Patrícia Becsky-Nagy, Ph.D., Assistant Professor, University of Debrecen Faculty of Economics Institute of Accounting and Finance Department of Finance, 4002 Debrecen, Pf. 400., Hungary, e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

Abstract

The current article focuses on the special aspects of venture capital’s value creation methods, summarizing the author’s researches in this field. This article puts special emphasis on the scrutiny of the Hungarian market as the value creation practices on the domestic market have not been revealed thoroughly in the literature yet. The article attempts to examine the performance of venture capital, especially the JEREMIE funds, according to the limited available secondary data of the companies involved, which helps to assess the role of the government in bridging the financial gap and solving the problems in the venture capital market in Hungary. In this field reliable statistical data is not available, but there is an ongoing primer research led by the author, producing new information soon. The article presents the special investment and value creating methods of venture capitalists. In the first part of the article the theoretical background is presented, and in the second part of the article the author’s research results are demonstrated following the same order.

Keywords: venture capital, value creation, governmental role.

Introduction

The main question of the article is how venture capitalists create value, what the special aspects of their value creating mechanism are, and how it works in Hungary. The relevance of the topic is, that the JEREMIE program launched by the European Union spurred the venture capital market of the Central and Eastern European region that made research in the field topical as previously unprecedented number of investments were made in the region. The great majority of the investments made by JEREMIE funds are currently active therefore bringing a verdict about the performance of the program would be premature therefore making certain conclusions about the program are limited. The exit performance and the return on investment can only be evaluated after the closure of the funds, but as the information about exits is usually confidential the evaluation in this field of venture capital funding is limited. Nonetheless the program is in the early stages and only at the end of its investment period can the scope of the portfolio companies be outlined and some conclusions reached about the state of the demand and supply side of the market.

The contribution of the article to the topic is that it puts special emphasis on the scrutiny of the Hungarian market, as the value creation practices on the domestic market have not been thoroughly revealed in the literature yet. The article attempts to examine the performance of venture capital, especially the JEREMIE funds, based on the limited available data of the companies involved, which helps to assess the role of the government in bridging the financial gap and solving the problems in the venture capital market in Hungary.

In the literature review the article introduces the theoretical framework of the analysis and the most important economic theories that are connected to venture capital funding. The literature review discusses the effects of imperfections in the venture capital market, the two-level principal-agent relationship that evolves in venture capital financing, the problem of funding gaps, the specialties of young and innovative companies’ capital structure, and the relevance and methods of active and passive roles of state.

Literature review

The following section will describe the theoretical background of the special aspects of venture capital’s value creating mechanisms based on the literature. There is an enhanced information asymmetry in the venture capital market that results in an increased uncertainty in the industry but, on the other hand, by selecting companies with huge growth potential and providing them value added services, the investors can benefit from the increasing value of these companies. Hence, there is the possibility of realizing extremely high returns on their investments. The inefficiencies of the venture capital market can be alleviated by informal venture capital investors and by the public sector’s direct and indirect involvement.

Imperfections in the venture capital market

Venture capitalists are financial intermediaries who collect capital from individuals and institutional investors then manage and invest the accumulated capital. They make their investments into private companies, not listed on the stock exchange, for equity in the company and/or optional rights for gaining further ownership. Venture capital investments are long term cooperation between investors and entrepreneurs in order to alleviate the increase of the firm’s value and benefit from this growth by selling their shares for a high profit. Venture capitalists take part in the control of the invested companies and usually they not receive dividends but reinvest the profits into the companies in order to enhance further growth. Traditional venture capital investors mainly focus on the early stages of the companies while buyout funds are for larger scale investments where the focus is more on the matured stages of the companies (Prowse, 1998, p. 22; Karsai, 1997, p. 168; Becskyné Nagy, 2008).

There is an increased information asymmetry in the venture capital market and the problem of adverse selection arises with a higher chance in the case of companies that are the focus of these investments (Hall, 2002; Becsky-Nagy & Fazekas, 2015a). The economic models that are based on the concept of information asymmetry provide a theoretical framework for understanding the inefficiencies that evolve in the market of the young and innovative enterprises and for exploring the methods that could alleviate the funding and knowledge gaps. In an imperfect informational environment the market cannot reach its optimal efficiency. Leland and Pyle (1977) describes the ‘missing market’ problem which says, that in markets where enhanced information asymmetry occurs the supply of capital will disappear if on the demand side the number of those companies that are not suitable for obtaining capital is too high. In order to bring suitable investment opportunities to the surface the bridging of the information gap via the transfer of relevant information is necessary. According to Hall (2002) venture capitalists are able to bridge this information gap, but in case of the Hungarian market the investors could not fulfill this role. Furthermore, government involvement was necessary in order to provide information for the venture capitalists.

In connection with the concept of information asymmetry, the pecking order theory is also a relevant economic theory that describes the hierarchy of the different capital sources (Myers, 1984, 2001; Myers & Majluf, 1984). Based on this theory, entrepreneurs have an information advantage about their companies and their goal is not in finding the optimal proportion of the different funding sources, but instead entrepreneurs have preferences towards the funding sources and they try to obtain the most preferred funding sources if they are available. In venture capital funding the general partners become owners of the companies with voting rights and they have insight into the operation of the companies that decreases the informational advantage of the entrepreneurs. In addition to this, as a result of its high profit expectations, venture capital can be the most expensive form of funding. Based on the findings of Zoppa and McMahon (2002) small and medium-sized enterprises are less willing to dilute the ownership structure, hence they prefer internal financing like retained earnings, depreciation and amortization and also debt financing, rather than external equity financing. However, the innovative companies are unable to obtain debt financing as they are about to enter new markets, their products are usually in the development stage and they do not have collateral (Philott, 1994; Gompers, 1995; Hall, 2002). In addition to this, the information gap that occurs in the case of these companies imposes further limits on the available funding forms (Mason & Harrison, 1998).

The principal-agent theory is in close connection with capital structure theories that are focusing on the wealth maximization of the owners. Sahlman (1990) was the first who presented the two-level principal-agent relationship that evolves in venture capital financing, where the venture capitalists are the principals in terms of their relationship with the portfolio companies. But on the other hand, in managing the funds they also act as agents for those investors who provide the capital to the venture capital funds in order to gain profit via the successful investment activity of the venture capitalists. Therefore, in managing the problems that derive from information asymmetry and the principal-agent relationship, such as adverse selection and moral hazard issues, the venture capitalists play a crucial role in the success of these investments, so venture capital contracts include various clauses in order to solve these problems. However, as a result of the ‘noise’ in the information the uncertainties deriving from the informational problems cannot be eliminated (Reid, 1999; Becsky-Nagy & Fazekas, 2015a).

