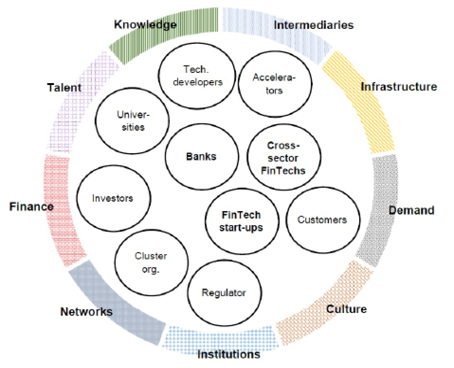

In developing our framework, we combine the FinTech ecosystem models consisting of actors with the ecosystem elements provided by the literature on EEs (Brown & Mason, 2017; Isenberg, 2011; Spigel, 2017; Stam, 2015). The approach of linking FinTech actors and EE conditions is supported by the findings of Spigel (2022) that well-developed FinTech ecosystems tend to benefit from linkages with the general EE, and the results of Harris (2021) that the FinTech ecosystem has emerged from the broader EE and is heavily interlinked with the latter, with actors benefiting from both ecosystems. Our framework (see Figure 1) is constructed as follows: ten main actors constitute the core of the FinTech ecosystem model, surrounded by nine EE conditions. We adapt and extend the model proposed by I. Lee and Shin (2018) as the basis for constructing our ecosystem framework, to achieve comparability with previous FinTech ecosystem studies and to consider a broad set of core actors Figure 1.

Following Castro et al. (2020) and Alaassar et al. (2021) we consider investors placed under financial institutions by I. Lee and Shin (2018) as a separate actor due to their strategic role. For clarity, we refer to the traditional financial institutions as “banks” and to the item “government” as “regulator,” as FinTechs need to be in close dialogue with regulators to ensure the survival and sustainable development of their services. The “regulator” component also encompasses the role of the financial supervisory authority in the framework. In addition to FinTech-specific regulations, there are general elements of legislation, such as the tax incentives or procedures for starting a business that form the policy conditions for all start-ups (Nicotra et al., 2018). We consider the general role of government under “institutions,” which is one of the conditions of EE.

We include four additional actors compared to the model of I. Lee and Shin (2018). Sheriff and Muffatto (2018) include universities in their model of high-tech ecosystems as those provide the talent pool, develop technologies, and transfer knowledge beyond academic borders, confirmed by empirical results of Lai and Vonortas (2019) on China. Accelerators are added based on the empirical results of Alaassar et al. (2021), who find accelerators to serve as intermediaries for various actors in the FinTech ecosystem in Singapore, and Harris (2021) documenting the significant role of accelerators in the development of the FinTech ecosystems in London and Singapore. In line with Berg, Novak, Potts, and Thomas (2018), we include cluster organizations and, following Zhang-Zhang et al. (2020), we include cross-section FinTechs among the actors. Relying on the EE literature (Alvedalen & Boschma, 2017) and previous studies on FinTech (Harris, 2021; Zhang-Zhang et al., 2020), we place FinTech start-ups, banks and cross-section FinTechs in the centre of the framework as the main providers of FinTech services.

Figure 1. A framework of FinTech actors and ecosystem conditions developed based on literature

EE conditions are introduced from EE frameworks by Stam (2015) and Stam and van de Ven (2021), which have been used in several recent empirical works (e.g., Laidroo, Koroleva, Kliber, Rupeika-Apoga, & Grigaliuniene, 2021; Leendertse, Schrijvers, & Stam, 2021). We include the nine conditions of the latter framework – infrastructure, demand, intermediaries, talent, knowledge, finance, institutions, culture, and networks. We merge the element of leadership with culture due to the strong interrelation of role models, visible entrepreneurial leaders and the degree to which entrepreneurship is valued in a society. While Sohns and Wójcik (2020) incorporate the four EE elements most relevant in the context of Brexit in their study, we chose to cover all elements to provide a more comprehensive framework. In what follows, we apply the framework to two ecosystems, examining the interaction between actors and conditions.

METHODOLOGY

Research design

The case study method has been prevalent in prior studies of FinTech ecosystems (Hendrikse et al., 2020; Muthukannan et al., 2020; Sohns & Wójcik, 2020). This research approach is apt when investigating understudied phenomena (Halinen & Törnroos, 2005; Siggelkow, 2007), such as the FinTech ecosystem, its components and their interrelations. Case studies are particularly useful in understanding contextual conditions (Yin, 2018) and necessary to use a variety of lenses, such as the ones of entrepreneurs, bankers, representatives of government institutions, and other organizations, which allow the phenomenon’s multiple facets to be revealed (De Massis & Kotlar, 2014).

Most authors tend to take the view that ecosystems should be analyzed on a regional or local level (Audretsch & Belitski, 2017; Hakala, O’Shea, Farny, & Luoto, 2020; Leendertse et al., 2020; Velt, Torkkeli, & Saarenketo, 2018). In line with extant empirical works on FinTech ecosystems (Hendrikse et al., 2020; Sohns & Wójcik, 2020; Spigel, 2022), we investigate the FinTech ecosystem on the city level. The cities of Tallinn and Moscow provide a suitable setting for the comparative analysis. Despite their similar history, the countries that the capital cities represent (Estonia and Russia, respectively) present distinct contexts: while Estonia scores above EU averages in the quality of institutions (reflected in indices for the corruption perception, rule of law, government effectiveness, voice and accountability), Russia is somewhat behind (Laidroo et al., 2021). The different size of the countries serves as a good basis for observing the ecosystems geared towards serving one’s home market as opposed to going after the international customer base. The regulative frameworks are also different, as the EU financial regulatory framework applies in Estonia and developments in the area are driven by EU-wide initiatives (for a more detailed overview see Tirmaste, Voolma, Laidroo, Kukk, & Avarmaa, 2019). In Russia, the Central Bank carries out the role of both the regulator and supervisor (Claeys, 2005), initiating and supporting the main directions of the development of FinTech (Bank of Russia, 2018).

Based on the literature review and our preliminary framework of the FinTech ecosystem, a case study protocol was developed using the guidelines of Yin (2018). It contained objectives and research aims, data collection procedures, protocol questions, and the tentative outline of the analysis. Details on the data collection and analysis methods used are provided in the next section.

Data collection and analysis

Data collection occurred in two main phases—the preparatory phase and the fieldwork phase. The preparatory phase started in 2019 as a part of a project focusing on the analysis of the FinTech landscape in Estonia and the neighbouring countries. In the preparatory phase, data from macroeconomic and industry reports, articles in the press, and legislative documents concerning Estonia and Russia were analyzed to understand the background of the countries. We then concentrated on mapping the factors influencing the development of the FinTech sector in the two cities as well as getting an initial understanding of the level of development, composition and the main participants of the ecosystems. In this process, we also compiled a list of all FinTech companies in Tallinn and Moscow. The final list for Tallinn consisted of 111 start-ups identified, based on a critical review of data provided in Crunchbase, Funderbeam, Key Capital6, and FinanceEstonia databases as of the end of 2019. The list of FinTech companies in Moscow was collected from the official websites of banks, accelerators, associations, and RusBase7, and, after corrections, included 272 companies. All corrections to the initial lists were made to ensure that the companies fell under the definition used in this paper, and this list was used to select some of the interviewees in the fieldwork phase.

