Received 10 February 2022; Revised 7 May 2022; Accepted 10 May 2022.

This is an open access article under the CC BY license (https://creativecommons.org/licenses/by/4.0/legalcode).

Monika Klimontowicz, Ph.D. Hab., Department of Banking and Financial Markets, Faculty of Finance, University of Economics in Katowice, ul. 1 Maja 50, 40-287 Katowice, Poland, e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

Justyna Majewska, Ph.D., Department of Demography and Economic Statistics, Faculty of Informatics and Communication, University of Economics in Katowice, ul. 1 Maja 50, 40-287 Katowice, Poland, e-mail:This email address is being protected from spambots. You need JavaScript enabled to view it.

Abstract

PURPOSE: The paper aims to investigate the contribution of intellectual capital to banks' competitive and financial performance. METHODOLOGY: The paper uses data retrieved from a research survey. The questionnaire on IC contribution to banks' competitive performance was applied to executive managers of retail banks operating in the Polish banking market. The data collected for the assessment of financial performance were retrieved from banks' annual reports and referred to each year from 2012 to 2019. The data were analyzed by Principal Axis Factor Analysis (PAF) and Partial Least Squares Structural Equation Modelling (PLS-SEM). FINDINGS: The results revealed that banks' competitive and financial performance depends on both the intellectual capital and environmental factors. The relation between financial performance and intellectual capital is positively mediated by competitive performance, and environmental factors can affect the strength of this relationship. The findings show that applying the resource-based theory might not be sufficient to gain a competitive advantage and sustainable market position in the case of banks. IMPLICATIONS: The results develop IC knowledge and prove the necessity to conduct systematic research on their importance for creating value for customers and gaining competitive advantage. They also provide direction for banks' decision-makers concerning factors that should be taken into account to create competitive advantage, market performance, and efficiency. The Polish banking market has transformed from undeveloped and non-competitive into a developed and competitive one during the last few decades. Thus, the results also have implications for other companies operating in transition markets as their competitiveness depends on understanding which factors should be the foundation for their market strategy and their competitiveness and efficiency to become a developed one. ORIGINALITY AND VALUE: The majority of the IC research concentrate on developed countries, and very little is known about developing and transition countries that were successful on their journey. Most of the research has focused on identifying and measuring IC components and the relationship between them. Usually, the research presents the state of the art and it is based on financial reports. However, the extent to which IC impacts competitive and financial performance in banking markets has been relatively rare. To the authors' best knowledge, this is the first study to examine empirically the relationship between intellectual capital, environment, competitive performance, and efficiency in a transformed banking market in Europe, which analyses the IC contribution over a few years' perspectives.

Keywords: intellectual capital; competitive performance; financial performance; IC survey; principal axis factor analysis; partial least squares structural equation modeling

INTRODUCTION

Both academics and practitioners have already accepted the general significance of knowledge for further sustainable growth and wealth creation across all industries (OECD, 1996; Kehelwalatenna & Premaratne, 2014; Neves & Proença, 2021). The development of knowledge importance has increased the interest in managing a firm’s intellectual capital (do Rosario Cabrita & Vaz, 2006). The intellectual capital (IC) is defined as a crucial factor for sustainable competitive advantage (Steward, 1997; Edvinsson & Malone, 1997; Birchall & Tovstiga, 1999; Davenport & Pruzac, 2000; Mondal & Ghosh, 2012) and value creation (Edvinsson, 1997; Lev, 2001; Shaikh, 2004; Mavridis, 2005; Phusavat & Kanchana, 2007; Walsh, Enz & Canina, 2008; Schiavone, Meles, Verdoliva & Del Giudice, 2014; Chowdhury, Rana & Azim, 2019; Rehman, Aslam & Iqbal, 2022). In many instances, it appears to be significant for decision-making within the firm and external stakeholders and has implications for efficiency and productivity (Alhassan & Asare, 2016; Saymeh, Arikat, Hashem & Al-Khalieh, 2021). The banking sector, in general, offers an ideal area for IC research because the business nature of the banking sector is intellectually intensive (Mavridis, 2005; Branco, Delgado, Sousa & Sá, 2011; Ahuja & Ahuja, 2012; Neves & Proença, 2021).

During the last few decades, the banking sector has changed remarkably. Systematically increasing complexity of new technology, development of information and communication techniques, economy’s networking, globalization, and growth of customers’ expectations combined with regulatory requirements make banks face new challenges. New categories of risk have been revealed. The global financial crisis has reminded policymakers and customers that banks are the critical players in modern economies. The crisis showed that banks and the banking system are too important to be left to self-regulate. As a result, new regulatory requirements were implemented to ensure banks’ safety and sustainability. They concern equity capital requirements, liquidity requirements, and prudential standards (Basel III - Capital Requirements Directive CRDIV, Capital Requirements Regulation CRR). Another regulation that is thought to change market condition significantly is the Payment Service Directive (PSD2), opening the market for non-bank payment service providers. Additionally, a new generation of customers has entered the market. Compared with previous generations, the digital ones behave differently in the market. It will require adjusting banks’ market strategies and business models (First Data Corporation, 2010; Williams & Page, 2011; BMO Wealth Institute, 2014). Considering the disruptively changing business environment and all other external aspects influencing banks’ market activity, searching factors and analyzing the IC role in enabling banks to cope with them and concurrently gain the sustainable competitive advantage, market performance, and efficiency remain relevant. Although some empirical studies have found evidence to support the role of IC in helping to create a competitive advantage in the banking industry (Mondal & Ghosh, 2012) and its relationship with financial performance (Yaseen & Al-Amarneh, 2021; Neves & Proença, 2021), to the best of our knowledge, there are only a few that measure IC using a survey (Cabrita & Bontis, 2008; Curado, 2008; Mention & Bontis, 2013). Thus, providing the empirical evidence on the contribution of IC to the dynamics of the banks’ value creation process remains rare, exclusively within specific geographic regions and industries (Alhassan & Asare, 2016; Mention & Bontis, 2013; Yaseen & Al-Amarneh, 2021).

Given this background, the paper seeks to expand the literature on IC and performance from the perspective of European transition markets. Specifically, the paper investigates the contribution of IC to banks’ competitive and financial performance in Poland as an example of a country that successfully transformed from a developing country into a developed one. Achieving the purpose of the paper requires answering the following research questions (RQ):

RQ1) How strongly does the intellectual capital impact banks’ competitive and financial performance?

RQ2) To what extent may competitive performance impact the IC influence on banks’ financial performance?

RQ3) Do environmental factors impact the IC influence on banks’ competitive and financial performance?

RQ4) Does the size of a bank and the length of its market activity influence the assessment of IC’s influence on the financial performance?

Based on the research questions, the corresponding hypotheses were proposed. They were falsified using the Principal Axis Factor Analysis and Partial Least Squares Structural Equation Modelling. All calculations were done in R Project for Statistical Computing.

The remainder of this paper is structured as follows: the second section presents the literature review concerning IC as a foundation for banks’ competitive performance and formulates the hypothesis and conceptual model, the third section considers the research methodology and describes the data, the sample, the measurement of model variables and research methods, and the fourth section presents the empirical results and discussion. The paper concludes with summary evidence of the study and its limitations.

LITERATURE REVIEW AND HYPOTHESIS

Competitive performance shows a firm’s ability to convert its resources into strengths (Porter, 1990; Zineldin, 1996). According to the resource-based theory, the firm’s assets are the foundation for building competitiveness, market and financial performance (Hamel & Prahalad, 1990; Barney, 1991; Acur & Bititci, 2004; Cheng, Lin, Hsiao & Lin, 2010; Zubac, Hubbard & Johnson, 2010). IC and its importance as a strategic resource and a competitive factor have been widely discussed over the last few decades. Several authors defined the term (e.g., Edvinsson & Malone, 1997; Edvinsson, 1997; Lev, 2001; Phusavat & Kanchana, 2007; Neves & Proença, 2021), but no consensus emerged. The authors agree with its complex character, intangible nature, and incredible potential for creating value and building a competitive advantage for any company (Klein & Prusak, 1994; Edvinsson, 1997; Lev, 2001; Shaikh, 2004; Mavridis, 2005; Phusavat & Kanchana, 2007; Walsh, Enz & Canina, 2008; Mondal & Ghosh, 2012). Unquestionably, IC is a link between knowledge, talent, skills, creativity, innovativeness, and other resources supporting the company’s effectiveness and performance. Most of the existing studies are focused on developed countries, and, therefore, there is still little knowledge about the impact of IC in developing and emerging economies (Petty & Guthrie, 2000). They are mostly conducted in Africa and Asia in the banking industry, while a few transition economies are worth exploring in the European Union. To bridge this gap, the authors decided to choose Poland as one of the forerunners among new EU members. In the banking market, the researchers usually apply selected definitions and focus on factors that influence the IC perception and IC performance or, conversely, the influence of IC or its components on different aspects of firms’ performance. In this paper, bank’s intellectual capital is defined as a strategic intangible asset that enables building a long-term sustainable competitive advantage.