The special expertise and business experience of venture capitalists enables them to get the companies through the early stages of their life when the uncertainty is very high hence they are able to exploit the growth potential of these companies. The competence of venture capitalists can be harnessed via the cooperation of the entrepreneurs and investors so the personnel contribution of venture capitalists is indispensable for enhancing the growth of these companies (Becskyné-Nagy, 2008).

The real options approach of venture capital shows how venture capital is able and willing to manage efficiently the high uncertainty of these companies that derives from the business risks, information asymmetries and moral hazard issues. Based on the real options approach of venture capital these investments are projects with high flexibility and managers can create options and gain profit by benefiting from the positive outcomes and mitigating the downside risks (Kogut & Kulatilaka, 2001; Kaplan, Sensoy & Strömberg, 2009; Copeland & Keenan, 1998). In this sense venture capital funds are portfolios created from real options and the managers of the funds can influence the value of these options. From an option valuation perspective, the increased uncertainty increases the value of these investments as a result of the inherent options, contrary to the traditional valuation approaches where risks decrease the utility of investors. Real options’ reasoning relies on the special expertise of venture capital investors and describes, from a valuation point of view, why venture capitalists are willing to fund these enterprises. In this sense the valuation itself is a special area of venture capital where value creation appears.

Venture capitalists use various tools and methods in order to manage the high risks of their investments, like; high profit expectations, screening, the use of special contract stipulations and syndicate agreements, the use of convertibles and preference shares, the monitoring of investments, multi-staged financing of companies, diversification and the integration of portfolio-companies into networks. The role of high profit expectations is to compensate the investors for the risks of the investments. Screening and due diligence can ensure the quality of the investments and via these activities venture capitalists can select companies for their portfolios that could be viable on the market and have the greatest growth potential. After the process of selection an investment contract is drawn up with various clauses built into it in order to eliminate special risks. The use of different financial instruments, like preference shares and convertible securities are also very widespread in these contracts that could protect the investors from downside risks while maintaining the chance of achieving high returns. The opportunity to revise the investments at certain stages is provided by the multi-staged funding, where additional investments are often bound to the condition of reaching given milestones. This method enables the investors to create options in the investments that could mitigate the downside risks hence the risk-return characteristics are favorable compared to straightforward funding. The investment decision is followed by the monitoring of the invested companies as a part of the cooperation of venture capitalists and entrepreneurs. One purpose of the monitoring is to reduce the information asymmetry, hence the possible negative effects that could arise from the principal-agent relationship while, on the other hand, through their special expertise they can improve the performance and increase the value of the companies. Especially in larger portfolios the effect of diversification leads to more favorable risk-return characteristics (Becsky-Nagy & Fazekas, 2015a).

The selection criteria of venture capital

As selection is the first and crucial step in the process of the value creation in venture capital funding prior to the investment decision itself, it is very important to collect the most important selection criteria of venture capitalists from the literature. Only a few enterprises are able to meet the standards and criteria imposed by the venture capitalists. Only companies with high profit expectations and great growth potential are able to obtain venture capital, around 90% of the companies that seek venture capital funding are rejected by the investors (Petty & Gruber, 2011). As selection is an essential momentum in the value creation there is an extensive literature that discusses the topic.

The first step of the selection process is the screening. According to the early study of Tyebjee and Bruno (1984) the companies are evaluated at the beginning of the screening based on the size of the investment, the industry and the applied technology, geographical location and the lifecycle stage of the companies. The business plans usually cover the mentioned criteria therefore the submission of the business plan is usually the first milestone in the selection process (Hudson & Evans, 2005). Companies in a very early stage of their life with lower capital needs are usually out of the target of venture capital. As a result of the costs of the investment process, especially the cost of due diligence, for institutional venture capitalists, investing under a certain amount of capital is not economical (Osman, 2008). For companies with lower capital needs, government funds, R&D tenders or angel investors can provide funding. The importance of geographical location is in connection with the personnel involvement of the venture capitalists (Tyebjee & Bruno, 1984). In the seed, early and early expansion stages the companies are in an imperfect information environment, with regards to the market and technology that decreases their chance of obtaining venture capital (Norton & Tannenbaum, 1993).

The first stage of the screening is followed by the scrutiny of the entrepreneur and the management, the product, the market characteristics and the financial aspects. The entrepreneur’s expertise, managerial and professional competences, personality and commitment all play a crucial role in the investment decision, as the cooperation of the entrepreneurs and venture capitalists is a key factor in the fate of the investments and a detailed analysis of the management can reduce the risks of principal-agent relationship (Becskyné Nagy, 2008; Becsky-Nagy, 2016; Dubini, 1989; Franke, Gruber, Harhoff & Henkel, 2008; Hall & Hofer, 1993). The technical uncertainty that arise in connection with new products and services is another important factor in the selection of companies as technically feasible products and services that are often protected by patent can lead to a rapid growth in sales. The level of competition in the market and the threat of new entrants are also an important factor as in saturated markets the growth’s opportunities are usually lower. The high initial costs of creating the prototype and also the cost of applied technology can only be compensated by high selling prices (Silva, 2004; Halaska, 2012; Petty & Gruber, 2011). Concerning market conditions, the industry, the potential size of the market, the probability of entering international markets, the chance of gaining permanent competitive advantage, the threat of substitute products and the volatility of the market are the most important factors that affect the growth potential of the invested companies. The exit opportunities, the time and possible method of the exit and the expected return are also taken into consideration in the investment decision (Becskyné & Biczók, 2006). Not just the individual characteristics of the companies have a role in the selection but also their contribution to the overall risk of the venture capitalists portfolio is important.

According to Shepard, Zacharakis and Baron (2003) the experience of the venture capitalists is in correlation with the success of their decisions. The more experienced venture capitalists are more successful in their investments as well, but on the other hand an overly long investment record leads to automatic decisions and by neglecting the unique aspects of each investment the chances of success may decrease.