The fieldwork phase was based on semi-structured interviews to collect data specific to our research aims and explore the two FinTech ecosystems in depth. This approach enables us to gain an insight into opinions, attitudes, experiences, and predictions of ecosystem participants where existing knowledge of the subject is inadequate, and was also preferred since our potential interviewees are likely to be more receptive to interviews than other data collection methods (Rowley, 2012). The semi-structured interviews were performed with the representatives of the ecosystem actors, the list of interviewees is illustrated below in Table 1.

The interviewees were selected via purposive sampling. Interviewees from FinTechs were selected from the list of FinTechs, keeping in mind the diversity of respondents and the variety of FinTech types, sizes, and business models. Non-entrepreneur interviewees were selected based on input from secondary data sources. The interviewees were contacted via emails or social media accounts. Several respondents were added through the snowball method via referrals because of their expertise and involvement in the FinTech ecosystem. Out of 32 interview requests, 11 resulted in an interview in the case of “cold” contacts, while all 24 requests through referrals or personal contacts got a positive response.

Table 1. List of interviewees

|

Actor Category |

Position |

Participant Code |

|

|

Tallinn |

Start-up |

Founder/CEO |

E1 |

|

Start-up |

Founder/CEO |

E2 |

|

|

Start-up |

Founder/CEO |

E3 |

|

|

Start-up |

Manager |

E4 |

|

|

Start-up |

CEO |

E5 |

|

|

Start-up |

Founder/CEO |

E6 |

|

|

Start-up |

Founder/CEO |

E7 |

|

|

Start-up and Bank |

Industry expert |

E8 |

|

|

Start-up |

Founder/COO |

E9 |

|

|

Start-up |

Founder/COO |

E10 |

|

|

Start-up |

Founder/CEO |

E11 |

|

|

Bank |

Head of Department |

E12 |

|

|

Bank |

Head of Department |

E13 |

|

|

Regulatory/Supervisory Authority |

Specialist |

E14 |

|

|

Regulatory/Supervisory Authority |

Specialist |

E15 |

|

|

Regulatory/Supervisory Authority |

Head of Department |

E16 |

|

|

Cluster organization |

Board Member |

E17 |

|

|

Non-profit FinTech association |

Board Member |

E18 |

|

|

Venture Capital network |

Board Member |

E19 |

|

|

Moscow |

Start-up |

CIO |

R1 |

|

Start-up |

HR business partner |

R2 |

|

|

Start-up |

Deputy of CEO |

R3 |

|

|

Start-up |

CIO |

R4 |

|

|

Start-up |

Founder/CEO |

R5 |

|

|

Start-up |

CEO |

R6 |

|

|

Start-up |

CEO |

R7 |

|

|

Start-up |

COO |

R8 |

|

|

Start-up |

Founder/CEO |

R9 |

|

|

Start-up |

CFO |

R10 |

|

|

Bank |

Manager |

R11 |

|

|

Bank |

Head of Department |

R12 |

|

|

Accelerator/ Venture Capital fund |

Head of Department |

R13 |

|

|

Cluster organization |

Head of Department |

R14 |

|

|

Cluster organization |

Head of Department |

R15 |

|

|

Regulatory/Supervisory Authority |

Head of Department |

R16 |

In total, 35 interviews (19 in Tallinn and 16 in Moscow) were performed between May and September 2020. The age of the interviewees ranged from 24 to 59, with 26% of the respondents being female. Interviews took place either online or in person, depending on the availability of the interviewees, and lasted from 27 to 105 minutes. Several interviewees had multiple current or previous roles in banking, start-ups, regulatory bodies and/or representative organizations and were thus able to see the ecosystem from multiple perspectives.

A detailed interview guide following the guidance from Yin (2018) and relying on the example of Cukier and Kon (2018) was applied. The interview questions presented in Table 2 were developed based on our research aims and the developed framework. The interview questions were asked in a flexible order to allow for a higher level of detail and responsiveness. Interviews were carried out in Estonian, Russian or English, depending on the native language of the interviewee. All interviews were digitally recorded and transcribed. Thematic analysis was performed according to the guidelines of Braun and Clarke (2006) and Nowell, Norris, White, and Moules (2017), using the software package Nvivo. Interview transcripts were read, and sections of text from the informants coded based on our research aims and the elements of our initial ecosystem framework, resulting in first-order codes. Patterns within the first-order codes were then identified through an iterative process, which led to the development of broad second-order themes that were on a higher level of abstraction than the first-order codes. The coding was performed independently by two of the authors and differences were discussed and modified until a consensus was reached. The broad themes included the composition of the ecosystem, its level of development, cooperation and connectivity within the ecosystem, the role of the local demand, entrepreneurial culture, FinTech regulation, and human and financial capital in its development.

Table 2. Interview questions

|

The interview starts with warm-up questions on the background of the person and institution/company, followed by questions on the FinTech ecosystem: |

|

1. What are the drivers and reasons for the establishment of FinTech companies in our city? 2. What are the factors in Tallinn/Moscow that foster/promote the development of FinTech companies? What are the factors in Tallinn/Moscow that discourage/create barriers for FinTech companies? 3. In your opinion, does the FinTech ecosystem exist in Tallinn/Moscow? Why? 4. What are the institutional mechanisms in place in the region that promote antrepreneurship? 5. What is the culture in your region with respect to entrepreneurship? How does it contribute to the establishment of FinTechs? 6. How do the existing firms (banks, technology companies, others) contribute to the establishment and development of FinTechs? 7. How does the development of the local financial services market/customers contribute to the establishment and development of FinTechs? 8. How does the FinTech ecosystem look like? How would you describe it? 9. If you were requested to draw a FinTech ecosystem map/chart/schema, how would it look like? 10. What is the role of the FinTech ecosystem? Why does it exist? Why is it important? 11. How is the ecosystem led? Is there a leader of the FinTech ecosystem? Who? 12. What role do actors play in the ecosystem? If some actors in our preliminary model are not discussed, ask for additional input on their presence and roles. 13. How has the emergence of FinTech transformed your industry dynamics and the position of actors? 14. How do resources (knowledge/info, talent, funds, etc.) flow in the ecosystem? 15. To what extent is the FinTech ecosystem a geographical phenomenon, present in a specific location as opposed to a virtual phenomenon? Spatial concept or not? 16. If you had to name three key elements of a healthy FinTech ecosystem in a region, what would they be? What are the key success factors for FinTech ecosystems? 17. How successful is the FinTech ecosystem in your city, in your oponion? What are the reasons? What are the problems? |

RESULTS

The FinTech ecosystem in Tallinn: Actors and configuration

Overall, the FinTech ecosystem of Tallinn is seen as being present and functioning: “I truly believe that we are a part of the FinTech ecosystem, I really do. There are so many FinTech companies operating here, we participate in Money2020 and use the slogan “Join the Estonian FinTech revolution”” (E5); “I believe it exists, as there are some participants. Not hundreds, but several dozens for sure, some more and some less ambitious” (E6). The dominating view among the informants occurs to be that the FinTech ecosystem exists in some form, described as “unconscious,” “abstract,” “uncoordinated,” “personal” or “in its infancy.”