There is a variety of IC typologies proposed and followed by authors. The term is extended to a complex list of components or narrowed down to just a few ones. Some scholars divide IC into human capital and structural capital (Petty & Guthrie, 2000; Joia, 2000). Another approach presents IC as three components, such as people, internal structure and external structure, corresponding to human capital (human resources, human assets), structural (organizational, infrastructure) capital, and relational (customer, client) capital (Roos & Roos, 1997; Bontis, 1998; Dzinkowski, 2000; Roos, Bainbridge & Jacobsen, 2001; McElroy, 2002). Many researchers split IC into different factors and items, further associated with variables to measure market efficiency and performance (Joshi, Cahill & Sidhu, 2010; Shih, Chang & Lin, 2010). Despite the authors’ research, there were just a few attempts to examine some aspects of IC in Poland. Two of them focused on human resources. The first study concerned human management as a critical indicator of business activity (Haffer & Kristensen, 2010). The second one presented the integration of human resources responding to mergers of western corporations in Poland (Łupina‐Wegener, 2013). Only one referred to the banking market and aimed to present a method enabling the assessment of the competitiveness of listed banks in Poland, taking economic and intellectual capital (Anielak-Sobczak, 2022).

Curado (2008), states that IC is identified as a different concept in the banking industry. This paper illustrates three different IC components of the banking industry: human capital, internal structures, and external structures. Some authors add a fourth component connected with the influence of technology on the financial service industry (Shih, 2008). On the contrary, others use a synthetic measure to examine the IC efficiency, such as as HCE, SCE and RCE (Poh, Kilicman & Ibrahim, 2018; Rehman, Aslam & Iqbal, 2022) or employ VAIC or other similar methods such as VAICTM to analyze the performance of banks, focusing on IC and its influence on different aspects of banks’ market position (Cabrita & Vaz, 2006, Mavridis, 2005; Alhassan & Asare, 2016; Goh, 2005; El‐Bannany, 2008; Al-Musali & Ismail, 2014; Singh, Sidhu, Joshi & Kansal, 2016; Mohammed & Irbo, 2018; Umanto & Atmoko, 2018; Xu, Haris & Yao, 2019; Neves & Proença, 2021; Yaseen & Al-Amarneh, 2021) or base their research on case studies (Murthy & Mouritsen, 2011; Hosseini & Owlia, 2016; Nawaz & Ohlrogge, 2022). Measuring IC using a survey is still unique (Cabrita & Bontis, 2008; Curado, 2008; Mention & Bontis, 2013). The question of what IC components are essential for building banks’ competitive and financial performance is still relevant. The studies consider IC or its components in two ways: as a dependent or an independent variable. The analysis of IC components applied in the concepts mentioned above from the perspective of a characteristic of banking products and services as well as competition in banking markets led to the conclusion that, as a strategic intangible asset that enables building a long-term sustainable competitive advantage, they should be grouped around three major categories – capital of processes, human capital, and relational capital. Analyzed together as IC, they influence both banks’ competitive and financial performance (H1).

During the last few decades, banking markets have experienced turbulent changes caused by globalization, liberalization, technology development, increasing customer expectations and regulatory requirements. On the one hand, fulfilling the regulatory requirements of Basel III concerning the level of capital and liquidity has resulted in increasing costs. On the other hand, the Payment Service Directive (PSD2) has opened the market for non-bank, payment service providers and has resulted in stronger competition. Additionally, a new generation of customers has entered the market. The digital ones’ purchase behavior will require adjusting banks’ market strategy and business models (First Data Corporation, 2010; Williams & Page, 2011; BMO Wealth Institute, 2014). As a result, maintaining a sustainable market position becomes more and more difficult. It is especially challenging for countries like Poland, where the competition is relatively recent. Even if the first banking houses were established in the 15th century there, and a few banks established over 100 years ago are still operating in the Polish banking market, the Polish history, the loss of independence and the socialist economy resulted in a lack of competitiveness. The banks’ market behavior started to change in 1989 after the introduction of a new Act of Banking that enabled the establishment of non-state banks. The market response was immediate. By the end of 1992, there were 54 domestic banks. Since then, mergers and acquisitions have become essential for gaining a more significant market share and restructuring some of them. Poland’s entry into the European Union also resulted in cross-border consolidation (Klimontowicz, 2016). Today, 62 commercial banks are operating in the Polish banking market.

The number includes banks established in Poland and credit institutions established in European countries. Over half of them represent foreign capital investments. Mergers and acquisitions influence the number of banks, the sector’s ownership structure, and banks’ resource base (Chan, Koh & Kim, 2016) and impact market concentration (Kasman, 2010). The market structure may also impact the IC performance (El-Bannany, 2015). The most frequently used measures of banking market concentration are the Herfindahl-Hirschman index (HHI) and the concentration ratio (CR5). They are also considered as an indicator of the level of market competition. The HHI and CR5 ratios level reflect that until 2010 big banks had been developing their operational activity slower than small and medium-size banks. Since 2010, both indexes have been growing to a small degree but systematically. The data characterizing the Polish banking market (Table 1) shows that the market concentration level is relatively low, which may create new perspectives on further consolidations. The financial markets’ uncertainty, strengthened by the COVID-19 pandemic, seems to be the only barrier to large-scale mergers and acquisitions today. The economy of scale will influence the banks’ efficiency. As a result, banks operating in Poland diverge in competitive performance measured by market share, market value, and innovativeness, which may affect the influence of IC on banks’ financial performance (H2).

Table 1. The structural characteristic of the Polish banking market

|

|

2009 |

2010 |

2011 |

2012 |

2013 |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

|

|

Commercial banks |

||||||||||||

|

Number of domestic banks |

46 |

46 |

45 |

43 |

39 |

36 |

36 |

36 |

35 |

32 |

30 |

|

|

Number of credit institutions |

18 |

21 |

21 |

25 |

28 |

28 |

27 |

27 |

28 |

31 |

32 |

|

|

Market concentration |

||||||||||||

|

HHI |

0.574 |

0.559 |

0.563 |

0.568 |

0.586 |

0.656 |

0.670 |

0.659 |

0.648 |

0.691 |

0.697 |

|

|

CR5 |

44.2 |

43.9 |

44.3 |

45.0 |

46.0 |

48.5 |

48.8 |

48.5 |

47.9 |

50.0 |

50.3 |

|

|

Ownership structure |

||||||||||||

|

Number of domestic banks |

7 |

6 |

8 |

7 |

8 |

8 |

10 |

12 |

14 |

13 |

13 |

|

|

Number of foreign banks |

57 |

61 |

58 |

61 |

59 |

56 |

53 |

51 |

49 |

50 |

49 |

|

|

Share of domestic banks’ capital |

31.9 |

33.8 |

35.0 |

36.4 |

36,8 |

38.5 |

41.0 |

43.5 |

54,7 |

53,2 |

53,9 |

|

|

Share of foreign banks’ capital |

68.1 |

66.2 |

65.0 |

63.6 |

63.2 |

61.5 |

59.0 |

56.5 |

45,3 |

46,8 |

46,1 |

|

Source: Own elaboration based on NBP 2007-2020.