Venture capital in the capital structure of companies

After the selection, according to the investment process, the venture capital’s position in the capital structure is crucial, as voting rights, control over the portfolio company and also the level of risk taking depends on the given financial instrument conditions. Based on many studies the convertible preference share is the optimal financial instrument for providing capital in venture capital funding (Berglöf, 1994; Casamatta, 2003; Cestone, 2000; Cornelli & Yosha, 2003; Marx, 1998; Schmidt, 2003; Trester, 1998) and this theory was confirmed by empirical studies as well (Kaplan & Strömberg, 2003; Bergemann & Hege, 1998). The special rights incorporated into preference shares can entitle venture capitalists to take control of the firm if the manager’s performance hinders the success off the investment. In extreme cases of the principal-agent problem, these instruments provide an opportunity for venture capitalists to solve the conflict of investors and managers (BecskyNagy & Fazekas, 2015a). This instrument also has a favorable effect on the position of investors in case of liquidation. According to Cumming (2005), in the case of the US, the tax benefits of convertible preference shares are an additional advantage of this financial instrument, but based on his research focusing on the Canadian market, he stated after analyzing 3000 companies, that there is not a prevailing method that could describe in a general way the funding practice of venture capitalists. Based on his research the form of common equity was the most widespread followed by debt financing and convertible bonds and convertible preference share was the fourth in this rank, but also a combination of the previous methods was observed. Furthermore he found a connection between the form of funding and the type of firm and, based on his results in the case of younger enterprises, the use of convertible preference shares is more frequent because in these companies the principal-agent problem evolves with higher probability. In early stage investments, venture capitalists do not favor debt, convertible bonds or the combination of equity and debt as a funding form, because these methods cannot provide the required control rights (Becsky-Nagy & Karászi, 2015).

The personnel contribution of venture capitalists

After the investment decision and contracts, the next step in the venture capitalists value creating process is the managerial support of the company. In their early stages the invested companies usually do not possess the decisive information and knowledge to formulate a strategy for their company and to manage it successfully (Rasila, Seppa & Hannula, 2002). The founders of young, innovative companies are usually experts with high qualifications but they do not have the necessary managerial and business experience (Vohor, Wright & Lockett, 2004). A special segment of the potential investments is the group of spin-off companies that commercialize technology and research with university origin, where the lack of managerial expertise is especially prevalent (Becsky-Nagy, 2013; Becsky-Nagy, Papp & Tóth, 2014).

One unique feature of venture capitalists is that, in addition to the capital, they also offer managerial assistance and can provide the necessary knowledge to run the company (Wright, Lockett, Clarysse & Binks, 2006). Through their personal contribution and knowledge transfer, venture capitalists are able to bridge not only the funding gaps that occur in case of young and innovative companies, but they also play an important role in the alleviation of the information and knowledge gap. The sources of the missing information and knowledge are a lack of managerial skills, market experience, engineering and professional skills. The other reason for the information gap is the uncertainty that derives from new technologies and new products that are introduced on previously non-existing markets with uncharted customer needs. The product itself often exists only as an idea and the companies shall deliver these plans to the market with the purpose of achieving a permanent competitive market advantage. Via the cooperation of investors and entrepreneurs, the venture capitalists are able to provide the necessary knowledge and information and also access to their extensive business networks. In order to reduce the risks of principal-agent relationship and to provide the non-financial value added services, the personnel contribution of the investors is necessary, therefore venture capitalists usually delegate members onto the supervisory board and appoint the chief executive of the firm. The presence of venture capitalists in the management team gives an insight into the operation of the invested companies and strengthens the functions of monitoring, control and governance, thereby reducing the risks of the investors (Wright, Hoskisson, Busenitz & Dial, 2001; Becsky-Nagy, 2016). However, the founders of small companies are not willing to share their innovative idea with the investors prior to investment because they fear that if the investment negotiations fail than the investors will implement and gain profit from their ideas. Another problem is that the founders are often biased towards their own ideas and they are not willing to take the advice and guidance of investors that may lead to compromises and the restricted freedom of their decisions.

The dynamic three-factor model (3C model) of value creation demonstrates the main sources of venture capital’s value creation that are capital, competence and cooperation (Becskyné- Nagy, 2008). The structural factors of venture capital are the size of the funds, the size of the deals, and the industrial and geographical extension. The model says that the value creation mechanism of venture capital is a self-feeding process where the sources and the structural factors become more and more extensive in time.

Alongside the provided knowledge and capital, there is also a great emphasis placed on cooperation, as a deteriorating relationship between investors and entrepreneurs, a conflict of interests or excessive control over the entrepreneurs, could lead to the failure of the investment. Cooperation, fair compromises and mutual trust is vital in order to create a well-functioning company.

The role of state in the venture capital market

Despite the fact that venture capitalists can create value in an investment process, there are insufficient market situations, when as a result of the information gap or the funding gap the supply side and the demand side of the venture capital market are not in the equilibrium. In these situations the state can help to shift the supply or the demand of venture capital.

Venture capital is a funding method that is able to alleviate the early stage funding problems of innovative firms with huge growth potential, but at the same time, because of the market inefficiencies that lead to funding gaps in the market of these companies, the question arises whether the active or passive role of the public sector is necessary to solve the funding problems of these enterprises. Table 1 contains the types of passive and active government participation in the venture capital industry. The active role of government on the venture capital market means that the state increases the supply of capital by providing funds in order to bridge the information gap or because of the absence of institutional investors’ interest. The primary goal of an active state role is to provide funding for those early stage companies that have huge growth potential, but for market investors, making investments in these companies is not economical because of the high transaction costs of selection and due diligence. Based on Hungarian and international evidence, direct state involvement does not lead to general success in the venture capital market. Government interventions have had a distorting effect on the market. One of the most important value creating factors of venture capital is the competence and managerial assistance of investors but in the absence of market investors this value enhancing effect cannot prevail. The public sector investors’ contribution to the development of companies is mainly confined to the capital provided but the other resources of venture capital, like competence and business networks do not occur in the case of public investments. Therefore, the public venture capital backed companies could not achieve such growth as the private venture capital backed companies do (Bottazzi & Darin, 2002; Schilder, 2006f; Luukkonen, Deschryvere & Bertoni, 2013; Grilli & Murtinu, 2014; Becsky-Nagy & Fazekas, 2015b; Fazekas, 2014).

| Passive government participation in the venture capital industry | Active government participation in the venture capital industry | |

|---|---|---|

| Passive government participation in the funding of technology-driven small enterprises | Active government participation in the funding of technologydriven small enterprises | |

| Stable economic environment Stable political environment Mitigation of country risks High GDP High public R&D expenditure Environment favourable for innovation Environment incentivising entrepreneurial activities Institutional and statutory conditions Support by business angels Support by incubators Facilitating the development of the capital market Tax allowance for investors Government loan and capital guarantees Training, education Improvement of entrepreneurial culture Promotion of information flow |

