Received 2 June 2021; Revised 25 August 2021, 12 October 2021, 23 November 2021; Accepted 8 December 2021.

This is an open access article under the CC BY license (https://creativecommons.org/licenses/by/4.0/legalcode).

Vuong Khanh Tuan, Malaysia University of Science and Technology, Block B, Encorp Strand Garden Office, No. 12, Jalan PJU 5/1, Kota Damansara, 47810 Petaling Jaya, Selangor Darul Ehsan, Malaysia, e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

Premkumar Rajagopal, Malaysia University of Science and Technology, Block B, Encorp Strand Garden Office, No. 12, Jalan PJU 5/1, Kota Damansara, 47810 Petaling Jaya, Selangor Darul Ehsan, Malaysia, e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

Abstract

PURPOSE: The purpose of this study is to aid the small- and medium-sized enterprise (SME) sector in Ho Chi Minh City (HCMC), resulting in enhancement, improved management performance, and sustainability in adopting beneficial competitive practices aligned to the new era. The study was conducted to determine the key managerial factors that affect the performance of Vietnamese SMEs. We analyzed factors like business planning, organizational commitment, strategy implementation, and managerial control, adopting the budget process as the mediating factor, as it was determined to positively affect SME performance. METHODOLOGY: In the pilot study, we collected 105 samples using the convenience technique and analyzed the results to examine and validate the reliability of the research instrument. A quantitative approach was used in the pilot study, which tested for reliability using Cronbach’s alpha and exploratory factor analysis (EFA) with the software IBM SPSS 20.0. The real study was conducted using quantitative analysis, where the randomization technique was applied to 403 suitable samples. A full quantity of data was tested using Cronbach’s alpha, confirmatory factor analysis (CFA), and EFA. Structural equation modelling (SEM) was used to test both the conceptual framework and the hypothesis of the real study. This study was conducted from October 2016 to June 2020. FINDINGS: Analysis of SMEs identified the mediating factor, budget process, as having a significant effect on the dependent factor, SME performance. Regarding the total effect on SME performance, among four independent variables, the variable with the highest positive total effect on SME performance was strategy implementation. The second highest positive total effect on SME performance was organizational commitment; the third highest positive total effect was business planning; and the fourth was managerial control. Therefore, it can be concluded that when SME managers change these key factors, they will change the level of performance for their enterprises. IMPLICATIONS: This research provides insight into the performance management of SMEs and how managerial factors affect the level of this performance management. In the results of study, the following key factors have been identified: strategy implementation, organizational commitment, business planning, managerial control, and the mediating role of the budget process. These independent variables have significant total effects on SME performance, and the theory’s implication builds on performance management to contribute to the field of management. This research model can be applied to management practices to restructure, innovate, and improve the overall performance of SMEs. Additionally, this study will provide SMEs with management procedures to compete, adapt, and enhance their sustainability within the global market. ORIGINALITY/VALUE: This model provides researchers and practitioners with the invaluable knowledge needed to manage enterprise performance, which will assist SMEs in developing as sustainable and competitive players in this new era.

Keywords: SMEs, performance management, strategy implementation, organizational commitment, business planning, managerial control, budget process, Vietnam

INTRODUCTION

Small- and medium-sized enterprises (SMEs) have made substantial contributions to the economic development of many countries (Chu, 2015; Ngo, 2016; Shamsudeen & Hassan, 2016; Lam, 2017; Nguyen, Khuu, & Nguyen, 2018; Tran, 2019). Thus, there is a need to study the management process and its impact on Vietnamese SME performance and to review the current status of these SMEs against trends in global integration (Nguyen, 2019). Additionally, in Vietnam, SMEs account for approximately 98% of businesses (Nguyen, Khuu, & Nguyen, 2018): their role in supporting the national economy and society is pivotal. SMEs are considered important contributors to ongoing economic development, generating a higher level of employment and additional opportunities (Chu, 2015; Ngo, 2016; Lam, 2017; Nguyen, Khuu, & Nguyen, 2018; Tran, 2019; Nguyen, 2019). Phan et al. (2015) and Nguyen (2019) similarly state that SMEs contribute to job creation and enhanced incomes for the Vietnamese. These are recognized as critical elements in economic development and encourage various social resources, inviting investment and development, and leading to a reduction in poverty.

The current overall capability of businesses and their management are faced with limitations in their skills and capacities to compete in highly competitive global markets; these limitations will be the challenges faced by Vietnamese SMEs (Ngo, 2016; Nguyen, 2019). In order to adapt and be competitive in global markets, Vietnamese SMEs should develop and adopt management innovations (Chu, 2015; Tran, 2016; Nguyen, 2019). Due to these identified management limitations, Vietnamese SMEs should review and realign their corporate vision and managerial procedures and develop strategies to provide sustainability with innovative, positive, and realistic measures to provide growth within the sphere of international integration.

Additionally, budget processes are part of the management process, supporting SME performance (Nguyen, 2019). In Vietnam, the overall budget process has limited effect due to many Vietnamese SMEs only being partially committed to its implementation (Chu, 2015; Tran, 2016). Upgrades are required to ensure the mediating role of the budget process provides additional performance growth for SMEs (Nguyen, 2019). However, the commitment to improved budget planning in Vietnamese SMEs remains limited (Chu, 2015; Nguyen, 2015; Nguyen, 2019). Overall, effective budgetary planning is a key factor in the actual outcome of all businesses (Chu, 2015; Tran, 2016; Nguyen, 2019). The previous synthesis analysis states that the mediating role of the budget process is critical in the management of cash flow and overall financial position within SMEs, and management needs to adopt significant enhancements to improve their performance.

Overall, performance management plays a crucial role in indicating all relevant values of the enterprises. However, the measurement processes of finance and their limitations, the performance measurement of enterprises should incorporate both financial and non-financial aspects (Luu, 2010; Ibrahim et al., 2012; Mashovic, (2018); Nguyen, 2019). The limitations of financial statements are due to intangible assets not being recorded (Bragg 2018). Moreover, financial indicators can only show results of the performance from an organization’s past; they do not forecast the enterprise’s future (Okoye, Odum, & Odum, 2017). Therefore, there is a need to review and study the overall performance management, including financial and non-financial.

As noted, the SME sector provides a significant contributing role in supporting the socio-economic development of Vietnam; this sector requires continuous research to identify additional benefits for growth development. However, Vietnamese SMEs currently are limited in management capacity and need to improve their level of overall performance management to improve their competitive advantages globally. Therefore, this study focuses on the mediating role of the budget process with the support of the management process including business planning, organizational commitment, strategy implementation, and managerial control on SME performance. This study will provide suggestions for future additional improvements, enhancements, and growth to improve Vietnamese SMEs’ overall performance management and enhance their competitiveness in global markets.

LITERATURE REVIEW

General systems theory and organizational performance

General systems theory was developed by Austrian biologist Ludwig Von Bertalanffy in the 1930s. According to Kihara (2016), in general systems theory all the components of an organization are interlinked; changing one variable brings flow-on changes to other variables. Assessing the theory of a general system, SMEs need a relationship between independent variables and the dependent variable (SMEs’ overall performance). Three key organizational resources that impact SME performance include physical, human interaction, and financial strength.

Organizational performance is described as an organization’s ability to acquire and utilize its resources and valuables as expeditiously as possible in the pursuit of its operating goals (Griffins, 2006). Organizational performance specifically measures integration performance, relative to financial and nonfinancial performance indications (Luu, 2010; Qi, 2010; Ibrahim et al., 2012; Santos & Brito, 2012; Peronja, 2015; Nguyen, 2019). The nonfinancial performance system is developed as a consequence of the shortages in financial-based performance measures (Ahmad & Zabri, 2016). In general, to improve overall performance, it is necessary to focus on, review, and apply both financial and non-financial indicators within SMEs. Balancing both financial and non-financial indicators provides full value to SMEs, assists in gaining competitive advantages, and supports sustainable development.