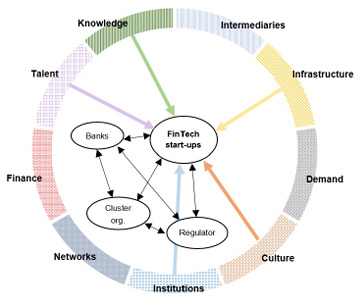

Several representatives of start-ups (E2; E8) likened the FinTech ecosystem to the EE as for them, it constitutes an informal network of technology-oriented entrepreneurs. When the interviewees were asked to bring out the leader of the ecosystem, most of them described the FinTech ecosystem in Tallinn as self-organizing rather than led by any particular actor. At the same time, FinTech start-ups are considered the most central participant in the ecosystem (see Figure 2). Some respondents say explicitly that the ecosystem is needed mainly for start-ups in their early stages of development (E12; E7; E9). The focus on start-ups is also confirmed by the view of bank representatives, who do not perceive the existence of a local ecosystem due to the smallness of the economy (E12; E13) or are not considering themselves as part of the ecosystem (E8).

Figure 2. Tallinn FinTech ecosystem

According to most non-bank actors, banks participate in the Tallinn ecosystem, but their role is rather secondary. Some start-ups perceive the largest foreign-owned banks as uninterested in developing the ecosystem due to their monopolistic position and foreign background (E1). Their restrictive banking practices, often dictated by the headquarters, are believed to pose a major obstacle to foreign founders establishing start-ups in Estonia (E11). On the contrary, one bank representative explains that although they initially saw FinTechs as a threat, they have opened up to cooperation over the past five years, welcoming FinTechs under their roof and providing venture capital (E12). Both bankers (E12) and start-ups (E3) pointed out that incumbent banks tend to be dependent on their legacy systems and time-consuming procedures that might limit their ability to cooperate on minor add-on applications. The major locally owned bank LHV was regarded as the most open to cooperation, for instance, through a well-functioning API and the integration of ready-made FinTech solutions (e.g., payments, verification) to their customers (E13; E10).

Data suggest that Tallinn has a strong FinTech section under FinanceEstonia, a cluster organization of the financial sector, facilitating connectivity in the ecosystem. Some respondents liken it to an ecosystem since it includes the main actors, such as banks, FinTechs, financial supervisor, regulator, and providers of support services; a few others consider it the leader of the FinTech ecosystem. Run and financed by its members, the main function of FinanceEstonia is representing participants’ interests towards regulators, as well as coordinating efforts to enter foreign markets. According to its members, the organization is necessary to ensure that the voices of the many small players can be heard, gain visibility and have negotiation power (E9).

Participants consider regulatory and supervisory authorities, marked as “regulator” in our framework, a crucial actor in the local FinTech ecosystem. The interviews showed that the role of regulators in creating a supportive environment while securing transparency and protection of participants’ rights is key to the development of the ecosystem. As one entrepreneur (E1) stressed, you cannot perform any innovation in the financial sector without coordinating this with the regulator, as regulation is the main shaper of the FinTech ecosystem. There are contradictory views on the impact of the regulatory and supervisory activities in Estonia. Some participants do not see regulation as a major obstacle (E17), while others consider it a major barrier. “In general, the Estonian financial sector regulation is a copy-paste from the EU, while in our country there is a tendency to be stricter in its enforcement and this limits abilities to innovate and take some business risks” (E3).

According to ecosystem actors, stronger cooperation between the regulator, supervisor and other market participants would speed up the alleviation of regulatory challenges of start-ups and enable Estonia to be the forerunner of FinTech internationally. “So, it’s kind of like all the pieces are there, but it seems to me that there is proximity with everybody, except with the Finance Minister’s office, the Financial Intelligence Unit, the Financial Supervisory Authority (FSA) and the banking sector. For some reason, they cannot communicate with each other, but everybody else can. I think they need to break down those walls” (E11).

The findings also suggested that several of the actors of our initial FinTech framework were not considered to be a part of the Tallinn ecosystem or were viewed to be loosely connected with the rest of the ecosystem. Technology developers were omitted since FinTech services tend to be built on relatively mainstream technologies, universities were mainly viewed as a provider of human capital, investors and accelerators lack specialization in FinTechs. Some interviewees pointed out the current underutilization of opportunities for industry–university cooperation and the related knowledge transfer (E12, E4). FinTechs expect universities to take a more proactive role in proposing marketable technologies to the industry as well as in the communication of research results.

The FinTech ecosystem in Tallinn: Ecosystem conditions and interplay with actors

According to the findings, the FinTech ecosystem in Tallinn is rooted in the entrepreneurial culture in Estonia, triggering the dominant role of start-ups in the ecosystem. The emergence of FinTech start-ups has been driven by the general entrepreneurial spirit and acceptance of risk-taking in society, as well as some early success stories and role models (E3; E8; E10). Success stories both inspire start-ups and help pave their way internationally. As an interviewee (E8) illustrated, “You constantly need success stories for the ecosystem to be successful, otherwise you are like the Eagles who plays Hotel California thirty years in a row and are still happy.” The interviewee also explained that successful entrepreneurs wish to invest capital in similar ventures where they understand the business and are ready to take high risks. The early success of technology start-ups has underpinned the creation of technological knowledge that is a key component in the development of FinTech services (E10; E13; E17).

Talent was also a key condition contributing to the development of FinTech start-ups in Tallinn. As several interviewees explained, strong technological skills, high financial literacy, as well as the availability of specialists and leaders with financial experience have supported the establishment and development of FinTech ventures. Hansapank, a local bank established in the early 1990s, now foreign-owned, has been a source of knowledge, talent, and capital (E8; E17). While Estonia has produced high-quality technological talent through serial entrepreneurship and the country stands out with its financial and IT literacy (Trabskaja & Mets, 2019), it has reached the stage where some start-ups face scarcity and an increasing cost of talent and struggle with bringing in key specialists, such as developers, engineers, product managers and designers from abroad (E2; E7). To overcome the shortage, some start-ups also use remote employees (FinanceEstonia, 2020).

Estonia’s small size is viewed as both an advantage and liability of the FinTech ecosystem in Tallinn. The liability of smallness is characterized by the limited domestic demand and scarcity of resources (Yamamura & Lassalle, 2020). As several participants explained, FinTech services, such as payments or crowdfunding, require a large scale to succeed (E1). Due to the limited local demand and a concentrated banking sector, most start-ups have the scalability to other markets in mind from the very beginning and therefore focus on adaptability in the early stages of development. Start-ups with a substantial home market might learn about the different needs and requirements of international markets at a later stage when it is costlier to modify and adapt. As several participants (E4; E17) explained, with its small scale and financially and technologically savvy customers, Estonia is a suitable platform for experimentation and a direct passage to the entire EU market. To access large multinational companies, one generally needs to have good connections in the US (E9). Due to the centrality of international markets, start-ups see a need for strengthening coordinated international sales efforts (E3, E10).