Non-reimbursable government grants for innovation and research and development Tax allowances for innovation and research and development activities Subsidised loans for the implementation of innovative research and development activities | Investment of budget resources in venture capital funds Management of venture capital funds created from budget resources |

| Source: Becsky-Nagy & Fazekas (2015b) | ||

The primary goal of a passive state role is to promote a stable economic and political environment that is able to create and sustain an efficient venture capital market. Incentivizing the market to evolve an innovative entrepreneurial environment contributes to the development of the demand side of the market that leads to an increasing number of technology-oriented, innovative enterprises via improving the entrepreneurial spirit. By ensuring a stable economic, political and legal environment and mitigating the regional and national risk, investment activity can be spurred into action that leads to the expansion of the capital’s supply. The role of the state is also pivotal in spurring the development and efficiency of the primary and secondary capital markets (Ludányi, 2002; Lerner, 1996). Table 1 contains the possible methods of active and passive state roles.

Research methods

As venture capitalists confidentially handle the information about their investments we do not have perfect information with regards to this funding form, especially about its return characteristics. The organizations that collect data about the returns on venture capital have to face various problems. The data is provided on a voluntary basis by the funds and, furthermore, the different databases use different methodologies. Although the latter research and databases provide more reliable results, we have to be aware of the fact that, in the interpretation of the results, there might be biases. In addition to the lack of data the analysis of return characteristics has methodological problems as well. The article attempts to collect the results of the Hungarian research based on the relevant secondary and primary sources.

The most commonly used secondary source of the return measure is IRR (Internal Rate of Return) that measures all returns based on the period’s cash flows, so as to make the investments comparable with other venture capital investments, or other type of investments. Horizontal IRR takes the net asset value at the beginning of the period as a negative cash flow, and the cash inflows within the period and the net asset value at the end of the period are positive cash flows and then IRR is calculated based on these cash flows. Horizontal IRR is able to show the industry trends. Net asset value is the residual value of the venture capitalists investments at the end of the period, in other words it shows the value of the still active investments. Rolling IRR shows the change of horizontal IRR in every year retrospectively. Pooled IRR shows the aggregated industry returns on the basis of the cash flows within the period modified by the residual values of the investments at the end of the given period. One drawback of using this measure is that IRR assumes the reinvestment of cash flows, which is rarely possible in the case of venture capital funds. Therefore, IRR can overestimate the actual return on funds invested, as there is a negative correlation between the return and the length of the investment. In addition to this, venture capitalists are more willing to only provide information about their successful investments which leads to an upward bias in the results (Becsky-Nagy & Fazekas, 2014).

The primary sources of data collection in the case of Hungarian investments are the business journals, internet portals and data provided by the investors. After the investments are identified, the financial reports of the invested companies provide further information about the parameters of their investments including the size of investment, change in sales and income etc. The databases of the European Venture Capital Association and the Hungarian Venture Capital Association provide data about the accumulated capital, the committed capital and about exit events. The main method of the industry’s scrutiny is still in the form of a case study as a result of the scarce information that limits the possibility of drawing more general conclusions.

Questionnaires come up against difficulties as the parties to investments are not willing to answer special key questions because of the confidentiality clauses in investment contracts and they consider this information to be a business secret (Glavanits, 2015).

In my previous research, in order to investigate the unique aspects of Hungarian venture capital investments, I compiled several case studies. Although more general conclusions cannot be drawn from these case studies, they did highlight the special moving forces and key factors of the industry (Becskyné-Nagy, 2008).

In connection with the selection criteria of the venture capitalists, we created a questionnaire based on the findings of the international literature, and asked all the Hungarian venture capital fund manager firms about their opinion (Dávid & Becsky-Nagy, 2016).

In 2012, I took part in research that focused on spin-offs in the capital and rural towns of Hungary. Spin-offs are a special field of venture capital investments, where the value creating contribution of the venture capitalists is similar to the general venture capital investments. In this research, I investigated the financing prospects of these companies. We observed 80 spin-offs and 38 of these companies were included in the research. Although the funding problems of spin-offs do not entirely cover the problems of venture capital’s potential investment targets, and are just a segment of it, it is assumable that their problems are similar to those companies that do not stem from universities (Becsky-Nagy, 2013).

Analysis / Study

The following section describes the findings of research into the venture capital value creating process based on the literature review and on the empirical research made by the author herself or as a member of a research group. The deductions of the research are not mentioned here, as those are written down in the referred publications. In this part, I follow the structure of the theoretical background where the following propositions were described.

Selection criteria

As a first step of the value creating mechanism of the venture capitalists, we examined the selection criteria of the potential portfolio companies. Through the synthesis and comparative analysis of the literature review in the field of the selection process of venture capital, they show that the most important criteria for venture capitalists, in order, are:

- return on investment,

- managerial skills of the entrepreneurs,

- growth potential of the market,

- professional experience of the founder,

- exit prospects,

- track record of the CEO (Dávid & Becsky-Nagy, 2016).

This ranking reflects the priorities of Hungarian investors towards the factors that are mentioned in the literature. The most important difference between Hungarian and international investors is that, in the opinion of international investors managerial skills play the most important role, while in the ranking of Hungarian investors the possible return has first place. At the same time, it is a common characteristic that investors put much emphasis on the skills, competence and experience of the executives in their investment decisions.

Venture capital in the capital structure of companies

In the venture capital market of the Central and Eastern European region, around 50% of the accumulated capital was provided by government funds. In the background of this dominance is the JEREMIE Program, where the capital of the funds is provided by the public and the private sector together and managed by market backed investors. Within the framework of this program, investments have been made in Hungary since 2010.

After the appearance of JEREMIE funds in 2010 they have become dominant in the Hungarian market. In 25% of the companies that received funding via JEREMIE, the investors used some form of preference shares to provide capital, in order to ensure adequate control over their companies (Becsky-Nagy & Fazekas, 2015b). In the case of the other companies, the investors became majority shareholders hence the additional rights provided by preference shares were unnecessary. Syndicated investments, in which the risks are shared between the investors, could also be observed. In other cases the mixed use of debt and equity financing could be observed as well.