A review of the managerial factors with the mediating role of the budget process on the performance of SMEs

The budget process and its mediating role in SME performance

The budget process (BP) is part of the overall management process, including planning. Budgets can serve as a tool to forecast profitability, allocate resources, or communicate specific knowledge from one part of an organization to other sectors of the business. All task efforts are connected to the budget (Ax, Johansson, & Kullvén, 2002) which can be divided into three phases: budget development; budget guidance; and budget review and tracking. As a consequence, the budget process mediates the allocation and implementation of the management process.

The asymmetric information theory and the human factor in the overall planning budget process contribute to an enterprise’s performance. The theory of asymmetric information originated in 1970 and was then implemented in modern economic sciences. The three economists who had a particular influence in developing asymmetric information theory were George Akerlof, Michael Spence, and Joseph Stiglitz, sharing the Nobel Prize in economics in 2001 for their earlier contributions. Asymmetric information can occur in economic negotiation, accounting activities; and communication between non-executive employees and executive management. In asymmetric information, those who possess information are divided into two distinct groups (managers and subordinates), or the information asymmetry is regarded as the difference in the amount of information possessed by the superior and the subordinate (Zainuddin et al., 2008). Additionally, according to Putri and Solikhah (2018), information asymmetry means that the relative difference in information retained by different parties pertaining to the same specific activity within the organization creates an imbalance in the group.

Considering the benefits of the budget process, there are also some limitations when implementing it, as the planning of a budget is tasked by people, and they can instill influences that can generate side-effects impacting the outcomes of the planned budget. The budget process has benefits and limitations that arise from human factors and one of the identified issues for administrators was the potential creation of an information gap within the budget process, reducing the correctness and suitability of the budget. When utilizing asymmetric information, budget planners may be relying on higher levels of contribution from direct employees than their supervisors; direct employees have intimate and specific information to develop the overall decisions relative to the budgetary plan (Yuen & Cheung, 2003). To achieve the development of a suitable budget, it is critical that the combined contributions from management and employees are considered to avert or minimize the level of asymmetric information.

According to Zainuddin et al. (2008), the lack of ideal information could bias managers to perceive uncertainly within a specific environment. Thus, the lack of reliable information is a handicap for managers within a specific environment. Similarly, unreliable information will result in gaps in the budget plan, impacting performance in manufacturing and business activities. The leaders of all businesses, including those at SMEs, prefer that the budgeting process be guided through all levels, including suitable levels of funding, transparency, and accountability (Kimunguyi, Memba, & Njeru, 2015). Putri and Solikhah (2018) contribute that information supplied by subordinates is considered more relevant than information from managers (there is asymmetric information); the contribution by subordinates is historically incomplete, and they can only provide an underestimated budget. Therefore, to achieve concise budget targets for all the enterprise’s nominated activities, there is a need to combine the contributions of its employees and management.

The budget plays a major role in the performance of businesses (Pimpong and Laryea, 2016), providing the mediating role in allocating all the activities within SMEs and contributing to their overall performance (Nguyen, 2019). To maintain their current competitive advantages, SMEs must constantly seek to maximize their effectiveness and efficiency in the overall budget control process (Yee et al., 2016). The connection between budgetary participation and managerial performance is of particular interest in accounting and management fields (Govindarajan, 1986; Dunk, 1993; Nouri & Parker, 1998; Rachman, 2014; Ogiedu, Killian & Odia, 2013; Li, Nan, & Mo, 2010; Hariyanto, 2018; Susanti, Eprillison, & Jolianis, 2018; Badu, Awaluddin, & Mas’ud, 2019). The applied theory of budget participation is a key factor in increasing the effectiveness and efficiency of the budgets of enterprises, providing an additional increase in managerial performance (Manafe & Setyorini, 2019). As identified in the previously notes theories and related studies, there is a strong relationship between the budget process and the performance of SMEs. Given this, the related hypothesis is as follows:

H5: There is a significant relationship between the budget process and

The relationship between business planning and the budget process towards SME performance

Planning is the first element of the overall management process for enterprises of all sizes. Planning forms part of the theory of management and involves setting goals, establishing strategies to achieve those goals, and developing plans to integrate and coordinate activities. Most studies focus on exploring the relationship between strategic planning and the enterprise’s performance, including financial performance (Nzewi & Ojiagu, 2015; Gomera et al., 2018; Omotayo et al., 2018). Business plans (BP) are considered a significant tool for securing suitable finance, forming alliances, developing the enterprise’s direction, and measuring performance (Burns & Dewhurst, 1990). An effective business plan will support an enterprise’s growth, helping it manage financial cash flow and develop its implementation plan (Yulia, 2017).

Brinckmann et al. (2010) stated that business planning utilizes systematic and oriented predictions, which provide suggestions for process options. It is considered pivotal in enhancing an enterprise’s success due to its high impact on profitability, stability, and elevating the enterprise’s market level (Yulia, 2017). According to Nguyen (2019), the objective of business planning is to develop all management activities for each sector, including manufacturing, operations, and sales. Business planning and managerial control relative to the firm’s performance are major contributors towards the overall management process (Nguyen, 2019). Ibrahim (2019) stated that a suitably defined plan guides the outcomes of goals, provides additional guidance on the allocation and implementation of resources, and provides planned and measurable outcomes. According to Nguyen (2019), business planning is pivotal in supporting the performance of SMEs. In conclusion, the related hypothesis is as follows:

H1b: There is a significant relationship between business planning and

SME performance.

According to Van (2015), budgeting is defined as the process of quantifying the elements of each budget into an actionable plan, with a timeline proposed by management and their employees to guide and assist in the coordination of tasks towards implementation. The relationship between business planning and the mediating role of budgeting is a significant and critical factor in implementing business strategy, control, and continued organization management (Nguyen, 2019). A strengthened connection between the two factors allows SMEs to realize maximum performance in business and overall management activities. The related hypothesis is as follows:

H1a: There is a significant relationship between business planning and the

budget process.

The relationship between organizational commitment and the budget process towards SME performance

The culture of an enterprise is related to its overall management process, and the role of organizational commitment (OC) provides significant support to SME performance. Strengthening the commitment of enterprises is a key factor in the improvement of an enterprise’s growth and development (Princy & Rebeka, 2019). Porter, Steers, Mowday, and Boulian (1974) note that organizational commitment identifies employees’ level of commitment to the organization as well as how they identify with an organization’s values and goals; organizational commitment is the connection of management with their subordinates. With a strong, loyal commitment to the organization, a united focus of working towards a common goal, striving to attain higher results in the long-term for its enterprise (Abdul, 2008). Additionally, Zefeiti and Mohamad (2017) state that organizational commitment facilitates a relationship with and acceptance of the enterprise, inclusive of its goals and values. According to Khan, Ziauddin, & Ramay (2010), as the level of organizational commitment grows, corresponding positive outcomes grow in parallel; high levels of commitment are strongly linked to high levels of achievement in organizational performance. Organizational commitment has developed as a theory and study (Porter et al., 1974; Steers, 1977; Allen & Meyer, 1990, Meyer & Allen, 1991; Batilmurik et al., 2019).