Answering the question of how to cope with environmental factors influencing banking business and developing market performance (obtain a competitive advantage and sustainable market position) ensuring the appropriate level of efficiency remains the current research task. In the IC research, banks’ financial performance is usually measured by return on assets (ROA) (Yaseen & Al-Amarneh, 2021) and a return on equity ratio (ROE) (Musali & Ismail, 2014; Mohammed & Irbo, 2018). Competitive performance and financial performance represent the two main aspects of overall organizational performance (Kianto, Andreeva, & Pavlov, 2013). In the case of banks, the external factors (competitive environment), such as banking market conditions, other banks’ competitiveness and lowering the entry barriers, are thought to be the most important among all factors influencing banks’ competitive and financial performance (Özkan-Günay, Günay, & Günay, 2013; El-Bannany, 2015). As a result, the following hypothesis (H3) was formulated, stating that the competitive environment moderates the relationship between IC and banks’ competitive performance as well as the competitive performance and financial performance. As the financial performance measured by the average rate of ROA and ROE change, may also be influenced by the size of the bank and the length of its market activity, the last hypothesis refers to this relationship (H4). The financial performance presents how banks manage their resources to generate profits. ROA shows banks’ ability to generate income using assets, while ROE assesses the financial return on a shareholder’s investment. That is why those indexes are commonly used as financial performance measures (Al-Musali & Ismail, 2014; Poh, Kilicman, & Ibrahim, 2018; Soewarno & Tjahjadi, 2020; Neves & Proença, 2021; Saymeh, Arikat, Hashem, & Al-Khalieh, 2021; Nawaz & Ohlrogge, 2022).

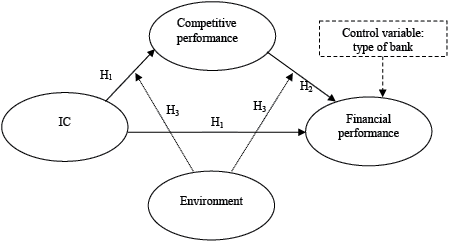

The IC literature review and analysis of banks’ competitive landscape lead to research questions and hypotheses that are the foundation of the conceptual model to investigate IC’s contribution to banks’ competitive and financial performance. To the authors’ best knowledge, any research develops the structure of IC components from the perspective of their ability to create banks’ competitive and financial performance. The conceptual model consists of the following variables:

- the independent variable: intellectual capital;

- the mediating variable: competitive performance;

- the dependent variable: financial performance;

- the moderating variable: market environment;

- the control variable: size of the bank and the length of its market activity (the type of bank)

and serves to falsify the following hypotheses that reflect the relationships between the model dimensions and variables (Figure 1):

H1: IC has a strong direct positive impact on both banks’ competitive and financial performance.

H2: Competitive performance affects the influence of IC on banks’ financial performance.

H3: The competitive environment moderates the relation between the competitive performance and financial performance, as well as the relationship between IC and banks’ competitive performance.

H4: The size of the bank and the length of its market activity influences the financial performance measured by the average rate of ROA and ROE change.

Figure 1. The conceptual model

RESEARCH METHODOLOGY

A two-step approach was implemented to test the hypotheses. The goal of the first step was to create a measurement model and obtain an acceptable fit of the data. In the second step, the structural model was statistically verified based on the measurement model found in the first step. As there is a time lag in the impact of IC on entities’ performance (Kujansivu & Lönnqvist, 2007), the data on financial performance were collected over 2012-2019 from banks’ annual reports.

Measurement of variables

The development of measurement tools for the variables mentioned above was based on a generalization of the literature review. The verification of content validity employed experts’ assistance to determine the contents’ fitness, enhance content validity, and ensure questionnaire effectiveness. After interviews with experts, the questions were modified (Joshi, Cahill & Sidhu, 2010; Shih, Chang & Lin, 2010). Therefore, the questionnaire in the field of measuring IC and environment factors should carry a certain degree of content validity.

A set of 45 IC items was proposed to create a suitable IC measurement model. Each of them was assessed from the perspective of its role in building banks’ competitive performance. The variables were made operative according to the Likert seven-point scale (where 7 meant the highest level of importance and 1 – no importance).

The competitive performance was measured by market share, market value, and a bank’s innovativeness. Klimontowicz (2016) adopted the scale developed and validated by Deshpandé, Farley and Webster (1993) and Drew (1997) and later used by Lee and Choi (2003). The original scale contains five components and aims to measure the organization’s market share, growth, profits, innovativeness, and overall success against its competitors. The market share meant the relation of a bank’s assets to the total assets of retail banks operating in Poland. The growth, profits, and overall success were integrated into market value. The market value refers to market capitalization obtained by multiplying the number of the bank’s outstanding shares by the current share price. The innovativeness described the bank’s ability to exhibit consistently innovative behavior over time, meaning three dimensions: the number of innovations adopted over time, the time of innovations’ adoption, and the consistency of the adoption of innovations’ time (Subramanian & Nilakanta, 1996). The executive managers assessed the bank’s competitive performance in comparison with other retail banks. Each variable was measured using the Likert seven-point scale (where 7 meant being significantly better and 1 being significantly worse than competitors).

Following Al-Musali and Ismail (2014), banks’ financial performance was measured by a return on assets ratio (ROA) and a return on equity ratio (ROE). ROA reflects the efficiency of utilizing available assets in creating profits and it is calculated as the annual net profit of an individual bank divided by average total assets. ROE measures bank profitability by revealing how much profit a bank generates with the money invested by shareholders. Both ratios are commonly applied as measures of financial performance in IC research (Al-Musali & Ismail, 2014; Poh, Kilicman & Ibrahim, 2018; Soewarno & Tjahjadi, 2020; Neves & Proença, 2021; Saymeh, Arikat, Hashem & Al-Khalieh, 2021; Rehman, Aslam & Iqbal, 2022). The impact of IC on further financial performance was measured by the average ROA and ROE change rate over 2012-2019 for each bank separately.

The environment was measured by 21 items considered essential influencers in the banking market during the last few decades. They were made operative according to the Likert seven-point scale (where 1 meant no influence on the bank, 7 – very high impact on the bank).

Following the Polish banking characteristics, for control variables, the size of the bank (Shiu, 2006; Chan, 2009; Al-Musali & Ismail, 2014; El-Bannany, 2015) and the length of market (El-Bannany, 2015) activity were used. The size of the bank was measured by the level of capital and the total assets. Some researchers chose only large banks as a sample (Curado, 2008; El‐Bannany, 2008). Analysis of the Polish banking market concentration showed that the largest banks do not always have a dominant position in the market. Thus, the size of the bank may influence market performance and efficiency. Concurrently, substantial differences concerning the length of market activity characterize the banking market. Shih, Chang, and Lin (2010) focused on the banks’ ownership. Their research sample included privately owned commercial banks, state-owned banks, and cooperative banks. As the vast majority of Polish banks are privately owned, there is no rationale to use ownership as a control variable in the case of the Polish banking market.

Research methods

Structural equation modeling (SEM) was implemented to examine the conceptual model. The choice of SEM is justified because of the need to test an integrated set of dependence links, distinguish between direct and indirect effects, and account for the measurement errors of the multi-item constructs (Anderson & Gerbing, 1988).

Two steps were scoped to read the SEM model (Barclay, Higgins, & Thompson, 1995): 1) an analysis of measuring model and 2) an analysis of structural model. A measurement model represents the relationships between constructs and their corresponding indicator variables, while the structural model tests all the hypothetical dependencies based on path analysis.

Exploratory and confirmatory analyses were conducted to construct and check the reliability and validity of the proposed IC and environment measuring scales. A specific dataset, where the number of variables is higher than the number of observations, forced the search for non-classical approaches to extract IC and environment components. Therefore, the Principal Axis Factor Analysis (PAF) implemented in the high dimension molecular data (HDMD) package in the R environment was applied (McFerrin, 2013). PAF is similar to principal components analysis, but a reduced matrix where the diagonals are the commonalities is taken into account (Revelle, 2013). For data with more variables than observations, the covariance matrix is singular, and a general inverse is used to determine the inverse correlation matrix and estimate scores. In this case, the principal axis factor method of analysis allows estimating commonalities by iteratively updating the diagonal of the correlation matrix and solving the eigenvector decomposition (McFerrin, 2013). Commonalities for each variable are estimated according to the number of factors, and convergence is defined by stabilizing total commonalities between iterations.

The analysis assessed (1) the effects of IC on financial performance (both directly and indirectly, through competitive performance), (2) the effect of IC on competitive performance (as moderated by environment), and (3) the effect of competitive performance on financial performance (as moderated by event environment). Thus, the structural model with moderated mediation effects is analyzed. In general, the moderated mediation effect indicates the presence, in a single model, of one or more mediating variables and one or more moderating variables.