There is no optimal and generally accepted practice as to how the capital provided by the venture capitalists should appear in the capital structure of the invested companies. The nature of the company, the stage in their lifecycle and other unique features of the companies, influence the ideal financial instruments that facilitate the growth of these companies the most, and hence increase their chances of a funding contract. Preference shares, convertible preference shares, convertible bonds, common shares and the combination of equity and debt financing, are widespread in Hungary as well as in the more developed countries, but compared to the market in the US convertible preference shares are not the most dominant instruments in Hungary.

Returns of venture capital

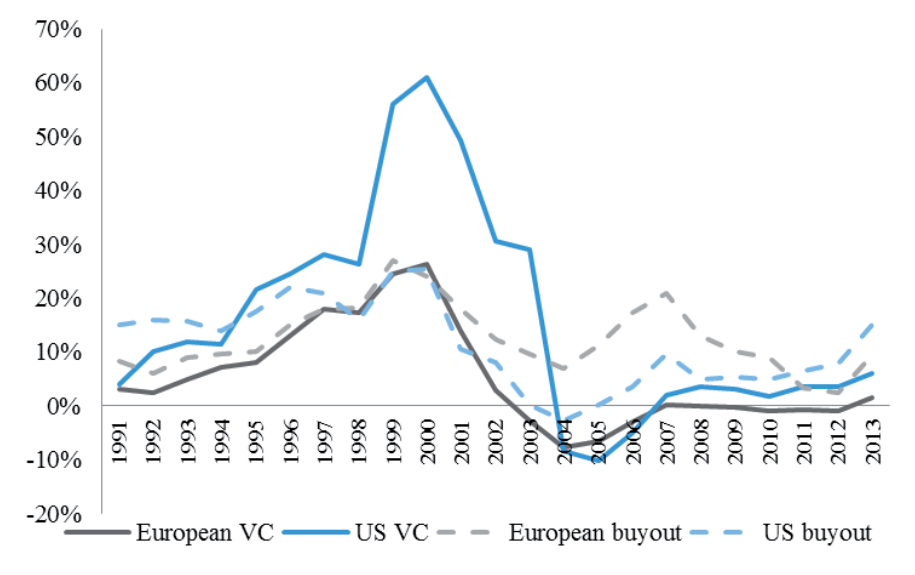

The returns on venture capital can be a measure of the venture capitalists’ value creation, though it is impossible to separate the venture capitalists contribution to the success, from the contribution of other parties. But the question was whether the venture capital backed companies can provide higher yields than others. In the case of venture capital investment returns, examined through IRR, this can be realized via exiting the invested companies, so the return characteristics of venture capital reflects how the value of the acquired shares increased within the investment period (Becsky-Nagy & Fazekas, 2014). By analyzing the returns in the markets of the US and Europe it is clear, that on average, the returns of the buyout funds that invest larger sums into more matured companies, were higher than the returns of the traditional venture capital investments. On the basis of risk-return tradeoff, buyout funds outperformed venture capital funds as well. In terms of geographical differences, the returns of the US venture capital market were higher than the returns of the European funds, which can be explained by the more developed stage of the US market. Figure 1 also shows that the return on venture capital investments were very sensitive to business cycles and current changes in returns show that the market is in recovery after the economic recession of 2008.

Source: EVCA (2014)

Within the private equity industry, the focus has shift ed away from its traditi onal functi on of funding young and innovati ve companies that have smaller capital needs, towards the fi nancing of more matured companies with larger capital needs. One reason of this change is the high cost of screening and due diligence of the deals that are proporti onately more favorable in case of buyouts, but by analyzing the return characteristi cs of the investments it is also clear, that buyout funds outperform the venture capital funds based on the average risk-return trade-off as well.

The yearly returns of the Hungarian market are infl uenced and biased by a few larger scale exit events as a result of the low sized market. In the coming years the investments of the government backed venture capital funds will approach exit ti me, so a record number of exits are expected by the closure of JEREMIE funds. On the other hand, while analyzing the exit acti vity of these funds, we have to be aware of the fact that, alongside the successful and highly profi table investments, there will be an increasing number of poor quality investments and low returns, as a result of the distorti ng eff ect of the temporary oversupply of capital induced by the government’s involvement.

The role of the state in the venture capital market

In an insuffi cient market the state can help in fi nding the new equilibrium point. Prior to the economic recession in 2008, the venture capital market in the Central and Eastern European showed signs of prosperity but its development still lags behind the developed Anglo-Saxon countries’ markets. This realization led to a more intensive active and passive role of the state and, therefore, the traditional venture capital markets shifted towards the government backed investments (Karsai, 2014; Karsai, 2015).

In the venture capital market of the Central and Eastern European region around 50% of the accumulated capital was provided by government funds. In the background of this dominance is the JEREMIE Program where the capital for the funds is provided by the public and the private sector together and managed by market backed investors. Within the framework of this program investments have been made in Hungary since 2010. There are several incentives built into this program with the aim of attracting private investors. These include the partial taking over of losses and a profit ceiling on the public funds, which create favorable leverage and improve the riskreturn characteristics of the investments for private investors. But, on the other hand, these incentives may implicate a threat of excessive risk taking. The funds were committed to invest 80% of the capital and that may lead to adverse selection in terms of the invested companies. On the other hand the increased investment activity increases the available information concerning the potential investments and the mechanisms of venture capital funding and hence the JEREMIE funds play an important role in alleviating the information asymmetries between the actual and potential demand and supply of venture capital. In the framework of JEREMIE, 28 venture capital funds made around 310 investments, which prove that the great amount of available capital on the market helped those companies obtain capital that otherwise, in the absence of collateral, would not have been able to obtain outside funding. The invested companies were mainly technology and IToriented, but companies in the field of life sciences and biotechnology were also able to obtain capital. The majority of the investments is currently active and awaits an exit, therefore the success of the investments, and with it the overall performance of the program itself, cannot be judged yet. However, the increased number of investments has already contributed to industry level knowledge and hence to the development of the venture capital market (Becsky-Nagy & Fazekas, 2015b).