Organizational commitment is linked to an enterprise’s performance or departmental performance (Recep et al., 2010; Moshood et al., 2019). When considering either affective, continuance or normative commitment, employee commitment has a critical influence on the performance of an enterprise (Moshood et al., 2019). In summary, organizational commitment plays a key role in SME performance, based on its partnered link. Based on information generated theory and related studies. The related hypothesis is as follows:

H2b: There is a significant relationship between organizational

commitment and SME performance.

According to Wong-On-Wing, Guo, and Lui (2010) and Rachman (2014), organizational commitment impacts participation within the overall budgeting process. When enterprises promote a higher level of commitment from individuals, the outcomes achieved are correspondingly higher. According to Ardiansyah, Isnurhadi, and Widiyanti (2019), to attain budget targets that produce high managerial performance, consideration must be given to ways to achieve organizational commitment. According to Nouri and Parker (1998), there is a strong link between budget participation and organizational commitment. The budget process can provide overall improvement to subordinates’ cultural belief, sense of agency, and solid involvement with an organization, bringing them into alignment and commitment to the defined budgets of the organization. Based on this synthesis analysis, the related hypothesis is as follows:

H2a: There is a significant relationship between organizational

commitment and the budget process.

The relationship between strategy implementation and the budget process towards SME performance

Ngugi et al. (2017) stated that strategy implementation (SI) is relative to an organization’s resources as well as its employees’ positive motivation in achieving its objectives. To achieve a successful strategy implementation, an enterprise should develop effective internal systems and processes to improve organizational performance; define future direction; assign teamwork resources based on expertise; deal effectively with organizational changes and uncertainties in external environments; and define processes for decision-making and prioritizing (Donna, 2018).

Successful strategy implementation requires contributions and cooperation from all levels of employees within an enterprise: Its effectiveness is impacted by the quality of people participating within the overall process (Obiero and Genga, 2018). Similarly, SI affects the whole organization and can only be successful if implemented and adopted throughout the entire organization (Weissenberger-Eibl et al., 2019); strategy implementation has a positive relationship with SME performance, if the enterprises possess well-developed and suitably strategic plans. Thus, strategy implementation is an important tool for an enterprise in achieving its objectives and goals. The hypothesis is as follows:

H3b: There is a relationship between strategy implementation and SME

performance.

The budget process plays a key role to allocate the cash-flow for providing the strategy implementation to achieve the goals and objectives of the enterprises. According to Doan et al. (2015), there are similarities in the relationship between implementation processes and overall budget processes. Combined information and opinions drawn from research, employees, and managerial contributions, define the enterprise’s overall goals and objectives. The budget is the primary tool for the enterprise to successfully implement its business plans and strategies. According to Mihaila, Ghedrovici, and Badicu (2015), budgets play a critical role in strategy implementation; budgets that are well-developed can generate significant benefits. Budgeting provides the foundation for all successful businesses (Banks, 2018). The role of the budget process is critical in the allocation of tasks and their implementation and in providing a higher level of performance in alignment with the strategies of SMEs. Based on the previous analysis, the related hypothesis is as follows:

H3a: There is a significant relationship between strategy implementation

and the budget process.

The relationship between managerial control and the budget process in SME performance

Control theory is the element of the overall management process. Its development as a theoretical discipline is linked to Planning and Control Systems: A Framework for Analysis, by Robert Anthony (1965). Managerial control assures management that assigned resources are utilized effectively and efficiently to attain an enterprise’s objectives. It assists in developing tools to measure performance (Anthony, 1965). There are several definitions of business managerial control related to industry, core business, organizational needs, and managerial style (Lakis & Giriunas, 2012; Suárez, 2017).

According to Cambalikova and Misun (2017), control is a process where managers ensure that financial budgets are defined and applied to selected task elements to align with the goals and objectives of an enterprise. Managerial control ensures management directives are carried out. Its employees adopt ongoing assigned tasks, ensuring proper operational execution, developing a culture of promoting accuracy and quality completion, and providing reliable processing of financial transactions (Eke, 2018).

Jones, George, and Hill (1998) state that control is regarded as a key function, providing accuracy in measurement, monitoring, and evaluation processes that achieve the goals and objectives of an enterprise. Vietnamese SMEs need to focus on managerial control to improve overall performance in attaining business targets (Nguyen, 2019). Managerial control would assist in realizing inherent problems within an SME, providing managerial review and adjustments to correct problems such as sub-standard levels of performance. Based on the research and discussions from the above analysis, the related hypothesis is as follows:

H4b: There is a significant relationship between managerial control and

SME performance.

There is a close link between managerial control and the budget process within overall business management, which impacts upon the enterprise’s overall performance and minimizes unforeseen risks. These two functions – managerial control and the budget process – have a close relationship that requires constant refinement. The overall budget process plays a significant role in the performance of any enterprise. Budgeting provides internal controls for the implementation of planning through the processing of defined costs, thus ensuring suitable annual appropriation of finances is secured (Omosidi et al., 2019). In general, the budget process is critical in the activities of an enterprise; it is linked with managerial control in overall performance. Based on the concepts and arguments presented above, the related hypothesis is as follows:

H4a: There is a significant relationship between managerial control and the budget process.

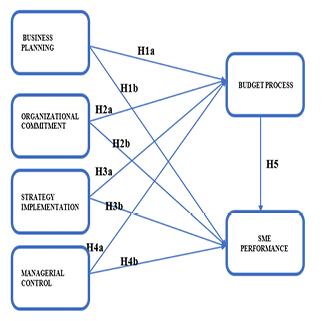

Figure 1 presents the conceptual framework and hypotheses for this study.

Figure 1. Conceptual framework and hypotheses for this study

METHODOLOGY

According to Ward (2019), an SME is identified as a business that maintains its revenues, assets, or number of employees below the threshold of what is considered a large company. The definition of an SME differs between countries and industries. Legally registered Vietnamese SMEs are divided into three levels: micro, small, and medium-size. Our research focuses on Vietnamese SMEs within the manufacturing sector, specifically in Ho Chi Minh City (HCMC). According to the Decree of the Vietnamese Government (2009), SMEs can be identified according to two standards: capital and the number of employees. This study focuses on SMEs that employed over 10 persons but less than 200 (small enterprises); and greater than 200 persons up to 300 (medium-sized enterprises); there was no research review of micro enterprises.

The study incorporates two stages: the pilot study and the real study. The pilot study proves the reliability of the questionnaires for dependent, mediating, and independent variables. The purpose of the pilot study was to assess the reliability of the overall instruments being used within the real study. A quantitative approach used in the pilot study tested for reliability using Cronbach’s alpha, exploratory factor analysis (EFA) by software IBM SPSS 20.0. The questionnaire distribution for the pilot study was 135 data samples. Questionnaire returns were 115. Valid questionnaires for analysis in the pilot study provided 105 data samples. The 105 data samples were scrubbed to remove the missing data after imputing it for the analysis. Data from the pilot study were not applied to the real study.

Data collection for the real study began with the distribution of 495 questionnaires. Of these, 429 were returned, and 403 were validated for use in analysis; the validity rate was 93.548%. The random technique was used for collection. The real study was conducted with a full quantity of data to test using Cronbach’s alpha; confirmatory factor analysis (CFA) was also utilized, as was EFA. Structural equation modelling (SEM) was used to test both the conceptual framework and the hypothesis of the real study (see Figure 1).

The scales of measurement for the study were: business planning, organizational commitment, strategy implementation, and managerial control. These were measured with a 5-degree Likert scale from ‘1: Strongly disagree’ to ‘5: Strongly agree.’ The budget process and SME performance were measured by Likert from ‘1: Least effective’ to ‘5: Most effective.’