Despite the strong international focus, start-ups mostly consider the FinTech ecosystem in Tallinn a location-specific phenomenon due to the importance of interactions, interpersonal ties, and concentration of knowledge. The relatively small capital market is associated with the limited availability of financing for FinTechs. The small circle of venture capital investors is approached by almost every start-up founder (E3) and opportunities for raising capital are much broader elsewhere, for instance, in London (E7). Thus, while Tallinn is considered a good location to establish a FinTech, several entrepreneurs highlighted the need to move to a major financial hub in the next phases to be closer to the capital and earn credibility. Several start-ups have experienced pressure from foreign investors to move the legal headquarters to the US or UK after a successful round of funding due to legislative reasons (E4) or to eliminate country risk (E17). The lack of a critical mass of start-ups was also mentioned as a limitation in the context of establishing a regulatory sandbox (E16).

Most participants highlighted the central role of the general digital and technological leadership with its advanced infrastructure and institutions in Estonia as one of the drivers for the establishment of FinTechs and success of the ecosystem in Tallinn. Residents’ digital identity and e-government solutions were often mentioned as distinctive elements of the infrastructure (E12; E15, E16). Also, the ease of doing business and a relatively simple tax system attract entrepreneurs (E1; E6; E15). While developing and enforcing legislation to support and facilitate innovation is considered a general challenge for the financial sector in Europe (E3, E4), start-ups in Tallinn see a need to consider how rigorously the legislation needs to be enforced locally (E3). Due to its small size, Estonia could be the forerunner in the regulation to support the development of the FinTech sector (E2). Several participants (E6, E12) have raised the need to proceed with the regulatory sandbox initiatives, yet, in its discussions with market participants, the FSA has experienced low interest towards the classical sandbox as a testing environment (E16).

All in all, there is a start-up-centric FinTech ecosystem, relying on a strong entrepreneurial culture, talent, and technologically advanced infrastructure and institutions present in Tallinn, facilitated by an active cluster organization. The small size of the economy enforces networking and agility of the ecosystem, while putting strong pressure on internationalization and calling for coordinated policy efforts.

The FinTech ecosystem in Moscow: Actors and configuration

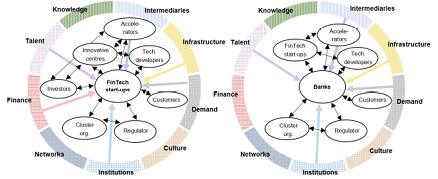

Since 2015, the participants of the financial sector in Russia, based mainly in Moscow, have aimed to establish a joint FinTech ecosystem through a constructive dialogue. Initiatives have been reflected in numerous negotiations and forums (Bankir.Ru, 2015; Finnopolis, 2016; Banking Review, 2016) and in the foundation of associations and innovation centres operating in Moscow. According to our study, the efforts to create a FinTech ecosystem have not succeeded due to the unaligned interests of the main actors. The data suggest that there is a loosely formed general FinTech ecosystem as well as two alternative configurations of nested ecosystems observed in Moscow (see Figure 3).

Figure 3. Moscow FinTech ecosystem: the nested ecosystem supporting FinTech start-ups (left) and banks’ private ecosystem (right)

First, the “private” ecosystems of most of the systematically important banks (Sber, VTB Bank, Tinkoff), consisting of start-ups, accelerators, and technology developers. The major banks acknowledge the need to provide state-of-the-art services to their consumers and therefore invest in start-ups. In the case of facing obstacles to entering the market and having limited development opportunities, start-ups benefit from participating in a bank-centred ecosystem by accessing the necessary resources. According to the opinion of the representative of start-ups (R1), “banks ensure the reliability of the start-up and thereby attract new consumers to its services.” The position of banks can be described as the Appleisation of finance (Hendrikse, 2018), whereby incumbents aim to transform legacy systems into integrated platforms, cultivating ecosystems where start-ups are “free” to compete whilst effectively being locked into the bank’s orbit. The configuration contrasts with the empirical findings of Hornuf, Klus, Lohwasser, and Schwienbacher (2021), indicating that banks in Canada, France, the UK, and Germany tend to cooperate with FinTechs through alliances rather than acquisitions. Second, the nested ecosystem gathered around the innovation cluster that supports start-ups established without the involvement of a major bank. There is a special competence centre of FinTech and blockchain in the Skolkovo innovation centre near Moscow. Start-ups observe a stronger trust of consumers in the members of Skolkovo in comparison with other start-ups (R2).

The dominance of bank-driven nested ecosystems is considered a reason for the lack of a well-functioning FinTech ecosystem in Moscow. As one respondent put it: “Start-up founders in Moscow tend to take a short-term view – creating a FinTech, attracting a bank, and selling the start-up to the bank” (R2). The position of banks is believed to hinder cooperation in the ecosystem: “It is extremely difficult to establish a constructive dialogue due to the importance of banks in the FinTech ecosystem in Moscow. This allows banks to impose their policies” (R9).

Most of the respondents consider the Central Bank, who acts both as a regulator and supervisor, not only a part but also the driver of the general FinTech ecosystem in Moscow. There are diverse views towards the activity of the Central Bank among respondents, depending on their area of activity. There are still areas (e.g., blockchain, cryptocurrency) with no specific regulation (Ermakova & Frolova, 2019). One respondent (R10) explained: “Innovations are usually in the grey zone of the regulator being not or poorly described in the legislation.” Thus, it is not always clear how to implement the technologies and draw up the relevant documentation. The actors of the FinTech ecosystem take a wait-and-see attitude: they wait for someone else to test the regulatory frameworks and their enforcement first. The uncertainty of regulation leads to start-ups registering abroad (e.g., Cyprus, US) to ensure the sustainability of their business (Remezova, 2010). One of the challenges of the FinTech ecosystem in Moscow is finding a regulatory approach that enables to intensify market competition and reduce barriers to entry to the market. Interviewees suggest directing the regulatory activities towards banks to promote healthy competition in the market and contribute to the development of the FinTech ecosystem in Moscow. The Central Bank recognizes the necessity of regulating new actors in the financial market and suggests testing possible decisions using the regulatory sandbox (Bloomchain, 2019).

The role of the FinTech cluster organizations reflects the bank-centred setup of the ecosystem. Cluster organizations view themselves as a part of the general FinTech ecosystem, acting as the facilitator of communication between different members of the ecosystem and the coordinator of improvements in the regulatory environment. The banks’ representatives brought out the difficulty of building an equal dialogue between the members of organizations and considering the interests of each type of actor in the ecosystem.

According to our interviews, in Moscow, local customers are believed to play a driving role in the ecosystem, unlike Tallinn. For instance, (R1) explained: “Well, the first reason [for the emergence of the FinTech ecosystem] is the demand of consumers for services and the further development of technologies in finance”. One respondent (R6) mentioned: “Consumers are interested in new, more convenient functionality of applications and look forward to new offers from actors of the FinTech ecosystem”. The local customers provide the necessary demand for the development of services and fuel the evolvement of the FinTech ecosystem.