A moderator variable interacts with a mediator variable such that the value of the indirect effect changes depending on the value of the moderator variable (such a situation is also referred to as a conditional indirect effect) (Hair, Hult, Tomas & Ringle, 2017). A conceptual and statistical model of a conditional process can be found in Hayes (2013) (model 58). Both mediation and moderation effects are tested simultaneously using a structural equation method. A general model to test these effects is created to include all possible interactions between variables in the mediation and moderation models (MacKinnon, 2008). The PLS-SEM algorithm (The Partial Least Squares Structural Equation Modelling) was selected for estimating the relationships in a structural equation model. PLS path modeling is a soft-modeling technique with less rigid distributional assumptions on the data. Research by other authors (e.g., Goodhue, Lewis, & Thompson, 2012) indicates that PLS-SEM performs as effectively as the other techniques in detecting actual paths and not falsely detecting non-existent paths when analyzing small sample sizes or data with non-normal distributions. The structural relationships were measured using PLS-SEM bootstrapping to achieve the significance of the correlation. The number of cases used was 5000 samples for the bootstrapping procedure (Hair, Ringle, & Sarstedt, 2011).

The IC, competitive performance and market environment are modeled based on a reflective measurement model. The financial performance is a composite variable and it serves as a construct. Considering all of the above, we are dealing with the reflective-formative, the second-order hierarchical component model.

Evaluation of reflective measurement models were assessed using composite reliability (the reliability), whereas validity is evaluated using the convergent validity (average variance extracted, AVE) and discriminant validity following the Fornell-Larcker criterion. After reliability and validity are established, the primary evaluation criteria for PLS-SEM results are the coefficients of determination (R2) as well as the size and significance of the path coefficients. Besides the f2 effect sizes, predictive relevance (Q2), and the q2 effect sizes give additional insights into the quality of the model estimations (Hair, Hult, Tomas, & Ringle, 2017).

Data collection and sample

The dataset used to explore the research hypotheses covers 2012-2019. The empirical study on IC was conducted in 2012. The data collected for the assessment of financial performance were retrieved from banks’ annual reports and referred to each year from 2012 to 2019.

The survey’s target group consisted of all retail banks operating in Poland, defined as banks that offer a broad range of financial services to different segments of individual customers and fulfill all their financial needs and expectations. According to this definition, among the retail banks’ features differentiating them from other banks is the broad range of distribution channels, products, and services dedicated to individuals. Their operating activity’s financial sources (liabilities) are based on customers’ deposits. They are primarily used in developing loans and credit products (assets). Questionnaires were spread among high-level managers responsible for organizational development, who know the bank’s competencies and capabilities. The research was conducted under the auspices of the Polish Banks Association and the National Science Centre. The data was collected by two methods – PAPI (personal and pencil interviews) and CAWI (computer-assisted web interviews). 37.9% of banks’ executive managers responded to the research invitation and filled in a questionnaire correctly (the total number of retail banks operating in the Polish banking market in 2012 was 29). A similar sample size was applied in other research conducted in European banking markets (e.g., Neves & Proença, 2021; Anielak-Sobczak, 2022). All the questionnaires were completed by senior (54.5% of the respondents) or middle-level (45.5%) managers.

The sample included banks established in Poland and credit institutions operating in the Polish banking market but established in European countries. The list of banks that conformed to this definition is presented in Table 2.

The number of samples is accurate for applying multiple regression analysis of the SEM-PLS model. The statistical power of the sample using Cohen’s retrospective test (1992) was carried out as it was suggested in Hair, Hult, Tomas, and Ringle (2017). As the number of independent variables in the measurement and structural models is two, we need 11 observations to achieve a statistical power of 80% for detecting R2 values of at least 0.5 with a 5% probability of error.

Table 2. The list of retail banks operating in Poland (the target population)

|

Banks |

|

|

Alior Bank SA Bank BPH SA Bank DnB Nord Polska SA Bank Gospodarki Żywnościowej SA Bank Handlowy w Warszawie (CitiHandlowy) Bank Millenium SA Bank Ochrony Środowiska SA Bank Pocztowy SA Bank Polska Kasa Opieki SA Bank Polskiej Spółdzielczości SA Bank Zachodni WBK SA BNP PARIBAS SA Oddział w Polsce BRE Bank SA Credit Agricole Bank Polska SA Deutsche Bank Polska SA |

Eurobank SA FM Bank SA Getin Noble Bank SA Idea Bank SA ING Bank Śląski SA Invest Bank SA Kredyt Bank SA Meritum Bank ICB SA Nordea Bank Polska SA PKO Bank Polski SA Polbank EFG SA Raiffeisen Bank Polska SA Santander Consumer Bank Polska SA SGB Bank SA |

Altogether, the sample banks’ assets represented 79.4% of total Polish banking sector assets. The total assets of banks that responded to the questionnaire correctly equaled PLN 561 205 million, which corresponded to 61.01% of all sample banks and 48.44% of all banks operating in the Polish banking market. The structure of the assets was as follows: 54.5% accounted for domestic capital, while 45.5% accounted for foreign capital. Such a structure corresponded to the capital structure of the Polish banking system. Over half of the banks that participated in the research were medium-sized and large banks with assets exceeding PLN 20 billion. The sample structure in terms of the value of assets is presented in Table 3.

Table 3. The structure of the sample in terms of the value of assets

|

The value of sample banks’ assets (in billion) |

The share in the research sample (in %) |

|

1-5 |

9.1 |

|

5.1-10 |

9.1 |

|

10.1-20 |

27.3 |

|

20.1-50 |

18.2 |

|

over 50 |

36.4 |

The sample included banks with over a hundred years of tradition, banks established after 1989 and those found in the current century. These groups are represented evenly – 36.4% of the surveyed banks started operating before the political transformation, 27.3% in the 1990s, and 36.4% after 2000. The sample was also diversified considering the banks’ number of employees and the number of branches (Tables 4 and 5).

Table 4. The structure of the sample in terms of the number of employees

|

The number of employees (in thousands) |

The share in the research sample (in %) |

|

less than 1 |

9,1 |

|

1.1-5 |

36.4 |

|

5.1-10 |

18.2 |

|

Over 10 |

36.4 |

Table 5. The structure of the sample in terms of the number of branches

|

The number of branches |

The share in the research sample (in %) |

|

less than 50 |

9.1 |

|

51-100 |

9.1 |

|

101-200 |

9.1 |

|

201-300 |

9.1 |

|

301-500 |

27.3 |

|

over 500 |

36.4 |

Considering the retail banks’ features, such as the value of assets, banks’ territorial scope and business profile, the year of banks’ establishment, the number of employees and branches, and persons filling in the questionnaire, the analyzed sample may be considered representative.

RESULTS AND DISCUSSION

The analysis of the measuring model

The factor analysis was applied to answer the question concerning IC components and their importance in creating value for customers and gaining a competitive advantage in the market (competitive performance and efficiency). The results identified three dimensions of IC and three dimensions of the environment. From 45 items designed to measure IC, 28 items remained: 12 items loaded the capital of processes, 7 items loaded human capital and 9 items loaded relational capital. Three factors of IC account for 72.3% of the item variance, with the first factor (Capital of Processes) which explains 40.7% of the total variance. The results of the factor composite reliability, Cronbach’s α and AVE, are superior to the limits set in the literature (i.e., Cronbach’s α≥0.7; composite reliability≥0.7, AVE≥0.5) (Roldán & Sánchez-Franco, 2012). Table 6 introduces the items representing the variables and factor loadings concerning IC (only items with a factor loading at least 0.70 are considered).