RESULTS

Pilot study: The results from analysing the reliability of the scales of measurement for the factors business planning, organizational commitment, strategy implementation, managerial control, the budget process, and SME performance, with all coefficients for Cronbach’s alpha was greater than 0.8. Reliability of the scales of measurement was accepted. The only non-accepted item was P3, because the corrected items total correlation was identified as being less than 0.5 (it was 0.302). All observed variables were grouped by individual factor; only item SI2 was separated, re-classified into the factor of strategy implementation, and removed (this was done by EFA). In conclusion, there were only two removed items, SI2 and P3 (‘SI2: Managers need to be proactive in planning implementation’ and ‘P3: Budgetary motivation is derived from the setting of budget goals’); these were not applied in the real study.

Real study: 403 complying data samples were collected for analysis.

Synthesis of Cronbach’s alpha of all factors

The data in Table 1 identifies the observed variables scales of measurement applied to the following factors: business planning, organizational commitment, strategy implementation, managerial control, the budget process, and SME performance. The results from analyzing the reliability of the scales of measurement (the coefficient of Cronbach’s alpha) for all factors are > 0.8. Concurrently, the observed variables also have the corrected item-total correlation > 0.5. Therefore, all observed variables of the scales of measurement factors meet the reliability requirements and are utilized in the preceding steps of the study.

Table 1. Synthesis of Cronbach’s alpha of all factors

|

Factors |

Cronbach’s alpha |

Evaluation |

|

Business planning (PL) |

0.925 |

Accepted |

|

Organizational commitment (OC) |

0.921 |

Accepted |

|

Strategy implementation (SI) |

0.886 |

Accepted |

|

Managerial control (CL) |

0.896 |

Accepted |

|

Budget process (BP) |

0.935 |

Accepted |

|

SME performance (P) |

0.905 |

Accepted |

Exploratory factor analysis (EFA)

Data was analyzed using the Kaiser-Meyer-Olkin measure of sampling adequacy (KMO) and Barlett’s test. The results of EFA processed with the software SPSS 20.0 and the coefficient of KMO was 0.933 > 0.05, and Bartlett’s test of sphericity produced the statistic meaning with a Sig. of 0.000 < 0.05.

The explained variance of 63.381% > 50% complies with the required standards. It identifies that 63.381% of changes from five factors extracted are explained by observed variables. The results in the rotated component matrix, it is evidenced that all the factors have their discriminant validity and the observed variables of the individual factor grouped into separate groups. The observed variables in each factor have correlations that contribute relevance to each factor. The factor loading of each observed variable is > 0.6. Therefore, the EFA was satisfied and met the required standard.

Confirmatory factor analysis (CFA)

Table 2 identifies that CMIN/DF= (<2), TLI and CFI exceeded 0.9, and RMSEA= 0.041 (< 0.05), indicating the model has significant value. Therefore, the model comparatively aligns with the data. To obtain significant results, the researcher considered issues related to the reliability of the following scales of measurement: Cronbach’s alpha (CA), composite reliability (CR), and average variance extracted (AVE).

Table 2. Index for evaluating the suitability of the model with research data

|

Evaluating index |

Value |

|

CMIN/DF |

1.676 |

|

TLI |

0.936 |

|

CFI |

0.940 |

|

RMSEA |

0.041 |

The reliability of scales of measurement was evaluated by three indexes: composite reliability, average variance extracted, and Cronbach’s alpha. The scales of measurement were estimated to have reliability of CR > 0.5, and AVE has meanings with value > 0.5 (Hair et al., 1992; Le, 2016). Table 3 demonstrates that indexes with CR > 0.5, AVE > 0.7, and Cronbach’s alpha of all factors were > 0.7. The results of the analysis and evaluation revealed that all the scales of measurement achieved validity and reliability. All the results of the CFA were suitable since all the models of the CFA were suitable for the market data without any adjustments, and there was no instance of minus variance.

Table 3. Cronbach’s alpha, composite reliability (CR), and average variance extracted (AVE).

|

Factors |

Cronbach’s alpha |

CR |

AVE |

|

Budget process |

0.935 |

0.936 |

0.622 |

|

Business planning |

0.925 |

0.926 |

0.584 |

|

Organizational commitment |

0.921 |

0.924 |

0.578 |

|

Strategy implementation |

0.886 |

0.889 |

0.537 |

|

Managerial control |

0.896 |

0.898 |

0.563 |

|

SME performance |

0.905 |

0.906 |

0.517 |

Analyzing structural equation modeling (SEM)

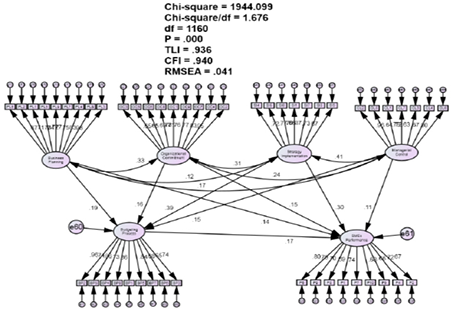

Based on the index in Figure 2, it was concluded that the model fits well with the data: CMIN/df = 1.676 (<2); TLI = 0.936 (>0.9); CFI = 0.940 (>0.9); and RMSEA = 0.041 (<0,05). The estimated results of parameters presented in Table 4 show that all relationships have the statistical meanings.

Figure 2. Results of SEM (standardized)

The results in Table 4 identify that the p-value of all factors is < 0.05; moreover, they estimate (unstandardized) that all factors significantly impact SME performance; thus, all hypotheses are supported. The table demonstrates that all relationships of independent factors or mediating factors impact dependent factors (SME performance). Based on the P-value of estimates in Table 4, the P-value of all factors is <0.05; all correlations in SEM have statistical reliability of 95%. The factors business planning, organizational commitment, strategy implementation, managerial control, and the mediating factor of the budget process, all impact positively the dependent factor of SME performance.

Table 4. Regression weights

|

Regression weights: Group number 1 - default model |

|

|

Estimate |

S.E. |

C.R. |

P |

|

Budget process |

<--- |

Business planning |

0.16 |

0.039 |

4.143 |

*** |

|

Budget process |

<--- |

Organizational commitment |

0.16 |

0.047 |

3.401 |

*** |

|

Budget process |

<--- |

Strategy implementation |

0.591 |

0.082 |

7.186 |

*** |

|

Budget process |

<--- |

Managerial control |

0.162 |

0.053 |

3.083 |

0.002 |

|

SME performance |

<--- |

Business planning |

0.104 |

0.036 |

2.848 |

0.004 |

|

SME performance |

<--- |

Organizational commitment |

0.127 |

0.044 |

2.908 |

0.004 |

|

SME performance |

<--- |

Strategy implementation |

0.39 |

0.08 |

4.851 |

*** |

|

SME performance |

<--- |

Managerial control |

0.107 |

0.049 |

2.201 |

0.028 |

|

SME performance |

<--- |

Budget process |

0.148 |

0.051 |

2.93 |

0.003 |

The results in Table 5 indicate that when analyzing the SEM with standardized regression weights among the variables of the study, it verifies that all relationships relating to the independent factors or mediating factors impact on the dependent factor (SME performance) with the detail standardized regression weight in detail.