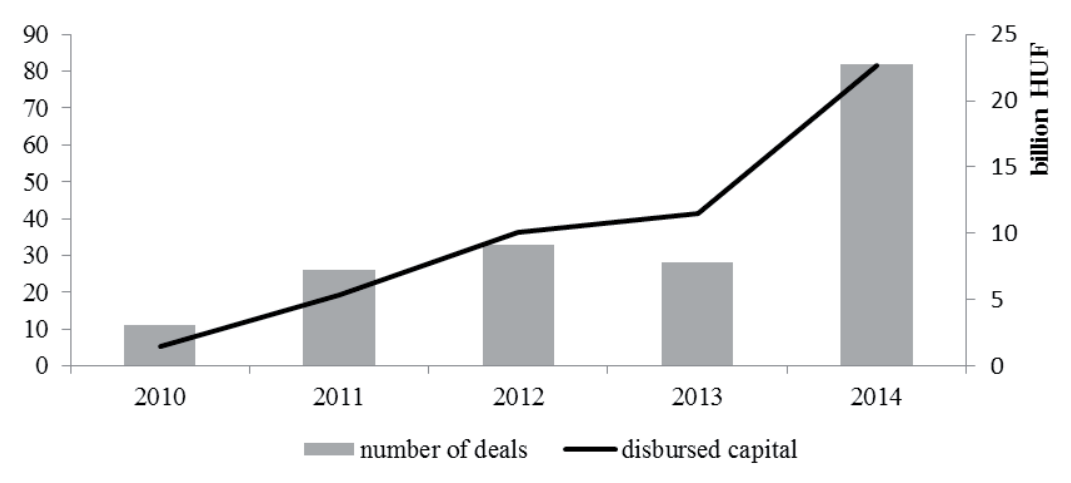

Figure 2 shows the actual capital disbursement of JEREMIE funds. JEREMIE funds were founded in four consecutive rounds but the progress of capital disbursement was low because of the complicated selection process. The slow progress of disbursement could be a sign of the low number of viable companies that are ready for investment as well. For the funds that were founded in the first round of the program, a wider range of investment opportunities had been available but because of the oversupply of capital and the high number of deals, in the later periods of the program less and less companies could be found that had the potenti al to meet the selecti on criteria of the venture capitalists. Because the diff erent rounds of the program were implemented within a short ti me period with overlap, the demand side of the market could not regenerate the companies that are able to obtain venture capital. But on the other hand the funds had been committ ed to invest 80% of the managed capital that might lead to lower quality investments which decreases the chance of successful and profi table exits on average.

* The disbursed amounts contain the growth in the subscribed capital and capital reserve of the portf olio companies as in the balance sheet. Consequently, the data disclosed for the disbursed amount may exceed the actual amount of the disbursement.

Source: Author’s own editi ng based on the data of the fi nancial statements of the portf olio companies

The venture capital’s contributi on to the spin-off companies, a special fi eld of venture capital value creati on

Based on 2012 research that was focusing on Hungarian university spin-off s, the most important barriers to insti tuti onal venture capital investments in Hungary are the following:

- venture capitalists are not conversant with the technology of the fi rm (4.0)

- venture capitalists are not willing to make smaller-scale investments (3.7)

- high return expectati ons of venture capitalists (3.6)

- the involvement of venture capitalists limits the authority of the chief executi ves in the operati on of the company (3.5)

- venture capital investors are averse to funding seed, early and early expansion stages (3.2)

- low quality of the business plan (2.9)

- lack of necessary business and managerial skills of the founders (2.8)

- inadequate support of venture capital by the economic policy (2.7)

- insufficient information about venture capitalists (2.6)

- unfavorable exit prospects (2.6) (Becsky-Nagy, 2013)

JEREMIE, launched by the European Union in 2005, started its investment activity in 2010 and was implemented as part of the EU cohesion policy with the objective of alleviating the regional, social and economic differences by enhancing the financing prospects of innovative SMEs through structural funds that provide financial engineering instruments. The result of the program is that a great amount of capital has flown into the Central and Eastern European region’s venture capital market that has mainly been invested into technology-oriented SMEs and this has improved the competitiveness of the companies and the region as well. The program was implemented with very similar conditions in the different countries of the region but their success can only be evaluated after the closure of the funds (Farkas, Gyallai & BecskyNagy, 2016).

The hybrid venture capital funds combine the methods of active and passive state involvement, as in this form, private investors with market experience manage mixed private and public capital, and the investment decisions are made by the private investors. The involvement of private investors strengthens the market perspective in the selection of possible investments, the “hands on” nature of the investments and the value added by the cooperation of investors and companies. The hybrid funds play a catalyst role in the development of the venture capital market. As a result of the increased investment activity, the private participants are able to gain experience and knowledge. At the same time, the venture capital awareness of the capital seeking firms’ increases as well, and this way hybrid funds enhance the actual development of the demand and supply of venture capital. On the other hand, the pressure of investing government funds raises the threat of adverse selection, as companies may receive funding that otherwise, under purely market conditions, they would not be able to meet the requirements of private investors. The soft requirements of hybrid funds distort the market and crowds out or bias the behavior of the few market participants that are willing to appear in the market. Such participants are mainly the angel investors.

In the long run, the withdrawal of the active role of the government’s funding and the increased role of passive participation in the market,

contributes the most to the efficiency of the venture capital market with the support of the start-up ecosystem. The passive role of the state is fundamental, not just temporarily as a catalyst in the venture capital market, but also in the long run in order to spur entrepreneurship via developing a stable economic, political, legal and capital market environment. The information asymmetries are prevailing especially in the case of rural regions and in order to support the innovative enterprises in these areas the mitigation of regional differences and the enhancement of regional environments is necessary.

Discussion

The article described the special aspects of venture capital’s value creation methods in the face of the unique characteristics of the Hungarian venture capital market compared to the developed countries’ market. The first part of the article gives the general theoretical background of the venture capital funding with special regard to the specific risks of these investments and the various risk management methods used by the investors. The next part discusses the active and passive state role and its necessity in the venture capital market in the face of the partial results of the currently running JEREMIE program’s investments.

The article also discusses how venture capital appears in the capital structure of the invested companies.

The selection of suitable companies is fundamental to the success of the investments; therefore the selection process of the venture capitalist is the basic pillar of the value creation itself. Alongside the high return expectations a great proportion of the major selection criteria are connected to the management of the companies.

The article describes how the value creation mechanisms appear in the return characteristics of venture capital investments in the US and Europe and attempts to evaluate the returns of the Hungarian market as well.

The section that discusses the financing background and prospects of university backed Hungarian spin-off companies reveals the problems and hindrances of venture capital financing in the case of these companies. In spite of the fact that spin-off companies cover just a segment of the potential targets of venture capitalists, based on their funding problems we can make some conclusions about the general problems of the industry.