Table 6. Reliability of measurement IC scale

|

Latent variables and scale items |

Loading |

Composite reliability |

Cronbach α |

AVE |

|

Capital of Processes (PC) |

0.963 |

0.885 |

0.765 |

|

|

The level of service modernity |

0.814 |

|||

|

The investment in innovations |

0.844 |

|||

|

The implementation of innovative products |

0.791 |

|||

|

The implementation of innovative procedures |

0.883 |

|||

|

The usage of technology in bank’s management |

0.821 |

|||

|

The investment in marketing |

0.737 |

|||

|

The number of employees |

0.770 |

|||

|

The efficiency and timeliness of services |

0.828 |

|||

|

The usage of traditional distribution channels |

0.931 |

|||

|

The usage of modern distribution channels |

0.884 |

|||

|

The safe and comfortable way of transactions authorisation |

0.850 |

|||

|

The number of ATMs |

0.841 |

|||

|

Human Capital (HC) |

|

0.949 |

0.871 |

0.773 |

|

The will of cooperation and knowledge sharing |

0.783 |

|||

|

The quality of executive management |

0.953 |

|||

|

The quality of middle level management |

0.966 |

|||

|

The level of managers’ acceptance |

0.936 |

|||

|

The quality of the motivation system |

0.878 |

|||

|

The quality of leadership |

0.926 |

|||

|

The knowledge of clients’ needs |

0.867 |

|||

|

Relational Capital (RC) |

|

0.945 |

0.892 |

0.627 |

|

The brand value |

0.708 |

|||

|

The employees’ knowledge and the level of education |

0.804 |

|||

|

The employees’ identification with the bank’s objectives |

0.894 |

|||

|

The level of knowledge regarding a bank and its offer |

0.722 |

|||

|

A customer-oriented attitude |

0.773 |

|||

|

The ability to develop long-term relations with clients |

0.775 |

|||

|

The willingness to self-development |

0.872 |

|||

|

The level of employees’ innovativeness |

0.701 |

|||

|

The branches’ organisation and working hours |

0.819 |

Among the three dimensions of IC identified (capital of processes, human capital, and relational capital), the capital of processes presents the highest potential for creating bank’s competitive advantage. This finding does not correspond with some previous research conducted on the banking market that showed the dominance of human capital over the other IC components (e.g., Curado, 2008; Al-Musali & Ismail, 2014). But the internal structure of this IC dimension shows the importance of using technology and implementing innovations. Thus, the results correspond with studies that positively verified the relation between innovation capital and firms’ performance (Shih, 2008; Tseng, Lan, Lu & Chen, 2013) and market predictions concerning customers’ adoption of technology and innovations (First Data Corporation, 2010; Williams & Page, 2011; BMO Wealth Institute, 2014).

The internal structure of human capital reveals the significance of management and knowledge sharing for building banks’ competitive performance. The impact of IC strategic management on value creation was also found by Kianto, Andreeva and Pavlov (2013). The findings correspond with Shih, Chang, and Lin (2010), who pointed out the importance of exchanging and sharing information in banks. It is also consistent with the conclusion that creating knowledge variety is the most critical activity in the management of IC (Schiuma & Lerro, 2008). The results proved the role of relational capital in the process of building banks’ competitiveness. The internal structure of this IC corresponds with factors influencing customer loyalty in the banking sector (Skowron & Kristensen, 2012).

For the environment, 10 items remain from the original 21. The first dimension presents variables influencing the banking market conditions (5 items), the second consists of items referring to the market activity and the competitive strength of other banks (3 items) and the third one presents variables connected with entry barriers (2 items). Three dimensions of environment account for 64.9% of the total variance, with the first category explaining 30.3% of the total item variance. Table 7 introduces the environmental items representing the variables and factor loadings. The dimensions of environmental factors pointed out the importance of market conditions, the competitors’ strengths and entry barriers. This result coincides with previous market-based concepts that assumed market factors as determinants of firms’ competitive advantage (Porter, 1990; Acur & Bititci, 2004; Rumelt, 1991; Obłój, 2007).

Table 7. Reliability of the measurement environment scale.

|

Latent variables and scale items |

Loading |

Composite reliability |

Cronbach alpha |

AVE |

|

Banking Market Conditions (BMC) |

0.900 |

0.832 |

0.766 |

|

|

The establishment of new banks |

0.727 |

|||

|

The situation in financial markets |

0.760 |

|||

|

The market capacity |

0.824 |

|||

|

The number of competitors |

0.885 |

|||

|

The technological progress |

0.747 |

|||

|

Other Banks’ Competitiveness (OBC) |

|

0.878 |

0.787 |

0.506 |

|

The competitive strength of other banks |

0.871 |

|||

|

The level of customers’ loyalty |

0.839 |

|||

|

The competitors’ pricing policy |

0.810 |

|||

|

Entry Barriers (EB) |

|

0.815 |

0.795 |

0.526 |

|

The equity relationships |

0.849 |

|||

|

The deregulation of financial markets |

0.702 |

The competitive performance construct is composed of three items (market share, market value and a bank’s innovativeness) with these values of indicators: Cronbach’s α = 0.85, composite reliability = 0.84, AVE = 0.61. All factor loadings are higher than 0.8.

As the financial performance is a composite variable, hence no quality of measurement in the actual sense of the word takes place. Discriminant validity was calculated to observe to which extent a factor indeed differs from others (Hair Jr, Sarstedt, Hopkins & Kuppelwieser, 2014). To get such results, each factor’s AVE square root values were compared with the correlations between constructs associated with these factors (Fornell & Larcker, 1981). All cases (Tables 8 and 9) show values on the diagonal higher than corresponding correlations.

Table 8. Discriminant validity of dimensions of ICa

|

IC dimensions |

Capital of Processes |

Human Capital |

Relational Capital |

|

Capital of Processes |

0.875 |

||

|

Human Capital |

0.373 |

0.879 |

|

|

Relational Capital |

0.491 |

0.300 |

0.792 |

Note: aAVE square root has been calculated on the diagonal (in bold).

Table 9. Discriminant validity of dimensions of environment a

|

Environment dimensions |

Banking market conditions |

Other Banks’ Competitiveness |

Entry Barriers |

|

Banking Market Conditions |

0.875 |

||

|

Other Banks’ Competitiveness |

-0.050 |

0.711 |

|

|

Entry Barriers |

0.373 |

-0.109 |

0.725 |

Note: aAVE square root has been calculated on the diagonal (in bold).

The results mean that indicators displayed to measure the different given factors are reliable and have discriminant validity. Therefore, the analysis suggests that the scales possess composite, convergent, and discriminant validity.

The assessment of the structural model

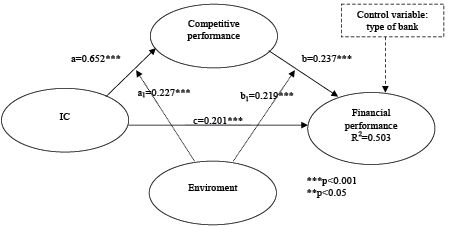

The first step of the structural model’s assessment relied on verifying the direct relationship between IC and financial performance. The effect obtained is positive and significant (β=0.224, p<0.05). In the second step, the mediator effect (i.e., competitive performance) was included. This indirect effect is positive and significant (between IC and competitive performance: β=0.316, p<0.001, and competitive performance and financial performance: β=0.320, p<0.001). The relationship between competitive performance and financial performance is not fully mediated according to the variance accounted for (VAF) index (Goodhue, Lewis & Thompson, 2012), resulting in a value of 0.418 (which is lower than 0.800 for total indirect effect – full mediation and higher than 0.200 for no mediation). The mediation effect did not eliminate the direct relationship between IC and financial performance. IC impacts 12.6% of the variance in competitive performance, which is quite significant, considering how many other issues affect the competitive performance of banks. The results of the structural model analysis are presented in Table 10.

The moderator effect, an environment of banks, was included in the next step to compare IC and competitive performance (first moderator effect) and the relation between competitive performance and financial performance (second moderator effect). The moderator effect of the environment is present in both relations. The moderator effect increases the explained variance of financial performance by 13%, confirming the double moderator effect of the environment of the proposed model. It is worth stressing that its absolute effect on financial performance is stronger than on competitive performance (Figure 2).

Table 10. Path analysis of the structural model

|

Path |

Path coefficient Beta |

R2 |

p-value |

|

Direct effect |

|||

|

IC→FP |

0.224 |

0.049 |

** |

|

Mediation effect |

|||

|

IC→FP |

0.217 |

** |

|

|

IC→CP→FP |

0.294 |

0.372 |

|

|

IC→CP |

0.316 |

0.126 |

*** |

|

CP→FP |

0.320 |

*** |

|

|

Conditional mediation effect |

|||

|

IC→FP (c) |

0.201 |

** |

|

|

IC→CP (a) |

0.652 |

*** |

|

|

CP→FP (b) |

0.237 |

** |

|

|

I.C.*E→CP*E→FP |

0.503 |

||

|

IC*E→CP (a1) |

0.227 |

0.145 |

** |

|

C.P.*E→FP (b1) |

0.219 |

** |

Note: ***p<0.001; **p<0.05.

Figure 2. Conditional mediation model

Considering this, the control variables (the size of the bank and the length of its market activity) are relevant and significant (coefficients are above 0.2, see Table 11).