Table 5. Result of analyzing SEM with standardized regression weights

|

Standardized regression weights: Group number 1 - default model |

|

|

|

|

|

|

|

Estimate |

|

Budget process |

<--- |

Business planning |

0.189 |

|

Budget process |

<--- |

Organizational commitment |

0.162 |

|

Budget process |

<--- |

Strategy implementation |

0.393 |

|

Budget process |

<--- |

Managerial control |

0.148 |

|

SME performance |

<--- |

Business planning |

0.140 |

|

SME performance |

<--- |

Organizational commitment |

0.148 |

|

SME performance |

<--- |

Strategy implementation |

0.297 |

|

SME performance |

<--- |

Managerial control |

0.112 |

|

SME performance |

<--- |

Budget process |

0.170 |

Table 6 demonstrates that the budget process as a mediating factor has a significant effect on SME performance, with beta 0.170. Regarding the total effect on SME performance, among four management factors, the factor with the highest positive total effect on SME performance was strategy implementation, with beta 0.364. The second highest positive total effect on SME performance was organizational commitment (beta 0.175). The third highest positive total effect on SME performance was business planning (beta 0.173). The fourth highest positive total effect on SME performance was managerial control (beta 0.138).

Table 6. Direct, indirect, and total causal effects

|

|

Budget process |

SME performance |

||||

|

|

Direct |

Indirect |

Total |

Direct |

Indirect |

Total |

|

Managerial control |

0.148 |

- |

0.148 |

0.112 |

0.025 |

0.138 |

|

Strategy implementation |

0.393 |

- |

0.393 |

0.297 |

0.067 |

0.364 |

|

Organizational commitment |

0.162 |

- |

0.162 |

0.148 |

0.028 |

0.175 |

|

Business planning |

0.189 |

- |

0.189 |

0.140 |

0.032 |

0.173 |

|

Budget process |

- |

- |

- |

0.170 |

- |

0.170 |

DISCUSSION

For positive growth in their overall management, SMEs must adapt and maintain parity with the current global market, provide improvement for management processes, and focus on the budget process as the mediating role in improving SME performance. It is necessary for SMEs to enhance their performance and gain the benefits that arise from involvement in global markets. Detailed suggestions for achieving this are outlined in the following paragraphs.

Analysis of SMEs identified the mediating factor, budget process, as having a significant effect on the dependent factor, SME performance. The budget process plays an important role in providing calculations, proposals, detailed summaries that incorporate every relevant source, and resource allocation. It allows for multiple specific tasks to be implemented within a defined timeframe. Budget planning assigns the necessary resources to implement planned activities and defines plans for manufacturing, business, and management. The importance of budget accuracy depends on the enterprise’s manufacturing and business situation and the management team’s overall commitment level. High budget estimates will result in waste; low budgets will cause difficulties for employees creating implementation plans and impact outcomes. Therefore, planning a budget requires the cooperation of all internal division employees and management in discussing the relevant details. Once finalized, the budget should be adopted by all parties within the enterprise. The interconnecting functions of a strong SME management process require the use of an overall budget process, which provides a key element. This allows for the implementation of all activities to maximize the achievement and performance of the business organization’s strategic goals. The proposed budget should be aligned to the enterprise’s vision and mission statements. The budget needs to be specific and nominate the appropriate goals and objectives. Specific budgets should be distributed to all relevant departments, such as management, planning, operations, manufacturing, sales, and marketing. SMEs’ managers and employees need to improve their budget processes to achieve their goals and objectives, which might involve enhancing their budget analysis, development, and review procedures.

It should be noted that the factor with the highest positive total effect on SME performance was strategy implementation. Thus, SMEs should strongly focus on strategy implementation, including employee training, guidelines for strategy implementation, and organizational structure improvements, due to its flexibility with strategy implementation. SEM management should provide support and concise preparation for strategy implementation by applying good resources, infrastructure, and budget preparation; these elements are crucial in supporting their management and business.

As noted in the results, the second-highest positive total effect on SME performance was organizational commitment. Thus, SMEs should develop and provide competent overall commitment to their business through suitable levels of finance, corporate culture, good working environment, good leadership, well-developed policies, and good HR policies for their employees in an effort to inspire employees in their work performance.

Following organizational commitment, business planning was the third highest positive total effect on SME performance. There are numerous elements SMEs should include as they seek to improve performance: SME management should have a clear organizational vision and mission; planned goals and objectives need to be detailed and clearly identified. When developing business planning, there is a need for a deep understanding and knowledge of the current status of internal resources such as capital, raw material, inventory, technology, and human resources. Contributions are required from all internal levels to improve the knowledge of managers and commitment of all employees in developing their overall plans, budget preparation, market analysis, competitor analysis, potential customer lists. Additionally, management needs to allocate time for suitable levels of planning.

The fourth highest positive total effect on SME performance was managerial control. SME management should focus on the managerial control elements of tracking, measuring, and correcting activities to ensure compliance with business planning and strategy implementation. The management team analyses documents, employees’ knowledge, and the skills required to accomplish tasks.

SME performance includes financial and non-financial performance management, which are also critical in the success of an enterprise. It has been determined that SME performance includes both financial and non-financial indicators. Financial indicators are the measurements SMEs can use to achieve financial objectives, such as profits, budget goals, cost targets achieved quarterly, and growth in sales revenue, etc. Non-financial indicators include production or service output goals, customer feedback scores, growth in the customer base, delivering products or services on time, developing process management capabilities, and the improvement and innovation of targets, etc. Therefore, in organizational performance, both financial and non-financial performance management are critical to the success of an organization.

Finally, empirical analysis focuses on specific SMEs in the manufacturing sector. However, different kinds of manufacturing industries will have different characteristics, since they are facing different competitors. Further suggestions for SMEs include attention to the concept that the budget process and internal managerial skills are important in the performance of SMEs. However, the quality of products produced by SMEs and the price of these products would be important for competition. SMEs should improve the quality of their products and services in order to compete. Training programs for employees would be another important factor in the success of SMEs, updating employees’ skills to adapt to competitive markets. The financial management of SMEs is the third point to be taken into account. SMEs face difficulty in borrowing money from banks compared to large businesses, as they may lack the collateral requested by banks. The final recommendation is that local governments develop policies supporting SMEs in technology, management, and financial support, in order to promote the survival and sustainable development of SMEs in current markets.

CONCLUSION

The results demonstrate that the research model has validity. The independent variables and the mediating variable all have significant effects on the dependent variable (SME performance). All the hypotheses are accepted. Specifically, the SEM results illustrated that the independent variables of business planning, organizational commitment, strategy implementation, and managerial control have a positive direct and indirect effect on SME performance, and the mediating factor of the budget process has a significant and direct effect on SME performance. Regarding the total effect on SME performance, among four independent variables, the variable with the highest positive total effect on SME performance was strategy implementation. The second highest positive total effect on SME performance was organizational commitment; the third-highest positive total effect was business planning; and the fourth was managerial control. Analysis of SMEs identified the mediating factor, budget process, as having a significant effect on the dependent factor, SME performance. Therefore, when the management of SMEs in the manufacturing sector of HCMC changes these key factors, they also change the level of performance for their enterprises.

Additionally, this research focuses on the effects of independent variables, with the mediating role of the budget process, on SME performance. The findings suggest that the identified variables and the mediating role of the budget process have significant effects on SME performance. Addressing budget process issues will reflect positively on the overall outcomes of the enterprises. Therefore, SME management needs to focus on the mediating role of the budget process within the management process, and it is necessary to improve the mediating role of the budget process within SMEs to enhance overall performance.