Although technology developers do not tend to be specialized in FinTech, start-ups consider them critical actors in the FinTech ecosystem by providing crucial developments that form a basis for products. Technology developers do not see their role in the ecosystem as FinTech is just one of the areas where their insight is used. Universities are not considered a part of the ecosystem since formal education is perceived as irrelevant in the FinTech area. Some respondents pointed out the low level of entrepreneurship education in Russia and emphasized the importance of obtaining additional skills for establishing start-ups through specialized courses or webinars. Cross-sectional FinTechs are not present in the ecosystem and not perceived by the actors.

The FinTech ecosystem in Moscow: Ecosystem conditions and interplay with the actors

As mentioned in the previous sub-chapter, the high home demand with relatively sophisticated customers is one of the main conditions driving the development of the FinTech services in Moscow. Due to the highly competitive banking market, large banks have been in search of ways to lock in their customer base and the ecosystem strategy has been designed for this purpose. As a banker (R12) describers: “It is becoming increasingly difficult for banks to compete for customers. Most players have similar rates for the same products and services. It seems that the solution was found in the ecosystem approach. We get a client, create a comfortable environment and seemingly there are endless opportunities for creativity and growth.” Advanced physical infrastructure with widespread high-quality Internet is believed to be another key condition for the development of the FinTech services in Moscow, supporting the home demand (R1).

The data suggest that regulatory activities are quite effective in regard to banks while regulation lags behind when it comes to financial innovations, thus creating uncertainties for the potential investors in FinTech (R10). Most accelerators, venture funds and innovation centres in Moscow are state-owned or supported by state grants and state programs (R12, R13) to compensate for the low interest of private entities. One entrepreneur (R6) noted that the increasing role of the government in the development of the FinTech ecosystem is further eroding the private sector. This resonates with the empirical findings of Keogh and Johnson (2021) that start-ups in the US financed by a government source have the highest likelihood of failure. The institutional aspects in Moscow also inhibit international activities – according to one entrepreneur (R4), Russia has a poor political reputation abroad, reflected in various sanctions and restrictions, thus leading to negative consequences for the FinTech sector.

The central role of banks in the Moscow ecosystem is reinforced by the lack of financial capital available for start-ups. Only a few venture capital funds invest in FinTech start-ups (Skolkovo Ventures, Digital Horizon, Sailing Start-up, Starla Capital, and Sberb CIB). In the words of a representative of a VC fund (R13), “the venture capital market in Russia is dead”. Moreover, Russian investors often reorient to foreign markets due to legal insecurity (R4). Therefore, start-up founders are forced to turn to banks.

Talent is a condition functioning both as a driver and a barrier to the development of the FinTech ecosystem in Moscow. As one interviewee (R12) explained, largely thanks to the IT-skilled workforce and advanced technological knowledge, especially in the development of interfaces and support systems, Russia is far ahead of Europe in the diversity of financial services. According to one entrepreneur (R1), the strong IT sector in Moscow is the main source of technological knowledge for FinTechs. However, the lower salary level of IT specialists compared to some other locations in Europe poses a threat to the development of the FinTech ecosystem, and entrepreneurial skills in Moscow are lagging behind: the founders struggle with presenting their business ideas, developing a business plan, assessing risks, attracting potential investors, registering a company, as well as making informed management decisions (R15). One respondent (R12) described the mix of skills from an interesting angle: “In Russia, a FinTech start-up with a poorly developed idea and a beautiful interface is more likely to be launched than a FinTech start-up with a well-thought-out idea and an irrelevant interface.” An interviewee (R2) pointed out that the lack of managerial skills and the short-term profit orientation of the founders of FinTech start-ups result in a high failure rate.8 Thus, entrepreneurial talent might also be a condition that has enforced the ecosystem configuration where banks dominate over start-ups. Our interviews provided no evidence of the presence of entrepreneurial culture or role models for FinTech start-ups in Moscow, also explaining the structure of the FinTech ecosystem.

Overall, the FinTech scene in Moscow is fragmented, consisting of strong banks’ ecosystems relying on a loyal customer base, ample financial resources, and institutional support, and less developed ecosystems organized around innovation centres serving FinTech start-ups. The ecosystem development is driven by a large local market and technologically skilled workforce and shaped by a dominating Central Bank.

DISCUSSION

The aim of the study was to investigate the role of actors and ecosystem conditions in the development of the FinTech ecosystems in Tallinn and Moscow. Applying our developed framework, Table 3 illustrates FinTech ecosystems in Tallinn and Moscow, showing that the composition of the FinTech ecosystem in each city is unique, with the EE conditions in each location eliciting diverging configurations and roles of actors. Tallinn is an example of an ecosystem evolving around a community of FinTech start-ups, routed in the strong ecosystem conditions of entrepreneurial culture, talent and technological infrastructure. Such entrepreneur-centred ecosystems are complex and self-organizing systems where entrepreneurs are dependent on and collaborate with many other actors (Fredin & Lidén, 2020; Sheriff & Muffatto, 2018). In Moscow, on the other hand, major banks, which relish a large local customer base, have created their own ecosystems that dominate over the ecosystem serving the FinTech start-ups, and there is no unified FinTech ecosystem observed in the city. Our evidence shows that the propositions of Alaassar et al. (2021) are valid for Tallinn but not for Moscow, probably due to different ecosystem conditions.

Table 3. Observed ecosystems in comparison to the proposed framework

|

|

Component |

Tallinn |

Moscow |

|

Actors |

Start-ups |

Main actor, leader |

Secondary actor, participating in nested ecosystems led by banks or innovative centres |

|

Banks |

Secondary actor, not dominating or not an actor |

Main actor, leading its own private ecosystems |

|

|

Cross-sector FinTechs |

Not perceived as a participant |

Not perceived as a participant |

|

|

Investors |

Not specialized in FinTech |

Not specialized in FinTech, underrepresented |

|

|

Universities |

Inactive role |

Inactive role |

|

|

Technology developers |

Not participating |

Perceived as participants by banks and start-ups |

|

|

Regulator |

Key actor |

Key actor, leader |

|

|

Accelerators |

Not specialized in FinTech |

Part of nested ecosystems of banks and innovation centres |

|

|

Cluster organizations |

FinanceEstonia as a key actor |

Under the control of banks and the Central Bank |

|

|

Customers |

Not perceived as a participant |

Key actor |

|

|

Conditions |

Institutions |

Ease of doing business, accessible |

Interlinked with large banks, insufficient support for entrepreneurship |

|

Culture and leadership |

Entrepreneurial culture with role models and serial entrepreneurship |

Entrepreneurial culture underdeveloped, no visible role models |

|

|

Networks |

Informal networks facilitated by the smallness of the country |

Dominated by banks and the Central bank |

|

|

Infrastructure |

Digital and technological leadership |

Advanced IT infrastructure |

|

|

Demand |

Small home market enforces scalability to foreign markets |

Large home market with loyal customers |

|

|

Intermediaries |

Moderate involvement in FinTech |

Mainly state-owned |

|

|

Talent |

Strong finance and technology talent through serial entrepreneurship |

Strong technology talent through the educational system; lack of entrepreneurial talent |

|

|

Knowledge |

Knowledge base through technology entrepreneurship and advanced technology and banking sectors |

Knowledge base through strong education and technology sector |

|

|

Finance |

Limited availability of venture capital |

Lack of venture capital, large banks have sufficient resources |

In Tallinn, the entrepreneurial culture, with a high presence of role models and technologically advanced talent and infrastructure, as well as institutional support, is conducive to the rapid evolvement and dominance of FinTech start-ups, compensating for the relatively weak ecosystem condition of the local demand. In Moscow, high domestic demand and bank-friendly institutions dominate among the ecosystem drivers, and culture was not believed to support the development of the FinTech ecosystem. While other studies have placed start-ups in the centre of the ecosystem, we show that this does not always hold: certain cultural and institutional conditions lead to the dominance of other actors, as our results indicate in the case of Moscow.