Table 11. Control variables in the structural model

|

Variable |

Beta |

t-test |

|

Size of the bank |

0.310 |

6.102 |

|

Length of banks market activity |

0.218 |

8.327 |

The statistical assessment of the conceptual model describing the contribution of IC to banks’ competitive and financial performance verified the assumptions that have grown from a literature review. A summary of hypotheses is as follows (all hypotheses are confirmed):

H1: IC positively affects competitive and financial performance. The impact of IC on financial performance explains only 4.9% of the variance of financial performance and 12.6% of the variance of competitive performance. A similar level was considered by Kianto, Andreeva, and Pavlov (2013) as quite significant, considering how many other issues affect competitive performance. The results are coherent with other studies examining the IC impact on financial performance (e.g., Neves & Proença, 2021; Yaseen & Al-Amarneh, 2021; Nawaz & Ohlrogge, 2022; Rehman, Aslam & Iqbal, 2022) and competitive performance measured by market share (e.g., Rehman, Aslam & Iqbal, 2022) although they applied research methodology.

H2: Competitive performance has a moderator effect on the relationship between IC and financial performance. This effect leads to an increase up to 37.2% of this model’s capacity to define the explained variance of financial performance.

H3: Environment moderates positively the relationship between IC and competitive performance, as well as the relationship between competitive performance and financial performance. Findings suggest that the strength of moderation between IC and competitive performance is slightly weaker than the relationship between competitive performance and financial performance. It means that the environment plays a significant role in financial performance assessment. The created model (with competitive performance as moderator and environment as the mediator) explains 50.3% of the variance of financial performance. In the case of banks, the results show that applying the resource-based theory might not be sufficient to gain a competitive advantage and sustainable market position. Banks’ financial performance depends not only on the ability to manage intangible (IC) and tangible assets but also on fulfilling regulatory requirements and managing different kinds of risks (Holland, 2010). The impact of such external determinants of IC as a market structure was also investigated and proved by El-Bannany (2015).

H4: The size of the bank and the length of its market activity influences the financial performance measured by the average rate of ROA and ROE change. It is coherent with previous hypothesis verification, as fulfilling regulatory requirements is strictly connected with the level of capital and assets.

CONCLUSIONS

The paper presents the contribution of intellectual capital to banks’ competitive and financial performance. In designing the performance measurement system of the individual components of the proposed structural model, it was necessary to adjust them to specific characteristics of the banking sector. It helped find those components that can drive organizations to a higher degree of competition by improving the value creation process.

Among the three dimensions of IC identified (capital of processes, human capital, and relational capital), the capital of processes presents the highest potential for creating a bank’s competitive advantage. The findings extended the knowledge on IC structure and proved the necessity to conduct systematic research on their importance for creating value for customers and gaining competitive advantage. Due to changing environmental conditions in the banking market, particular IC components’ importance is changing. The dominance of human capital over the other IC components proved in previous research has not been confirmed. Today, the capacity to use technology and implement innovations seen in the capital of processes is much more critical. But still the management and knowledge sharing contribute significantly to banks’ value creation and competitive performance. The results proved the role of relational capital in the process of building banks’ competitiveness. The internal structure of this IC corresponds with factors influencing customer loyalty in the banking sector.

The research results pointed out the importance of market conditions, the competitors’ strength, and entry barriers, which has a huge impact on the theoretical foundation of further IC research. It seems irrelevant to apply only the resource-based theory anymore. A new attitude combining both resource-based and market-based approaches is needed.

The results proved the positive IC impact on banks’ competitive and financial performance. It must be stressed that the relationship between IC and financial performance is moderated by competitive performance. In contrast, the relationship between IC and competitive performance and the relationship between competitive performance and financial performance is moderated by the environment that has practical implications for banks. Their financial performance depends not only on the ability to manage intangible (IC) and tangible assets but also on addressing the environmental challenges, such as fulfilling regulatory requirements and managing different kinds of risks. The results confirmed that the environment plays a significant role in financial performance assessment. They also pointed out that in the banking market the size of the bank (the level of capital and assets) and the length of its market activity influences the financial performance measured by the average rate of ROA and ROE change.

The long journey from a transition economy and banking market into a developed one may be an inspiration for both entities operating in other emerging and transition countries, as well as entities entering and investing in those markets. Building competitiveness and managing efficiency depend on understanding which factors should be the foundation for market strategy. The results lead to new insights for banks’ decision-makers concerning factors that should be taken into account in the process of creating value for customers and gaining a competitive advantage. Shifting the importance to the capital of processes from other IC dimensions has practical implications for further technological investments. Meeting market challenges requires developing adequate managerial skills and focusing on factors that help build long-relations with customers. When making market decisions, managers should consider environmental factors that impact and strengthen the IC impact on competitive and financial performance.

This study is not free of limitations. The retrieved data cover the period from 2012 to 2019 and does not include the pandemic and Ukrainian war, which may impact the result. Thus, future research is needed to check if IC is also supporting competitive and financial performance in such an unpredictable situation. Future studies may cover other European banking markets enabling the results’ comparison. Today most of the research applies the VIAC and similar methodology that makes discussing the results difficult. Thus, the above study will constitute an important point of reference for future surveys.

References

Acur, N., & Bititci, U. (2004). A balanced approach to strategy process. International Journal of Operations & Production Management, 24(4), 388-408. https://doi.org/10.1108/01443570410524659

Ahuja, B. R., & Ahuja, N. L. (2012). Intellectual capital approach to performance evaluation: A case study of the banking sector in India. International Research Journal of Finance and Economics, 93(1), 110-122.

Alhassan, A. L., & Asare, N. (2016). Intellectual capital and bank productivity in emerging markets: Evidence from Ghana. Management Decision, 54(3), 589-609. https://doi.org/10.1108/MD-01-2015-0025

Al-Musali, M. A. K., & Ismail, K. N. I. K. (2014). Intellectual capital and its effect on financial performance of banks: Evidence from Saudi Arabia, Procedia – Social and Behavioural Sciences, 164, 201-207. https://doi.org/10.1016/j.sbspro.2014.11.068

Anderson, J. C., & Gerbing, D. W. (1988). Structural equation modelling in practice: A review and recommended two-step approach. Psychological bulletin, 103(3), 411-423. https://doi.org/10.1037/0033-2909.103.3.411

Anielak-Sobczak, K. (2022). A bank’s intellectual capital and its importance in building competitiveness on the example of Polish listed banks. Ekonomia i Prawo. Economics and Law, 21(1), 5–24. https://doi.org/10.12775/EiP.2022.001

Barclay, D., Higgins, C., & Thompson, R. (1995). The partial least squares approach to causal modeling: Personal computer adoption and use as an illustration. Technology Studies: Special Issue on Research Methodology, 2(2), 284-324.

Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1), 99-120. https://doi.org/10.1177/014920639101700108

Battagello, F. M., Grimaldi, M., & Cricelli, L. (2015). A rational approach to identify and cluster intangible assets: A relational perspective of the strategic capital. Journal of Intellectual Capital, 16(4), 809-834. https://doi.org/10.1108/JIC-06-2015-0050

Birchall, D.W., & Tovstiga, G. (1999). The strategic potential of a firm’s knowledge portfolio. Journal of General Management, 25(1), 1-16. https://doi.org/10.1177/030630709902500101

BMO Wealth Institute. (2014). Getting ahead: The financial challenges for generations X and Y. BMP Wealth Institute Report, The U.S Edition. Retrieved from https://www.bmo.com/privatebank/pdf/Q1-Wealth-Institute-Report-Getting-Ahead.pdf

Bontis, N. (1998). Intellectual capital: An exploratory study that develops measures and models. Management Decisions, 36(2), 63-76. https://doi.org/10.1108/00251749810204142

Branco, M. C., Delgado, C., Sousa, C., & Sá, M. (2011). Intellectual capital disclosure media in Portugal. Corporate Communications: An International Journal, 16(1), 38-52. https://doi.org/10.1108/13563281111100962

Cabrita, M. D. R., & Bontis, N. (2008). Intellectual capital and business performance in the Portuguese banking industry. International Journal of Technology Management, 43(1-3), 212-237. https://doi.org/10.1504/IJTM.2008.019416

Cabrita, M. D. R., & Vaz, J. L. (2006). Intellectual capital and value creation: Evidence from the Portuguese banking industry. Electronic Journal of Knowledge Management, 4(1), 11-20. Retrieved from www.ejkm.com

Chan, K. H. (2009). Impact of intellectual capital on organisational performance: An empirical study of companies in the Hang Seng Index (Part 1). The Learning Organisation, 16(1), 22-39. https://doi.org/10.1108/09696470910927650