The findings of this study suggest that strategy implementation is the variable with the highest positive total effect on SME performance. Therefore, when SMEs develop and implement their management processes, strategy implementation should be focused on as a priority to improve overall SME performance. The results also suggest that organizational commitment has the second highest positive total effect on SME performance. Therefore, organizational commitment is crucial for supporting SME performance. In the corporate governance process within SMEs, it is necessary to consider the role of organizational commitment to support overall performance. The third factor that has total effects on SME performance is business planning. Therefore, business planning plays a vital role in enhancing SME performance and requires attention. When developing and implementing the business planning process, analysis and review are necessary to ensure professionalism. The variable with the fourth-highest positive total effect on SME performance is managerial control. Managerial control plays a vital role in SME performance, as enhancing management will also improve an SME’s general performance level. Therefore, managerial control should be developed as a focus to enhance SME performance.

Limitations and direction for further research

There are several limitations to this study. The research was limited to data collected in HCMC, and this sample did not provide a comprehensive view of typical enterprises in Vietnam. Additionally, there is a lack of comparative research available from different regions and other diverse industries, which might have expanded the overall scope of this research. Administrators and future researchers can use this study as a base from which to expand the research by enriching the research variables and adding geographic scope, for example, by looking beyond HCMC into enterprises in broader regions of Vietnam. Further studies might conduct a comparative study by addressing different geographic and cultural areas. The outcomes would be realized when applied to SME performance management, providing suitable solutions for SMEs in various geographic and cultural areas of Vietnam.

Acknowledgment

This article is part of a Ph.D. thesis, specializing in Management, Malaysia University of Science and Technology.

References

Ahmad, K., & Zabri, S.M. (2016). The effect of non-financial performance measurement system on firm performance. International Journal of Economics and Financial Issues, 6(S6), 50-54. http://www.econjournals.com/index.php/ijefi/article/view/3149

Allen, N.J., & Meyer, J.P. (1990). The measurement and antecedents of affective, continuance and normative commitment to the organization. Journal of Occupational Psychology, 63(1), 1–18. https://doi.org/10.1111/j.2044-8325.1990.tb00506.x

Allen, N.J., & Meyer, J.P. (1991). A three-component conceptualization of organizational commitment. Human Resource Management Review, 1, 61-89. http://dx.doi.org/10.1016/1053-4822(91)90011-Z

Ardiansyah., Isnurhadi, H., & Widiyanti, H.M. (2019). The effect of budget participation on budget performance with organizational commitment as a moderating variable: Case study at the Public Service Agency (BLU) of Sriwijaya University. International Journal of Scientific Research and Engineering Development, 2(1), 256-269. http://www.ijsred.com/volume2/issue1/IJSRED-V2I1P30.pdf

Ax, C., Johansson, C., & Kullvén, H. (2002). Den nya Ekonomistyrningen (2. uppl.ed.). Malmö: Liber ekonomi.

Anthony, R.N. (1965). Planning and Control Systems: A Framework for Analysis. Boston: Division of Research, Graduate School of Business Administration, Harvard University.

Badu, I., Awaluddin, I., & Mas’ud, A. (2019). Pengaruh partisipasi penyusunan anggaran, Komitmen Organisasi, Profesionalisme, Gaya Kepemimpinan dan Struktur Organisasi Terhadap Kinerja Managerial. Jurnal Progres Ekonomi Pembangunan, 4(1), 99-113. http://dx.doi.org/10.33772/jpep.v4i1.6247

Banks, K. (2018). The importance of budgeting in business. Retrieved from https://wlf.com.au/importance-budgeting-business

Batilmurik, R. W., Noermijati., Acmad S.., & Fatur, R. (2019). Organizational commitment of police officers: A static study technique in Indonesian national police. Journal of Advanced Research in Dynamic and Control Systems, 11(02), 1876-1884. https://www.jardcs.org/abstract.php?id=1568

Bragg, S. (2018). Limitations of financial statements. Retrieved from https://www.accountingtools.com/articles/limitations-of-financial-statements.html.

Brinkmann, J., Grichnik, D., & Kapsa, D. (2010). Should entrepreneurs plan or just storm the castle? A meta-analysis on contextual factors impacting the business planning–performance relationship in small firms. Journal of Business Venturing, 25(1), 24–40. http://dx.doi.org/10.1016/j.jbusvent.2008.10.007

Burns, P., & Dewhurst, J. (1990). Small Business and Entrepreneurship. Basingstoke: Macmillan Education.

Cambalikova, A., & Misun, J. (2017). The importance of control in managerial work. In International Conference Socio-Economic Perspectives in The Age of XXI Century Globalization (pp. 218-229). Retrieved from https://mpra.ub.uni-muenchen.de/83776/

Chu, H. M. (2015). Factors affecting to budget process in small and medium-sized enterprises (SMEs) in Ho Chi Minh City-Vietnam [Master’s thesis, Ho Chi Minh City University of Technology].

Donna, O. K. (2018). Strategy implementation and organizational performance among institutions of higher learning in Kiambu County [Master’s thesis, Kenyatta University].

Dunk, A. S. (1993). The effects of job-related tension on managerial performance in participative budgetary settings. Accounting Organizations and Society, 18(7/8), 575-585. https://doi.org/10.1016/0361-3682(93)90043-6

Eke, G. O. (2018). Internal control and financial performance of hospitality organizations in Rivers State. European Journal of Accounting, Auditing and Finance Research, 6(3), 32-52.

Gomera, S., Chinyamurindi, W. T., & Mishi, S. (2018). Relationship between strategic planning and financial performance: The case of small, micro and medium-scale businesses in the Buffalo city metropolitan. South African Journal of Economic and Management Sciences, 21(1), 1-9. https://doi.org/10.4102/sajems.v21i1.1634.

Govindarajan, V. (1986). Impact of participation in the budgetary process on managerial attitudes and performance: Universalistic and contingency perspectives. Decisions Sciences, 17(4), 496- 516. https://doi.org/10.1111/j.1540-5915.1986.tb00240.x

Griffins, L. W. (2006). Strategic planning: Concept and cases. Strategic Management Journal, 16(2), 71-83.

Hair, J. F., Anderson R. E., Tatham R. L., & Black, W. C. (1992). Multivariate Data Analysis with Readings, (3rd edition). Macmillan, New York.

Hariyanto, E. (2018). Effect of participation budgeting on manager performance: Goal commitment and motivation as moderating variable. In Advances in Social Sciences, Education and Humanities Research. 5th International Conference on Community Development (AMCA 2018), Atlantis Press. https://doi.org/10.2991/amca-18.2018.91

Ibrahim, M., Sulaima, M., Kahtani, A. A., & Abu-Jarad, I. (2012). The relationship between strategy implementation and performance of manufacturing firms in Indonesia: The role of formality structure as a moderator. World Applied Sciences Journal, 20(7), 955-964. https://doi.org/10.5829/idosi.wasj.2012.20.07.2799.

Jones, G., George, J., & Hill, C. (1998), Contemporary Management. New York: McGraw-Hill.

Khan M.R., Ziauddin, Jam F.A., & Ramay M.I. (2010). The impact of organisational commitment on employee job performance. European Journal of Social Sciences. 15(3), 292-298.

Kihara, M. P. (2016). Influence of strategy implementation on the performance of manufacturing small and medium firms in Kenya [Doctoral dissertation, Jomo Kenyatta University of Agriculture and Technology].

Kimunguyi, S., Memba, F., & Njeru, A. (2015). Effect of budgetary process on financial performance of NGOs in heath sector in Kenya. International Journal of Business and Social Science, 6(12), 163-172.

Kochik, S. (2011). Budget participation in Malaysian Local Authorites. [Doctoral dissertation, Aston University].

Lakis, V., & Giriunas, L. (2012). The concept of internal control system: Theoretical aspect. Ekonomika, 91(2), 142-152. http://dx.doi.org/10.15388/Ekon.2012.0.890

Lam, M. T. (2017). Exploring the practice and application of strategic management in small and medium sized enterprises (SMEs) in Dong Thap province of Vietnam. International Journal of Scientific & Engineering Research, 8(10), 1067-1072.