In both cities, universities were mainly viewed as a provider of human capital with no active involvement in the FinTech ecosystem, which contradicts Alaassar et al. (2021). Moreover, contrary to Castro et al. (2020) and Alaassar et al. (2021), investors and accelerators were not significant actors in the FinTech ecosystem due to their lack of specialization in FinTechs in the case of Tallinn or subordination to government or banks in Moscow, a feature potentially differentiating emerging ecosystems from developed ones.

In sum, we observed a start-up-centred ecosystem in Tallinn, built on a strong culture, technologically advanced human capital, and infrastructure. In Moscow, conversely, the FinTech scene is oriented towards the local market and characterized by isolated ecosystems of banks and a relatively underdeveloped nested ecosystem servicing start-ups.

The present study contributes to the literature on EEs and FinTech in several ways. First, the study illustrates how EE conditions, such as culture, demand and institutions, impact the way individual ecosystem actors develop and operate within a structured ecosystem configuration, and thus adds to the understanding of sectoral variations in EEs while highlighting distinct features of emerging ecosystems. Extending the model of I. Lee and Shin (2018) and subsequent empirical works (Castro et al., 2020; Hendrikse et al., 2020; Zhang-Zhang et al., 2020), we have constructed the internal layer of the FinTech ecosystem actors. This enables observation of the roles and interrelations of start-ups, banks, regulators, and other players stemming from the specifics of FinTech. By combining the prior models and empirical results, we can observe a richer set of actors.

Second, the study contributes to the literature by complementing its framework on FinTech actors with the second line of literature relying on the EE research (Alaassar et al., 2021; Sohns & Wójcik, 2020), thus adding the outer layer of EE conditions. Through the framework, the present study helps to integrate the streams of research on FinTech ecosystems, combining FinTech actors with EE conditions. The role of conditions enables us to acknowledge the broader EE where FinTech actors operate and to pay attention to the influence of the ecosystem elements on roles and interrelations of actors. While Sohns and Wójcik (2020) focus on selected actors and ecosystem conditions in the context of one specific intervention, and Alaassar et al. (2021) study interrelations of start-ups with other actors, we integrate the whole set of actors and ecosystem conditions, thus contributing to the literature by offering a holistic view of the FinTech ecosystem. We also contribute to the prior research by highlighting the potential implications of the variations of entrepreneurial culture, characteristics of the home demand and formal institutions in the development of FinTech ecosystems. Our empirical study also highlights the role of FinTech cluster organizations in building the connectivity between FinTech ecosystem actors.

Third, the present study contributes to the empirical studies of FinTech ecosystems (Alaassar et al., 2021; Hendrikse et al., 2020; Muthukannan et al., 2020; Sohns & Wójcik, 2020) with a comparative empirical analysis with data from Estonian-Russian perspectives, thereby enhancing the understanding of local conditions necessary to increase the likelihood of developing and maintaining an emerging FinTech ecosystem. Recent studies have called for comparative case studies on FinTech (Kavuri & Milne, 2019), and for more clarification on FinTech ecosystems in particular (Muthukannan et al., 2020). Our comparative case study demonstrates the existence of interdependencies between FinTech actors and conditions introduced in our framework in terms of the role of demand, culture, and institutions. This enables to explain how the roles and configurations of actors in different ecosystems emerge from specific locational conditions, and how ecosystems can potentially be developed addressing the key conditions. As FinTech services tend to be characterized by low profit margins and the need for scalability (D. K. C. Lee & Teo, 2015), we show that local demand is one of the forces shaping the configuration of FinTech ecosystems, the power of various actors and the nature of collaboration. We demonstrate that a high home demand is associated with a more polarised ecosystem configuration where incumbents have a stronger starting position. Small home markets are likely to lead to a more balanced ecosystem with multiple players, where newcomers are able to develop.

Fourth, while Sohns and Wójcik (2020) omit culture, which is considered one of the most fundamental EE conditions (Donaldson, 2021; Vedula & Kim, 2019), from their framework due to its general nature, our holistic approach enables us to capture the interplay between culture and other conditions, and FinTech actors. We show that the nature of entrepreneurial culture acts as a trigger or barrier for the evolvement of start-ups, impacting their position in the ecosystem and the overall balance in the ecosystem. We show that institutional conditions may determine the composition of the ecosystem depending on whether the priority is on promoting general ease of doing business or supporting and prioritizing certain actors. We found that institutions also influence other ecosystem conditions, such as access to finance or intermediaries. Finally, we also demonstrate that ecosystem conditions are likely to contribute to the emergence of a dominant actor in a particular ecosystem. While prior studies attribute the central role in entrepreneurial ecosystems to start-ups, we show that certain conditions may result in a different configuration where some other actors, for instance, incumbent banks, take leadership.

CONCLUSION

Building on the two lines of prior research on FinTech ecosystems, we have developed a comprehensive entrepreneurial ecosystem framework for FinTech and illustrated the interplay of ecosystem actors and conditions. Our multiple-case study of Tallinn and Moscow demonstrates the interdependence of ecosystem conditions and FinTech actors. The status of ecosystem conditions is likely to guide FinTech actors to take certain roles, and stronger cooperation between the main ecosystem actors, such as start-ups, regulatory and supervisory authorities, and banks is needed for the further development of the entrepreneurial ecosystem, both in informal and structured forms.

Our empirical research highlights the strengths and weaknesses of the studied FinTech ecosystems. The approach taken by banks with the support of the institutions in Moscow enables them to achieve rapid digitalization. On the other hand, according to our findings, the private ecosystems of banks are believed to inhibit the evolvement of the financial sector and a more comprehensive FinTech ecosystem in Moscow. The results emphasize the crucial role of regulators and supervisors in the FinTech ecosystems as the development of the sector is driven by regulation. High transparency and up-to-date regulations help to attract new participants and support the development of the existing ventures. It is crucial to facilitate cooperation between regulators and other participants. The newly established Innovation unit of the Estonian FSA is a good example of such an initiative.