Conclusion

My conclusion is that the government backed hybrid funds have a catalyst effect on the developing venture capital markets but in the long run the withdrawal of active involvement and an increasingly passive role can spur the industry on in the most effective way. The venture capital industry is able to contribute to economic growth and employment (via its value creation mechanisms) the most, if the venture capitalists operate under market conditions. Based on the comparison of Central and Eastern European countries the JEREMIE Program had similar effects on the region’s markets.

There is not a prevailing and generally used financial instrument that supports value creation the most, instead the ideal form depends on the characteristics of the deals and the companies.

As was described in the discussion of the limited managerial decisions, the managerial assistance of the investors creates additional value only if the investors are capable of cooperating with the management of the company. Therefore, besides capital and competence, cooperation is also a determinant of venture capital’s value creation and that is the reason why the personnel traits of the companies’ management play a crucial role in the selection process.

The most important problems of the Hungarian venture capital market identified in the research based on the Hungarian spin-off companies, were targeted and tried to be solved through the JEREMIE Program.

The examination of the demand side of the venture capital market can be a further research topic, in order to find the reasons of the insufficiency caused by the demand side. Another topic is to find a way in which the government could withdraw from the market in the long run to allow the market mechanisms to work independently.

References

- Becsky-Nagy, P. (2016). Korlátozott vezetői döntéshozatal, avagy a kockázati tőkés aktív szerepvállalása. Taylor Gazdálkodás-És Szervezéstudományi Folyóirat Virtuális Intézet Közép Európa Kutatására Közleményei. 25(4), 109-116.

- Becsky-Nagy, P. (2013). Venture capital in Hungarian academic spin-offs. Annals of the University of Oradea Economic Science, 1(2), 351-360.

- Becsky-Nagy, P., & Fazekas, B. (2015a). Speciális kockázatok és kezelésük a kockázatitőke-finanszírozásban. Vezetéstudomány, 46(3), 57-68.

- Becsky-Nagy, P., & Fazekas, B. (2015b). Investment or learning curve? – The effects of the EU and government funds on the development of the Hungarian venture capital market. Public Finance Quarterly, 60(2), 238- 248.

- Becsky-Nagy, P., & Fazekas, B. (2014). Returns of private equity: comparative analyses of the returns of venture capital and buyout funds in Europe and in the US. Annals of the University of Oradea Economic Science, 2(2), 820-827.

- Becsky-Nagy, P., & Karászi, E. (2015). Capital structure and venture capital. Annals of the University of Oradea Economic Science, 24(1), 783-791.

- Becsky-Nagy, P., Papp, Zs., & Tóth, E. (2014). A vidéki spin-off cégek létjogosultsága: debreceni és budapesti székhelyű spin-off vállalatok összehasonlító elemzése. Közgazdász Fórum/Economists Forum, 17(119- 120), 20-33.

- Becskyné Nagy, P. (2008). A kockázati tőke hozzáadott és “elvett” értéke: Elmélet és gyakorlat. Debreceni Egyetem, Közgazdaságtudományi Doktori Iskola, Doktori disszertáció. Debrecen, 255.

- Becskyné Nagy, P., & Biczók S. (2006). A kockázatitőke-befektetésekből történő kiszállás útjai. In Zs. Makra (Ed.), A kockázati tőke világa (pp. 53- 75). Budapest, Hungary: Aula.

- Bergemann, D., & Hege, U. (1998). Venture capital financing, moral hazard and learning. Journal of Banking and Finance, 22(6-8), 703-735.

- Berglöf, E. (1994). The control theory of venture capital finance. Journal of Law, Economics and Organization, 10(2), 247-267.

- Bottazzi, L., & Darin, M. (2002). Venture capital in Europe and financing of innovative companies. Economic Policy, (34), 229-269.

- Casamatta, C. (2003). Financing and advising: optimal financial contracts with venture capitalists. Journal of Finance, 58(5), 2059-2086.

- Cestone, G. (2000). Venture capital meets contract theory: risky claims or formal control? Working papers of University of Toulouse and Institut d’Analisi Economica Barcelona. Retrieved from http://pareto.uab.es/ wp/2001/48001.pdf

- Copeland, T. E., & Keenan, T. E. (1998). How much is flexibility worth? McKinsey Quarterly, (2), 38-49.

- Cornelli, F., & Yosha, O. (2003). Stage financing and the role of convertible securities. Review of Economic Studies, 70(1), 1-32.

- Cumming, D. J. (2005). Capital structure in venture finance. Journal of Corporate Finance, 11(3), 550-585.

- Dávid, Sz. D., & Becsky-Nagy, P. (2016). A kockázatitőke-befektetők kiválasztási kritériumai. Controller Info, 4(1), 22-29.

- Dubini, P. (1989). Which venture capital backed entrepreneurs have the best chances of succeeding? Journal of Business Venturing, 4(2), 123-132.

- Farkas, B., Gyallai, É., & Becsky-Nagy, P. (2016). A JEREMIE program tapasztalatai Közép-Kelet Európában. Közgazdász Fórum, 19(126), 88- 100.

- Fazekas, B. (2014). Government interventions in the venture capital market – How JEREMIE affects the Hungarian venture capital market? Annals of the University of Oradea Economic Science, 23(1), 883-892.

- Franke, N., Gruber, M., Harhoff, D., & Henkel, J. (2008). Venture capitalists’ evaluation of start-up teams: trade-offs, knock-out criteria, and the impact of VC experience. 32(3), 459-483.

- Glavanits, J. (2015). A kockázati tőkebefektetések egyes jogi kérdései. Győr, Universitas-Győr Nonprofit Kft, 319.

- Gompers, P. A. (1995). Optimal investment, monitoring and staging of venture capital. The Journal of Finance, 50(5), 1461-1489.

- Grilli, L., & Murtinu, S. (2014). Government, venture capital and the growth of European high-tech entrepreneurial firms. Milan, Italy: Politecnico di Milano.

- Halaska, G. (2012). Jeremie I. dosszié 5. rész: Euroventures. Retrieved from http://insiderblog.hu/blogzine/2012/10/31/jeremie-i-dosszie-5-reszeuroventures/

- Hall, B. H. (2002). The financing of research and development. The Oxford Review of Economic Policy, 18(1), 35-51. Hall, J., & Hofer, C. W. (1993). Venture capitalists’ decision making criteria in new venture evaluation. Journal of Business Venturing, 8(1), 25-42.