Le, Q. H. (2016). Data Analysis in Business. Vietnam: Economics Publication of HCMC.

Li, W., Nan, X., & Mo, Z. (2010). Effects of budgetary goal characteristics on managerial attitudes and performance. In 2010 International Conference on Management and Service Science (pp. 1-5). https://doi.org/10.1109/ICMSS.2010.5578521.

Luu, T. T. (2010). Organizational culture, leadership and performance measurement integratedness. International Journal of Management and Enterprise Development, 9(3), 251-275. https://doi.org/10.1504/IJMED.2010.037066

Manafe, J. D., & Setyorini, T. (2019). The impact of organizational commitment as mediator and moderator relationship between budgeting participation on managerial performance: Evidence from Indonesia. The International Journal of Social Sciences World, 1(1), 1-10. https://doi.org/10.5281/zenodo.3522567.

Mashovic, A. (2018). Key financial and nonfinancial measures for performance evaluation of foreign subsidiaries. Journal of Contemporary Economic and Business Issues, 5(2), 63-74.

Mihaila, S., Ghedrovici O., & Badicu, G. (2015). The importance of budgeting for strategy implementation. European journal of Accounting, finance and Business, 3(2), 57-69.

Moshood, B., Sanjo, O. M., & Taofeek, A., & Eze, B. U. (2019). Employee commitment and firm performance: Evidence from a manufacturing firm in Nigeria. Hallmark University Journal of Management and Social Sciences, 1-3. Retrieved from https://www.hallmarkuniversity.edu.ng/portal/FileUploads/Hallmark%20Journal,%20HUJMSS%20Vol.%201,%20No.%203.pdf

Mowday, R. T., Steers, R. M., & Porter, L. W. (1979). The measurement of organizational commitment. Journal of Vocational Behavior, 14(2), 224-247. https://doi.org/10.1016/0001-8791(79)90072-1

Ngo, V. M., & Nguyen. H. H. (2016). The relationship between service quality, customer satisfaction and customer loyalty: An investigation in Vietnamese retail banking sector. Journal of Competitiveness, 8(2), 103 – 116. https://doi.org/10.7441/joc.2016.02.08

Ngugi, C. N., Kihara, P., & Munga, J. (2017). Relationship between strategy implementation and performance of insurance firms in Nairobi-Kenya. The Strategic Journal of Business & Change Management, 3(2), 15–31.

Nguyen, T. H., Khuu, T. Q., & Nguyen, N. D. L. (2018). Determinants of firm growth: Evidence from Vietnamese SMEs. Journal of Economics and Development, 20(3), 71-87. https://doi.org/ 10.33301/JED-P-2018-20-03-05

Nguyen, T. T. T. (2019). Analysis of the management process to enhance SMEs performance in Ho Chi Minh City. International Journal of New Technology and Research, 5(12), 09-15.

Nouri, H., & Parker, R. J. (1998). The relationship between budget participation and job performance: The role of budget adequacy and organizational commitment. Accounting Organizational and Society, 23(5/6), 467-483. https://doi.org/10.1016/S0361-3682(97)00036-6

Nzewi, H. N., & Ojiagu, N. C. (2015). Strategic planning and performance of commercial banks in Nigeria. International Journal of Scientific & Technology Research, 4(5), 238-246.

Obiero, J. O. & Genga, P. (2018). Strategy implementation and performance of Kenya Revenue Authority. International Academic Journal of Human Resource and Business Administration, 3(3),15-30.

Ogiedu, K. O. & Odia, J. (2013). Relationship between budget participation, budget procedural fairnes, organizational commitment and managerial performance. Review of Public Administration and Management, 2(3), 234-250. https://doi.org/10.4172/2315-7844.1000138

Okoye, E. I., Odum, A. N., & Odum, C. (2017). Effect of balanced scorecard on firm value: The case of quoted manufacturing companies in Nigeria. In The 2017 International Conference on African Entrepreneurship and Innovation for Sustainable Development (AEISD). Retrieved from https://ssrn.com/abstract=3038680.

Omosidi, A. S., Oguntunde, D. A., Oluwalola, F. K., & Ajao R. L. (2019). Budget implementation strategies and organisational effectiveness in colleges of education in Nigeria. Makerere Journal of Higher Education, 10(2), 119-131. http://dx.doi.org/10.4314/majohe.v10i2.9

Omotayo, O. O., Michael, O. O., & Andre, A. A. (2018). Strategic planning and corporate performance in the Nigerian banking industry. Asian Journal of Economics, Business and Accounting, 7(2), 1-12. http://dx.doi.org/10.9734/AJEBA/2018/36118

Peronja, I. (2015). Performance effects of the business process change in large enterprises: The case of Croatia. Management, 20(1), 1-22.

Phan, U. H. P., Nguyen, P. V., Mai. K. T., & Le. T. P. (2015). Key determinants of SMEs in Vietnam. Combining quantitative and qualitative studies. Review of European Studies, 7(11), 359-375. http://dx.doi.org/10.5539/res.v7n11p359

Pimpong, S., & Laryea, H. (2016). Budgeting and its impact on financial performance: The case of non-bank financial institutions in Ghana. International Journal of Academic Research and Reflection, 4(5), 12-22.

Porter, L. W., Steers, R. M., Mowday, R. T., & Boulian, P. V. (1974). Organizational commitment, job satisfaction, and turnover among psychiatric technicians. Journal of Applied Psychology, 59(5), 603–609. https://doi.org/10.1037/h0037335

Princy, K., & Rebeka, E. (2019). Employee commitment on organizational performance. International Journal of Recent Technology and Engineering, 8(3), 891-895. https://doi.org/10.35940/ijrte.C4078.098319.

Putri, Y., & Solikhah, B. (2018). Organizational commitment, information asymmetry, and the nature of conscientiousness as moderating the relationship of budget participation to budgetary slack. Accounting Analysis Journal, 7(3), 176-182. https://doi.org/10.15294/aaj.v7i3.22278

Qi, Y. (2010). The impact of the budgeting process on performance in small and medium-sized firms in China [Doctoral dissertation, Enschede: University of Twente]. https://doi: 10.3990/1.9789036529839.

Rachman, A. A. (2014). The effect of organization commitment and procedural fairness on participative budgeting and its implication to performance moderating by management accounting information (A survey on province Local Government Unit Agencies of West Java). Review of Integrative Business And Economics, 3(1), 201-218.

Recep, B., Mahmut, D., & Murat, D. (2010). Organizational commitment and case study on the union of municipalities of Marmara. Regional and Sectoral Economic Studies, 10(2), 29-52.

Santos, J. B & Brito. L. A. L. (2012). Toward a subjective measurement model for firm performance. Brazilian Administration Review, 9(6), 95-117. https://doi.org/10.1590/S1807-76922012000500007

Steers, R. M. (1977). Antecedents and outcomes of organizational commitment. Administrative Science Quarterly, 22(1), 46–56. https://doi.org/10.2307/2391745

Suárez, C. A. (2017). Internal control systems leading to family business performance in Mexico: A framework analysis. Journal of International Business Research, 16(1).

Susanti, N., Eprillison, V., & Jolianis, J. (2018). Budgeting participation and managerial performance of government apparatus. Advances in Economics, Business and Management Research, 64, 73-79. https://doi.org/10.2991/piceeba2-18.2019.10

Shamsudeen, K., Keat, O. Y., & Hassan, H. (2016). Assessing the impact of viable business plan on the performance of Nigerian SMEs: A Study among Some Selected SMEs Operators in North-Western Nigeria. MAYFEB. Journal of Business and Management, 1, 18-25.