When aiming to develop the FinTech ecosystem in a city, supporting FinTech cluster organizations might be one practical option, provided they have built a strong reputation among the ecosystem participants. At the same time, it is crucial to keep in mind the inclusiveness criterion of the ecosystem, ensuring that the cluster organization would not be dominated or governed by a couple of major market players or the state. Facilitating university–industry cooperation, either through cluster organizations or direct partnerships, might be another way of helping FinTech ecosystems to move to the next level of development, as low involvement of universities seems to be an aspect that distinguishes emerging FinTech ecosystems from more mature ones.

We acknowledge that this study also has several limitations, while providing several potential areas for future research. While we incorporate the layers of actors and ecosystem conditions in our conceptual framework, an additional dimension of the institutional and economic environment that might have implications for the composition and development of the FinTech ecosystem could complement our proposed view. Also, due to the complexity of the FinTech ecosystem phenomenon, our conceptual approach does not encompass the evolutionary aspect of ecosystems with its stages of development from nascence to resilience. A limitation of our empirical approach is that the results of the analysis cannot be considered generalizable to all FinTech ecosystems, as each ecosystem is the product of the unique historical and economic processes of the location.

Several of the actors of our initial framework were not considered active participants of the FinTech ecosystem in the two cities. In contrast to the prominent model of I. Lee and Shin (2018), technology developers play a modest role, probably since FinTech services tend to be built on relatively mainstream technologies. Future research should address if closer integration of the technology development into the FinTech ecosystem would influence its success.

As the research on FinTech ecosystems continues to evolve, frameworks are needed to study the interplay between the evolutionary dynamics of the ecosystem, roles of actors and ecosystem conditions. In addition, the implications of the potential invasion of Big Tech companies into the area of FinTech, requires a systematic approach in respect to the ecosystem configurations and related implications. While case studies are the first step in gaining knowledge on the emerging phenomenon of FinTech ecosystems, it is also necessary to quantify the presence and strength of FinTech actors, ecosystem conditions, and their interactions in various locations, and measure the impact of possible configurations on ecosystem success.

Acknowledgments

The authors appreciate the insightful feedback obtained from the participants of the European Centre for Alternative Finance Conference 2021. We are grateful to Professor Susanne Durst for her valuable feedback and advice on the various versions of the article, and to master’s students Elina Tasa and Lubov Solgan for contributing to the process of data collection. We also thank the participants of the interviews for their valuable insights and time.

References

Alaassar, A., Mention, A.-L., & Aas, T. H. (2021). Ecosystem dynamics: Exploring the interplay within fintech entrepreneurial ecosystems. Small Business Economics, 160, 120257. https://doi.org/10.1007/s11187-021-00505-5

Alvedalen, J., & Boschma, R. (2017). A critical review of entrepreneurial ecosystems research: Towards a future research agenda. European Planning Studies, 25(6), 887-903. https://doi.org/10.1080/09654313.2017.1299694

Arner, D. W., Barberis, J., & Buckley, R. P. (2015). The evolution of FinTech: A new post-crisis paradigm? University of Hong Kong Faculty of Law Research Paper No. 2015/047, UNSW Law Research Paper No. 2016-62. http://dx.doi.org/10.2139/ssrn.2676553

Audretsch, D. B., & Belitski, M. (2017). Entrepreneurial ecosystems in cities: Establishing the framework conditions. The Journal of Technology Transfer, 42(5), 1030-1051. https://doi.org/10.1007/s10961-016-9473-8

Audretsch, D. B., Cunningham, J. A., Kuratko, D. F., Lehmann, E. E., & Menter, M. (2019). Entrepreneurial ecosystems: Economic, technological, and societal impacts. The Journal of Technology Transfer, 44(2), 313-325. https://doi.org/10.1007/s10961-018-9690-4

Auerswald, P. E., & Dani, L. (2017). The adaptive life cycle of entrepreneurial ecosystems: The biotechnology cluster. Small Business Economics, 49(1), 97-117. https://doi.org/10.1007/s11187-017-9869-3

Banking Review. (2016). FinTech in Russia risks remaining exotic. Retrieved from https://bosfera.ru/event_report/fintech-v-rossii-riskuet-ostatsya-ekzotikoy

Bankir.Ru. (2015). From competition to cooperation. Fintech Lab - 2015 conference was held in Moscow. Retrieved from https://bankir.ru/novosti/20150706/ot-sopernichestva-k-sotrudnichestvu-v-moskve-sostoyalas-konferentsiya-fintech-lab-2015-10108828/

Basole, R. C., & Patel, S. S. (2018). Transformation through unbundling: Visualizing the global FinTech ecosystem. Service Science, 10(4), 379-396. https://doi.org/10.1287/serv.2018.0210

Berg, C., Novak, M., Potts, J., & Thomas, S. J. (2018). From industry associations to ecosystem associations: Blockchain, interest groups and public choice. Retrieved from http://dx.doi.org/10.2139/ssrn.3285647

Bloomchain. (2019). The Central Bank spoke about possible methods of regulating fintech in Russia. Retrieved from https://bloomchain.ru/newsfeed/tsentrobank-rasskazal-o-vozmozhnyh-metodah-regulirovaniya-finteha-v-rossii/

Bogers, M., Sims, J., & West, J. (2019). What is an ecosystem? Incorporating 25 years of ecosystem research. Academy of Management Proceedings, 2019(1). Retrieved from https://ssrn.com/abstract=3437014 or http://dx.doi.org/10.2139/ssrn.3437014

Braun, V., & Clarke, V. (2006). Using thematic analysis in psychology. Qualitative Research in Psychology, 3(2), 77-101. https://doi.org/10.1191/1478088706qp063oa

Brown, R., & Mason, C. (2017). Looking inside the spiky bits: A critical review and conceptualisation of entrepreneurial ecosystems. Small Business Economics, 49(1), 11-30. https://doi.org/10.1007/s11187-017-9865-7

Castro, P., Rodrigues, J. P., & Teixeira, J. G. (2020). Understanding FinTech ecosystem evolution through service innovation and socio-technical system perspective. In Exploring Service Science (pp. 187-201). https://doi.org/10.1007/978-3-030-38724-2_14

Claeys, S. (2005). Optimal regulatory design for the Central Bank of Russia BOFIT Discussion Papers 7, 41. https://doi.org/10.2139/ssrn.1002916

Cukier, D., & Kon, F. (2018). A maturity model for software startup ecosystems. Journal of Innovation and Entrepreneurship, 7(1). https://doi.org/10.1186/s13731-018-0091-6

Cusumano, M. A., & Gawer, A. (2002). The elements of platform leadership. MIT Sloan Management Review, 43(3), 51.