- Hudson, E., & Evans, M. A. P. (2005). A review of research into venture capitalists’ decision making: implications for European entrepreneurs, venture capitalists and researchers. Retrieved from http://epubs.scu. edu.au/cgi/viewcontent.cgi?article=1078&context=jesp

- Kaplan, S. N., Sensoy, B. A., & Strömberg, P. (2009). Should investors bet on the jockey or the horse? Evidence from the evolution of firms from early business plans to public companies. The Journal of Finance, 64(1), 75- 115.

- Kaplan, S., & Strömberg, P. (2003). Financial contracting theory meets the real world – An empirical analysis of venture capital contracts. Review of Economic Studies, 70(2), 281-315.

- Karsai, J. (1997). A kockázati tőke lehetőségei a kis- és középvállalatok finanszírozásában. Közgazdasági Szemle, 44, 165-174.

- Karsai, J. (2015). Állami szerepvállalás a kelet-közép-európai kockázatitőkepiacon. Közgazdasági Szemle, 62(11), 1172-1195.

- Karsai, J. (2014). Fából vaskarika? Az állam mint kockázatitőke-befektető. Külgazdaság, 58(9-10), 3-34.

- Kogut, B., & Kulatilaka, N. (2001). Capabilities as real options. Organization Science, 12(6), 744-758.

- Leland, H. E., & Pyle, D. H. (1977). Informational asymmetries, financial structure, and financial intermediation. The Journal of Finance, 32(2), 371-387.

- Lerner, J. (1996). The government as venture capitalist: the long-run impact of the SBIR Programme. NBER Working Papers Series, Working Paper 5753, National Bureau of Economic Research Cambridge. September, 1-33. Retrieved from http://www.nber.org/papers/w5753.pdf

- Ludányi, A. (2002). A tőkeerő és az alapítói háttér hatása a kockázatitőkeszervezetek befektetési magatartására I-II. rész. Közgazdasági Szemle, 49(7-8), 659-672 and 779-798.

- Luukkonen, T., Deschryvere, M., & Bertoni, F. (2013). The value added by government venture capital funds compared with independent venture capital funds. Technovation. 33(4-5), 154-162.

- Mason, M. C., & Harrison, R. T. (1998). Stimulating investments by business angels in technology-based ventures: The Potential of an Independent Technology appraisal service; In: R. P. Oakey & W. During (Eds.) New Technology-based firms in the 1990; Volume 5 (pp. 81-96). London, Great-Britain: Paul Chapman.

- Marx, L. M. (1998). Efficient venture capital financing combining debt and equity. Review of Economic Design, 3(4), 371-387.

- Myers, S. C. (1984). The capital structure puzzle. Journal of Finance, 39(3), 575-592.

- Myers, S. C. (2001). Capital structure. The Journal of Economic Perspectives, 15(2), 81-102.

- Myers, S. C., & Majluf, N. C. (1984). Corporate financing and investment decisions when firms have information that investors do not have. Journal of Financial Economics, 13(2), 187-221.

- Norton, E., & Tenanbaum, B. H. (1993). Specialization versus diversification as a venture capital investment strategy. Journal of Business Venturing, 8(5), 431-442.

- Osman, P. (2008). Az üzleti angyalokról. Pénzügyi szemle. 53(1), 83-99.

- Petty, J. S., & Gruber, M. (2011). „In pursue of the real deal”: A longitudinal study of VC decision making. Journal of Business Venturing. 26(2), 172- 188.

- Philott, T. (1994). Banking and new technology small firms: a study of information exchanges in the financing relationship. In R. P. Oakey & W. During (Eds.), New technology-based firms in the 1990, Volume 5 (pp. 68-80). London, Great-Britain: Paul Chapman.

- Prowse, S. (1998). The economics of the private equity market. Federal Reserve Bank of Dallas Economic Review, Third Quarter, 21-34.

- Rasila, T., Seppa, M., & Hannula, M. (2002). V2C or venture-to-capital: New model for crossing the cash between start-up venture and venture capital. E-Business Research Center, Tampere University of Technology: Tampere.

- Reid, G. C. (1999). The application of principal-agent methods to investorinvestee relations in the UK venture capital industry. Venture Capital, 1(4), 285-302.

- Sahlman, W. A. (1990). The structure and governance of venture-capital organizations. Journal of Financial Economics, 27(2), 473-521.

- Schilder, D. (2006). Public venture capital in Germany: Task force or forced task? Freiburg Working Papers. TU Bergakademie Freiberg, Faculty of Economics and Business Administration.

- Schmidt, K. M. (2003). Convertible securities and venture capital finance. Journal of Finance, 58(3), 1139-1166.

- Shepherd, D. A., Zacharakis, A., & Baron, R. A. (2003). VCs’ decision processes: Evidence suggesting more experience may not always be better. Journal of Business Venturing, 18(3), 381-401.

- Silva, J. (2004). Venture capitalists’ decision-making in small equity markets: a case study using participant observation. Venture Capital, 6(2/3), 125- 145.

- Trester, J. J. (1998). Venture capital contracting under asymmetric information. Journal Banking and Finance, 22(6-8), 675-699.

- Tyebjee, T. T., & Bruno A. V. (1984). A model of venture capitalist investment activity. Management Science, 30(9), 1051-1066.

- Vohora, A., M., Wright, & A. Lockett (2004). Critical junctures in the growth in university high-tech spinout companies. Research Policy, 33, 147–75.

- Wright, M., Hoskisson, R. E., & Busenitz, L. W. & Dial, J. (2001). Finance and management buyouts: agency versus entrepreneurship perspectives. Venture Capital Journal, 3(3), 240.

- Wright, M., A., Lockett, B., Clarysse, & M. Binks (2006). University spin-out companies and venture capital. Research Policy, 35, 481–501.

- Zoppa, A., & McMahon, R. G. (2002). Pecking order theory and the financial structure of manufacturing SMEs from Australias’s business longitudinal survey. Small Enterprise Research, 10(2), 23-42.

Biographical note

Patrícia Becsky-Nagy, Ph.D. is an Assistant Professor at the University of Debrecen, Faculty of Economics, Institute of Accounting and Finance, Department of Finance. The author graduated from the predecessor faculty of her workplace and received a PhD degree at the Doctoral School of Economics in 2008. Her main research field is the value creation of venture capital, but she is also interested in the value measurement methods in IFRS. The process of her habilitation was recently finished, and this article is a summary of her article collection about the research made after her Ph.D. dissertation.