Chan, S. G., Koh, E. H., & Kim, Y. C. (2016). Effect of foreign shareholdings and originating countries on banking sector efficiency. Emerging Markets Finance and Trade, 52(9), 2018-2042. https://doi.org/10.1080/1540496X.2016.1142231

Cheng, M. Y., Lin, J. Y., Hsiao, T. Y., & Lin, T. W. (2010). Invested resource, competitive intellectual capital, and corporate performance. Journal of intellectual capital, 11(4), 433-450. https://doi.org/10.1108/14691931011085623

Chowdhury, L. A. M., Rana, T., & Azim, M. I. (2019). Intellectual capital efficiency and organisational performance: In the context of the pharmaceutical industry in Bangladesh. Journal of Intellectual Capital, 20(6), 784-806. https://doi.org/10.1108/JIC-10-2018-0171

Cohen, J. (1992). Statistical power analysis. Current Directions in Psychological Science, 1(3), 98-101. https://doi.org/10.1111/1467-8721.ep10768783

Constantine, G. (2010). Tapping into Generation Y: Nine ways community financial institutions can use technology to capture young customers. A First Data White Paper. Retrieved from firstdata.com

Curado, C. (2008). Perceptions of knowledge management and intellectual capital in the banking industry. Journal of Knowledge Management, 12(3), 141-155. https://doi.org/10.1108/13673270810875921

Davenport, T., & Pruzac, L. (2000). Working Knowledge: How Organisations Manage What They Know. Boston, United States: Harvard Business Scholl Press.

Deshpandé, R., Farley, J. U., & Webster Jr, F. E. (1993). Corporate culture, customer orientation, and innovativeness in Japanese firms: A quadrad analysis. Journal of Marketing, 57(1), 23-37. https://doi.org/10.2307/1252055

Drew, S. A. (1997). From knowledge to action: the impact of benchmarking on organisational performance. Long Range Planning, 30(3), 427-441. https://doi.org/10.1016/S0024-6301(97)90262-4

Dzinkowski, R. (2000). The measurement and management of intellectual capital: An introduction. Management Accounting, 78(2), 32-36.

Edvinsson, L. (1997). Developing intellectual capital at Skandia. Long Range Planning, 30(3), 366-373. https://doi.org/10.1016/S0024-6301(97)00016-2

Edvinsson, L., & Malone, M. S. (1997). Intellectual Capital: Realising Your Company’s True Value by Finding Its Hidden Brainpower. London, England: Piatkus.

El‐Bannany, M. (2008). A study of determinants of intellectual capital performance in banks: The UK case. Journal of Intellectual Capital, 9(3), 487-498. https://doi.org/10.1108/14691930810892045

El-Bannany, M. (2015). Explanatory study about the intellectual capital performance of banks in Egypt. International Journal of Learning and Intellectual Capital, 12(3), 270-286. https://doi.org/10.1504/IJLIC.2015.070167

Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39-50. https://doi.org/10.1177/002224378101800104

Goh, P.C. (2005). Intellectual capital performance of commercial banks in Malaysia. Journal of Intellectual Capital, 6(3), 385-396. https://doi.org/10.1108/14691930510611120.

Goodhue, D. L., Lewis, W., & Thompson, R. (2012). Does PLS have advantages for small sample size or non-normal data?. MIS Quarterly, 36(3), 981-1001. https://doi.org/10.2307/41703490

Haffer, R., & Kristensen, K. (2010). People management as indicator of business excellence: The Polish and Danish perspectives. The TQM Journal, 22(4), 386-398. https://doi.org/10.1108/17542731011053316

Hair Jr, J. F., Sarstedt, M., Hopkins, L., & Kuppelwieser, V. G. (2014). Partial least squares structural equation modeling (PLS-SEM): An emerging tool in business research. European Business Review, 26(2), 106-121. https://doi.org/10.1108/EBR-10-2013-0128

Hair, J., Hult, G., Tomas, M., Ringle, C., & Sarstedt, M. (2017). A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM) (3rd ed.). Thousand Oaks, United States: Sage Publications Inc.

Hair, J., Ringle, C. M., & Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory and Practice, 19(2), 139-152. https://doi.org/10.2753/MTP1069-6679190202

Hamel, G., & Prahalad, C. K. (1990). The core competence of corporation. Harvard Business Review, 68(3), 79-91.

Hayes, A. F. (2013). Introduction to Mediation, Moderation, and Conditional Process Analysis: A Regression-Based Approach. New York, United States: Guilford.

Holland, J. (2010). Banks, knowledge and crisis: A case of knowledge and learning failure. Journal of Financial Regulation and Compliance, 18(2), 87-105. https://doi.org/10.1108/13581981011033961

Hosseini, M., & Owlia, M. S. (2016). Designing a model for measuring and analysing the relational capital using factor analysis: Case study, Ansar bank. Journal of Intellectual Capital, 17(4), 734-757. https://doi.org/10.1108/JIC-04-2016-0042

Joia, L. A. (2000). Measuring intangible corporate assets: Linking business strategy with intellectual capital. Journal of Intellectual Capital, 1(1), 68-84. https://doi.org/10.1108/14691930010371636

Joshi, M., Cahill, D., & Sidhu, J. (2010). Intellectual capital performance in the banking sector: An assessment of Australian owned banks. Journal of Human Resource Costing & Accounting, 14(2), 151-170. https://doi.org/10.1108/14691931311323887

Kasman, A. (2010). Consolidation and competition in the banking industries of the EU member and candidate countries. Emerging Markets Finance and Trade, 46(6), 121-139. https://doi.org/10.2753/REE1540-496X460608.

Kehelwalatenna, S., & Premaratne, G. (2014). Intellectual capital performance and its long-run behavior: The US banking industry case. New Zealand Economic Papers, 48(3), 313-333. https://doi.org/10.1080/00779954.2013.867796

Kianto, A., Andreeva, T., & Pavlov, Y. (2013). The impact of intellectual capital management on company competitiveness and financial performance. Knowledge Management Research & Practice, 11(2), 112-122. https://doi.org/10.1057/kmrp.2013.9

Klein, D. A., & Prusak, L. (1994). Characterising Intellectual Capital. Cambridge, MA: Centre for Business Innovation, Ernst and Young.

Klimontowicz, M. (2013). Aktywa niematerialne jako źródło przewagi konkurencyjnej banku (Intangibles as a source of competitive advantage). Warszawa, Poland: CeDeWU.

klimontowicz, m. (2016). Knowledge as a foundation of resilience on Polish banking market. Electronic Journal of Knowledge Management, 14(1), 58-72. Retrieved from www.ejkm.com

Kujansivu, P., & Lönnqvist, A. (2007). Investigating the value and efficiency of intellectual capital. Journal of Intellectual Capital, 8(2), 272-287. https://doi.org/10.1108/14691930710742844

Lee, H., & Choi, B. (2003). Knowledge management enablers, processes, and organisational performance: An integrative view and empirical examination. Journal of Management Information Systems, 20(1), 179-228. https://doi.org/ 10.1080/07421222.2003.11045756

Lev, B. (2001). Intangibles: Management, Measurement, and Reporting. Washington DC, USA: The Brookings Institution.

Łupina‐Wegener, A. A. (2013). Human resource integration in subsidiary mergers and acquisitions: Evidence from Poland. Journal of Organizational Change Management, 26(2), 286-304. https://doi.org/10.1108/09534811311328353

MacKinnon, D. P. (2008). Introduction to Statistical Mediation Analysis. Mahwah, United States: Earlbaum.

Mavridis, D. G., & Kyrmizoglou, P. (2005). Intellectual capital performance drivers in the Greek banking sector. Management Research News, 28(5), 43-62. https://doi.org/10.1108/01409170510629032

McElroy, M. (2002). The new knowledge management. In M. W. McElroy (Ed.) Complexity, Learning and Sustainable Innovation (pp. 3-13). Burlington, United Kingdom: Butterworth-Heineman.