De Massis, A., & Kotlar, J. (2014). The case study method in family business research: Guidelines for qualitative scholarship. Journal of Family Business Strategy, 5(1), 15-29. https://doi.org/10.1016/j.jfbs.2014.01.007

Donaldson, C. (2021). Culture in the entrepreneurial ecosystem: A conceptual framing. International Entrepreneurship and Management Journal, 17(1), 289-319. https://doi.org/10.1007/s11365-020-00692-9

Dorfleitner, G., Hornuf, L., Schmitt, M., & Weber, M. (2017). Definition of FinTech and description of the FinTech industry. In G. Dorfleitner, L. Hornuf, M. Schmitt, & M. Weber (Eds.), FinTech in Germany (pp. 5-10). Cham: Springer. https://doi.org/10.1007/978-3-319-54666-7_2

Ermakova, E. P., & Frolova, E. E. (2019). Legal regulation of digital banking in Russia and foreign countries (European Union, USA, Prc). [Правовое регулирование цифрового банкинга в России и зарубежных странах (Европейский союз, США, КНР)]. Вестник Пермского университета. Юридические науки (46), 606-625. https://doi.org/10.17072/1995-4190-2019-46-606-625

Evans, D. S. (2003). The antitrust economics of multi-sided platform markets. Yale Journal on Regulation., 20(2), 325-382.

FinanceEstonia. (2020). Taavi Tamkivi: Eesti startupide trump on koduturu väiksus. [Estonian startups benefit from the small home market]. Retrieved from http://financeestonia.eu/news/taavi-tamkivi-eesti-startupide-trump-on-koduturu-vaiksus/

Finnopolis. (2016). Program of conference. Retrieved from http://www.finopolis.ru/archive/2016/program/

Fredin, S., & Lidén, A. (2020). Entrepreneurial ecosystems: Towards a systemic approach to entrepreneurship? Geografisk Tidsskrift-Danish Journal of Geography, 120(2), 87-97. https://doi.org/10.1080/00167223.2020.1769491

Gazel, M., & Schwienbacher, A. (2021). Entrepreneurial fintech clusters. Small Business Economics, 57(2), 883-903. https://doi.org/10.1007/s11187-020-00331-1

Giglio, F. (2022). Fintech: A literature review. International Business Research, 15(1), 1-80. https://doi.org/10.5539/ibr.v15n1p80

Gimpel, H., Rau, D., & Röglinger, M. (2018). Understanding FinTech start-ups – a taxonomy of consumer-oriented service offerings. Electronic Markets, 28(3), 245-264. https://doi.org/10.1007/s12525-017-0275-0

Gomber, P., Koch, J.-A., & Siering, M. (2017). Digital finance and Fintech: Current research and future research directions. Journal of Business Economics, 87(5), 537-580. https://doi.org/10.1007/s11573-017-0852-x

Hakala, H., O’Shea, G., Farny, S., & Luoto, S. (2020). Re‐storying the business, innovation and entrepreneurial ecosystem concepts: The model‐narrative review method. International Journal of Management Reviews, 22(1), 10-32. https://doi.org/10.1111/ijmr.12212

Halinen, A., & Törnroos, J.-Å. (2005). Using case methods in the study of contemporary business networks. Journal of Business Research, 58(9), 1285-1297. https://doi.org/10.1016/j.jbusres.2004.02.001

Harris, J. L. (2021). Bridging the gap between ‘Fin’ and ‘Tech’: The role of accelerator networks in emerging FinTech entrepreneurial ecosystems. Geoforum, 122, 174-182. https://doi.org/10.1016/j.geoforum.2021.04.010

Hendrikse, R. (2018). Appleization of finance. Finance and Society, 4(2), 159-180. https://doi.org/10.2218/finsoc.v4i2.2870

Hendrikse, R., van Meeteren, M., & Bassens, D. (2020). Strategic coupling between finance, technology and the state: Cultivating a Fintech ecosystem for incumbent finance. Environment and Planning A: Economy and Space, 52(8), 1516-1538. https://doi.org/10.1177/0308518x19887967

Hornuf, L., Klus, M. F., Lohwasser, T. S., & Schwienbacher, A. (2021). How do banks interact with fintech startups? Small Business Economics, 57(3), 1505-1526. https://doi.org/10.1007/s11187-020-00359-3

Iman, N., & Tan, A. W. K. (2020). The rise and rise of financial technology: The good, the bad, and the verdict. Cogent Business & Management, 7(1), 1725309. https://doi.org/10.1080/23311975.2020.1725309

Isenberg, D. (2011). The entrepreneurship ecosystem strategy as a new paradigm for economic policy: Principles for cultivating entrepreneurship. Presentation at the Institute of International and European Affairs, May 12, 2011, Dublin Ireland.

Kavuri, A. S., & Milne, A. (2019). FinTech and the future of financial services: What are the research gaps? CAMA Working Papers, 18. https://dx.doi.org/10.2139/ssrn.3333515

Keogh, D., & Johnson, D. K. N. (2021). Survival of the funded: Econometric analysis of startup longevity and success. Journal of Entrepreneurship, Management, and Innovation, 17(4), 29-49. https://doi.org/10.7341/20211742

Lai, Y., & Vonortas, N. S. (2019). Regional entrepreneurial ecosystems in China. Industrial and Corporate Change, 28(4), 875-897. https://doi.org/10.1093/icc/dtz035

Laidroo, L., Koroleva, E., Kliber, A., Rupeika-Apoga, R., & Grigaliuniene, Z. (2021). Business models of FinTechs – Difference in similarity? Electronic Commerce Research and Applications, 46, 101034. https://doi.org/10.1016/j.elerap.2021.101034

Lee, D. K. C., & Teo, E. G. S. (2015). Emergence of FinTech and the LASIC principles. Journal of Financial Perspectives, 3(3). Retrieved from https://ssrn.com/abstract=3084048. http://dx.doi.org/10.2139/ssrn.2668049

Lee, I., & Shin, Y. J. (2018). Fintech: Ecosystem, business models, investment decisions, and challenges. Business Horizons, 61(1), 35-46. https://doi.org/10.1016/j.bushor.2017.09.003

Leendertse, J., Schrijvers, M., & Stam, E. (2021). Measure twice, cut once: Entrepreneurial ecosystem metrics. Research Policy, 104336. https://doi.org/10.1016/j.respol.2021.104336

Leong, C., Tan, B., Xiao, X., Tan, F. T. C., & Sun, Y. (2017). Nurturing a FinTech ecosystem: The case of a youth microloan startup in China. International Journal of Information Management, 37(2), 92-97. https://doi.org/10.1016/j.ijinfomgt.2016.11.006

Mason, C., & Brown, R. (2014). Entrepreneurial Ecosystems and Growth Oriented Entrepreneurship. Retrieved from https://www.oecd.org/cfe/leed/Entrepreneurial-ecosystems.pdf

Milian, E. Z., Spinola, M. d. M., & Carvalho, M. M. d. (2019). Fintechs: A literature review and research agenda. Electronic Commerce Research and Applications, 34, 100833. https://doi.org/10.1016/j.elerap.2019.100833

Mohan, D. (2020). Financial Services Guide to Fintech: Driving Banking Innovation Through Effective Partnerships. London: Kogan Page Ltd.

Muthukannan, P., Tan, B., Chian Tan, F. T., & Leong, C. (2021). Novel mechanisms of scalability of financial services in an emerging market context: Insights from Indonesian Fintech ecosystem. International Journal of Information Management, 61, 102403. https://doi.org/10.1016/j.ijinfomgt.2021.102403