Tran, N. T. (2019). Improvement of Vietnamese small and medium enterprises competitiveness in international integration. Political Theory Journal. Retrieved from http://lyluanchinhtri.vn/home/en/index.php/practice/item/642-improvement-of-vietnamese-small-and-medium-enterprises-competitiveness-in-international-integration.html.

Van, T. T. T. (2015), Budgeting practices in Vietnam: A survey in Da Nang city [Master’s thesis, Oulu Business School].

Ward, S. (2019). SME definitions vary from country to country. Retrieved from https://www.thebalancesmb.com/sme-small-to-medium-enterprise-definition 2947962.

Weissenberger-Eibl, M. A., Almeida, A., & Seus, F., (2019). A systems thinking approach to corporate strategy development. Systems, 7(16), 1-10. https://doi.org/10.3390/systems7010016

Wong-On-Wing, B., Guo, L., & Lui, G. (2010). Intrinsic and extrinsic motivation and participation in budgeting: Antecedents and consequences. Behavioral Research in Accounting 22(2), 133-153. https://doi.org/10.2308/bria.2010.22.2.133

Yuen, D. C. Y., & Cheung, D. C. Y. (2003). Impact of participation in budgeting and information asymmetry on managerial performance in the Macau service sector. Journal of Applied Management Accounting Research, 1(2), 65-78.

Yulia, Y. (2017). Effective business planning case study: Company x [Bachelor’s thesis, Lahti University of Applied Sciences].

Zainuddin, Y., Yahya, S., Kader Ali, N.N., & Abuenniran, A. S. (2008). The consequences of information asymmetry, task and environmental uncertainty on budget participation: Evidence from Malaysian managers. International Journal of Managerial and Financial Accounting, 1(1), 97–114. http://dx.doi.org/10.1504/IJMFA.2008.020464

Zefeiti, S. M. B., & Mohamad, N. A. (2017). The influence of organizational commitment on Omani public employees’ work performance. International Review of Management and Marketing, 7(2), 151-160.

Abstrakt

CEL: Celem tego badania jest wsparcie sektora małych i średnich przedsiębiorstw (MŚP) w Ho Chi Minh City (HCMC), co skutkuje ulepszeniem, lepszą wydajnością zarządzania i zrównoważonym przyjęciem korzystnych praktyk konkurencyjnych dostosowanych do współczesności. Badanie przeprowadzono w celu określenia kluczowych czynników zarządczych, które wpływają na wyniki wietnamskich MŚP. Przeanalizowaliśmy takie czynniki, jak planowanie biznesowe, zaangażowanie organizacyjne, wdrażanie strategii i kontrola zarządcza, przyjmując jako czynnik pośredniczący proces budżetowy, który pozytywnie wpływa na wyniki MŚP. METODYKA: W badaniu pilotażowym zebraliśmy 105 próbek i przeanalizowaliśmy wyniki w celu zbadania i potwierdzenia wiarygodności instrumentu badawczego. W badaniu pilotażowym zastosowano podejście ilościowe, w którym testowano wiarygodność za pomocą analizy alfa Chronbacha i eksploracyjnej (EFA) z oprogramowaniem IBM SPSS 20.0. Rzeczywiste badanie przeprowadzono z wykorzystaniem analizy ilościowej, w której technikę randomizacji zastosowano na 403 próbie. Pełna ilość danych została przetestowana za pomocą alfa Cronbacha, konfirmacyjnej analizy czynnikowej (CFA) i EFA. Modelowanie równań strukturalnych (SEM) zostało wykorzystane do przetestowania zarówno ram koncepcyjnych, jak i hipotez rzeczywistego badania. Badanie przeprowadzono w okresie od października 2016 do czerwca 2020. WYNIKI: Analiza MŚP zidentyfikowała czynnik pośredniczący, proces budżetowy, jako mający istotny wpływ na czynnik zależny, czyli wyniki MŚP. Jeśli chodzi o łączny wpływ na wyniki MSP, spośród czterech czynników zarządzania, czynnikiem o największym pozytywnym łącznym wpływie na wyniki MSP było wdrożenie strategii. Drugim największym pozytywnym łącznym wpływem na wyniki MŚP było zaangażowanie organizacyjne; trzecim co do wielkości pozytywnym efektem łącznym było planowanie biznesowe; a czwartym była kontrola zarządcza. Można zatem stwierdzić, że gdy menedżerowie MŚP zmienią te kluczowe czynniki, zmienią one poziom wydajności swoich przedsiębiorstw. IMPLIKACJE: Badanie to dostarcza wglądu w zarządzanie wydajnością MŚP oraz w jaki sposób czynniki zarządcze wpływają na poziom tego zarządzania wydajnością. W wyniku badania zidentyfikowano następujące kluczowe czynniki: realizacja strategii, zaangażowanie organizacji, planowanie biznesowe, kontrola zarządcza oraz pośrednicząca rola procesu budżetowego. Te czynniki związane z zarządzaniem mają znaczący wpływ na wyniki MŚP, a implikacja teorii opiera się na zarządzaniu wynikami, aby przyczynić się do rozwoju dziedziny zarządzania. Ten model badawczy można zastosować do praktyk zarządzania w celu restrukturyzacji, innowacji i poprawy ogólnych wyników MŚP. Ponadto badanie to zapewnia MŚP procedury zarządzania, które umożliwią im konkurowanie, adaptację i poprawę zrównoważenia na rynku globalnym. ORYGINALNOŚĆ/WARTOŚĆ: Model ten zapewnia naukowcom i praktykom bezcenną wiedzę niezbędną do zarządzania wydajnością przedsiębiorstwa, która pomoże MŚP w rozwoju jako zrównoważonych i konkurencyjnych graczy na rynku.

Słowa kluczowe: MŚP, zarządzanie wynikami, wdrażanie strategii, zaangażowanie organizacji, planowanie biznesowe, kontrola zarządcza, proces budżetowy, Wietnam

Biographical notes

Premkumar Rajagopal [BBA (RMIT, Melbourne), MBA (UUM, Malaysia), PhD (USM, Malaysia) and Master Class BSC, Harvard]. Prof. Dr. Premkumar Rajagopal is a specialist in Supply Chain Management (SCM) and is currently President of Malaysia University of Science and Technology. He started his career as Manufacturing System Analyst at Seagate Technology (1994-1997), later joining Intel Technology as Logistics Manager and later as Supply Chain Planning Manager. A highly sought-after speaker in the field of Industry 4.0 and SCM, he is frequently invited to speak on Industry 4.0 trends and SCM issues at international conferences in France, China, Indonesia, Philippines, Japan, Sudan, Riyadh, Thailand, India, Colombo, and Myanmar.

Vuong Khanh Tuan, MBA (OUM, Malaysia), PhD in Management, Malaysia University of Science and Technology (The Malaysia University of Science and Technology was established with the assistance of the Massachusetts Institute of Technology (MIT) under the auspices of a collaborative agreement between MUST-Ehsan Foundation of Malaysia and MIT).

Conflicts of interest

The authors declare no conflict of interest.

Citation (APA Style)

Tuan, V.K., & Rajagopal, P. (2022). The mediating effect of the budget process on the performance of small- and medium-sized enterprises in Ho Chi Minh City, Vietnam. Journal of Entrepreneurship, Management, and Innovation, 18(1), 65-92. https://doi.org/10.7341/20221813