McFerrin, L. (2013). HDMD: Statistical analysis tools for High Dimension Molecular Data (HDMD). Retrieved from https://CRAN.R-project.org/package=HDMD

Mention, A. L., & Bontis, N. (2013). Intellectual capital and performance within the banking sector of Luxembourg and Belgium. Journal of Intellectual Capital, 14(2), 286-309. https://doi.org/10.1108/14691931311323896

Mohammed, A. A., & Irbo, M. M. (2018). Intellectual capital and firm performance nexus: Evidence from Ethiopian private commercial banks. International Journal of Learning and Intellectual Capital, 15(3), 189-203. https://doi.org/10.1504/IJLIC.2018.094723

Mondal, A., & Ghosh, S. K. (2012). Intellectual capital and financial performance of Indian banks. Journal of Intellectual Capital, 13(4), 515-530. https://doi.org/10.1108/14691931211276115

Murthy, V., & Mouritsen, J. (2011). The performance of intellectual capital: Mobilising relationships between intellectual and financial capital in a bank. Accounting, Auditing & Accountability Journal, 24(5), 622-646. https://doi.org/10.1108/09513571111139120

Nawaz, T., & Ohlrogge, O. (2022). Clarifying the impact of corporate governance and intellectual capital on financial performance: A longitudinal study of Deutsche bank (1957–2019). International Journal of Finance and Economics, 21 April 2022. https://doi.org/10.1002/ijfe.2620

NBP (2007-2020), Rozwój system finansowego w Polsce (The development of Polish financial system). National Bank of Poland. Retrieved from https://www.nbp.pl/home.aspx?f=/systemfinansowy/rozwoj.html

Neves, E., & Proença, C. (2021). Intellectual capital and financial performance: Evidence from Portuguese banks. International Journal of Learning and Intellectual Capital, 18(1), 93-108. https://doi.org/10.1504/IJLIC.2021.113658

Obłój, K. (2007). Strategia organizacji (Organisation strategy). Warszawa, Poland: Polskie Wydawnictwo Ekonomiczne.

OECD. (1996). The knowledge-based economy. Retrieved from https://www.oecd.org/officialdocuments/publicdisplaydocumentpdf/?cote=OCDE/GD%2896%29102&docLanguage=En

Özkan-Günay, E. N., Günay, Z. N., & Günay, G. (2013). The impact of regulatory policies on risk taking and scale efficiency of commercial banks in an emerging banking sector. Emerging Markets Finance and Trade, 49(sup5), 80-98. https://doi.org/10.2753/REE1540-496X4905S505

Petty, R., & Guthrie, J. (2000). Intellectual capital literature review: measurement, reporting and management. Journal of Intellectual Capital, 1(2), 155-176. https://doi.org/10.1108/14691930010348731

Phusavat, K., & Kanchana, R. (2007). Competitive priorities of manufacturing firms in Thailand. Industrial Management & Data Systems, 107(7), 979-996. https://doi.org/10.1108/02635570710816702

Poh, L. T., Kilicman, A., & Ibrahim, S. N. I. (2018). On intellectual capital and financial performances of banks in Malaysia. Cogent Economics and Finance, 6(1), 1-15. https://doi.org/10.1080/23322039.2018.1453574

Porter, M. E. (1990). The Competitive Advantage of Nations. New York, United States: Free Press.

Rehman, A. U., Aslam, E., & Iqbal, A. (2022). Intellectual capital efficiency and bank performance: Evidence from Islamic banks. Borsa Istanbul Review, 22(1), 113-121. https://doi.org/10.1016/j.bir.2021.02.004

Revelle, W. (2013). Procedures for Personality and Psychological Research. Retrieved from http://personality-project.org/r/psych-manual.pdf

Roldán, J. L., & Sánchez-Franco, M. J. (2012). Variance-based structural equation modeling: Guidelines for using partial least squares in information systems research. In M. Mora, O. Gelman, A. Steenkamp, & M. Raisinghani (Eds.), Research Methodologies, Innovations and Philosophies in Software Systems Engineering and Information Systems. Hershey: IGI Global.

Roos, G., & Roos, J. (1997). Measuring your company’s intellectual performance. Long Range Planning, 30(3), 413-426. https://doi.org/10.1016/S0024-6301(97)90260-0

Roos, G., Bainbridge, A., & Jacobsen, K. (2001). Intellectual capital analysis as a strategic tool. Strategy Leadership, 29(4), 21-28. https://doi.org/10.1108/10878570110400116

Rumelt, R. P. (1991). How much does industry matter?. Strategic Management Journal, 12(3), 167-185. https://doi.org/10.1002/smj.4250120302

Saymeh, A., Arikat, H., Hashem, F., & Al-Khalieh, A. (2021). Intellectual capital effectiveness of Jordanian banks financial performance. WSEAS Transactions on Business and Economics, 18, 552-568. https://doi.org/10.37394/23207.2021.18.56

Schiavone, F., Meles, A., Verdoliva, V., & Del Giudice, M. (2014). Does location in a science park really matter for firms’ intellectual capital performance?. Journal of Intellectual Capital, 15(4), 497-515. https://doi.org/10.1108/JIC-07-2014-0082

Schiuma, G., & Lerro, A. (2008). Intellectual capital and company’s performance improvement. Measuring Business Excellence, 12(2), 3-14. https://doi.org/10.1108/13683040810881153

Shaikh, J. M. (2004). Measuring and reporting of intellectual capital performance analysis. Journal of American Academy of Business, 4(1/2), 439-448.

Shih, K. H. (2008). Is e-banking a competitive weapon? A causal analysis. International Journal of Electronic Finance, 2(2), 180-196. https://doi.org/10.1504/IJEF.2008.017539

Shih, K. H., Chang, C. J., & Lin, B. (2010). Assessing knowledge creation and intellectual capital in banking industry. Journal of Intellectual Capital, 11(1), 74-89. https://doi.org/10.1108/14691931011013343

Shiu, H. J. (2006). The application of the value added intellectual coefficient to measure corporate performance: evidence from technological firms. International Journal of Management, 23(2), 356-365.

Singh, S., Sidhu, J., Joshi, M., & Kansal, M. (2016). Measuring intellectual capital performance of Indian banks: A public and private sector comparison. Managerial Finance, 42(7), 635-655. https://doi.org/10.1108/MF-08-2014-0211

Skowron, L., & Kristensen, K. (2012). The impact of the recent banking crisis on customer loyalty in the banking sector: Developing versus developed countries. The TQM Journal, 24(6), 480-497. https://doi.org/10.1108/17542731211270052

Soewarno, N., & Tjahjadi, B. (2020). Measures that matter: An empirical investigation of intellectual capital and financial performance of banking firms in Indonesia. Journal of Intellectual Capital, 21(6), 1085-1106. https://doi.org/10.1108/JIC-09-2019-0225

Stewart, T. A. (1997). Intellectual Capital: The New Wealth of Organizations. New York, United States: Doubleday/Curency.

Subramanian, A., & Nilakanta, S. (1996). Organisational innovativeness: Exploring the relationship between organisational determinants of innovation, types of innovations, and measures of organisational performance. Omega, 24(6), 631-647. https://doi.org/10.1016/S0305-0483(96)00031-X

Tseng, K. A., Lan, Y. W., Lu, H. C., & Chen, P. Y. (2013). Mediation of strategy on intellectual capital and performance. Management Decision, 51(7), 1488-1509. https://doi.org/10.1108/MD-03-2012-0143

Umanto, Wijaya, C., & Atmoko, A. W. (2018). Intellectual capital performance of regional development banks in Indonesia. Banks and Bank Systems, 13(3), 36-47. https://doi.org/10.21511/bbs.13(3).2018.04

Walsh, K., Enz, C. A., & Canina, L. (2008). The impact of strategic orientation on intellectual capital investments in customer service firms. Journal of Service Research, 10(4), 300-317. https://doi.org/10.1177/1094670508314285

Williams, K. C., & Page, A. R. (2011). Marketing to generations. Journal of Behavioural Studies in Business, 3(1), 37-53. Retrieved from http://www.aabri.com/jbsb.html

Xu, J., Haris, M., & Yao, H. (2019). Should listed banks be concerned with intellectual capital in emerging Asian markets? A comparison between China and Pakistan. Sustainability, 11(23), 6582. https://doi.org/10.3390/su11236582

Yaseen, H., & Al-Amarneh, A. (2021). Intellectual capital and financial performance: Case of the emerging market banks. Journal of Governance and Regulation, 10(1), 35-41. https://doi.org/10.22495/jgrv10i1art4

Zineldin, M. (1996). Bank strategic positioning and some determinants of bank selection. International Journal of Bank Marketing, 14(6), 12-22. https://doi.org/10.1108/02652329610130136

Zubac, A., Hubbard, G., & Johnson, L. W. (2010). The RBV and value creation: A managerial perspective. European Business Review, 22(5), 515-538. https://doi.org/10.1108/09555341011068921

Abstrakt