Received 10 August 2022; Rejected 1 March 2023; Revised 29 May 2023; Accepted 17 July 2023.

This is an open access paper under the CC BY license (https://creativecommons.org/licenses/by/4.0/legalcode).

Piotr Łasak, Ph.D. Hab., Associate Professor, Institute of Economics, Finance and Management, Jagiellonian University, ul. Prof. S. Łojasiewicza 4, 30-348 Kraków, Polan, e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it., corresponding author.

Sławomir Wyciślak, Ph.D., Associate Professor, Institute of Economics, Finance and Management, Jagiellonian University, ul. Prof. S. Łojasiewicza 4, 30-348 Kraków, Poland, e-mail: This email address is being protected from spambots. You need JavaScript enabled to view it.

Abstract

PURPOSE: The banking sector is under intense pressure from digitalization. One of the accompanying processes is the development of digital platforms and platform ecosystems in banking services. The paper aims to present the dynamic pattern of behavior among partners stemming from the tensions between governance costs and co-created value within platforms in banking services. METHODOLOGY: The study employs an approach based on a systematic literature review of 54 publications selected from Scopus and WoS databases. We applied an approach that consists of two steps. The first step of the research was a literature review and critical analysis of the sources related to our research questions. In the second step, we propose a causal loop diagram research procedure, which is a research system dynamic tool used in modeling system dynamics. FINDINGS: There are different types of platforms, and among the most important are blockchain-based and cloud-based platforms. In both types, the relations between owners, complementors, and customers are important. The tension between governance costs and co-created value informs behavior patterns among platform partners. The degree of interconnectedness between platform participants and the level of centralization of banking services depends on the platform type. The study highlights that blockchain-based and cloud-based platforms play a significant role in the transformation of the current banking services. The choice of platform type has important implications for the platformization of banking services. IMPLICATIONS: The pattern of behavior among platform partners identifies the self-reinforcing dynamics that suggest how managers can navigate the tension over time amidst the asymmetry of benefits and risks. The research findings can be informative for financial regulators and they help work out a policy that reduces the asymmetry of benefits and contributes to the more sustainable development of digital platforms. ORIGINALITY AND VALUE: This paper addresses the paradox perspective on the banking sector changes during the intensive processes of digitalization and the creation of new ‘platform ecosystems.’ This topic has not been studied in this context so far.

Keywords: banking services, banking sector transformation, blockchain-based platforms, cloud-based platforms, paradox theory, blockchain, cloud

INTRODUCTION

Digital platforms transformed the step-by-step arrangement to produce, distribute, and sell a product. They leverage the networked relationship of consumers, producers, and prosumers. Such processes are visible in the real economy and financial services, especially in the banking sector. The platformization of banking services enables transformation from linear business provision to non-linear business models, where services are offered in real-time. The changes embrace especially the move from output-based business models to outcome-based models, focused on customers and their needs (Sironi, 2021).

The financial sector is currently undergoing a very far-reaching digital transformation. Banking services are offered to a lower degree by traditional banks, organized on a hierarchical structure, but are often submitted via other forms of institutions and structures (Avarmaa et al., 2022; Caron, 2018; Omarini, 2021). One of these solutions is financial platforms. Platform-based banking services are becoming common place and leading to new ‘platform ecosystems’ (Claessens et al., 2018, Frost, Turner, & Zhu, 2018; Langley & Leyshon, 2021). The banking sector’s transformation is non-homogeneous. Some incumbent banks implement technology to improve the efficiency of their activity (preservation). Others are entering market-oriented structures, like modularized networks or open ecosystems (Finken & Finkemeyer, 2019; Gozman et al., 2018; Hedman & Henningsson, 2015; Premchand & Choudhry, 2018). During such changes, the structure of the banking sector also changes, and some of these services are modified while others are newly created (Łasak & Gancarczyk, 2021). The development of banking platforms is also favoured by the incorporation of other entities into these platforms. They include, among others, e-commerce entities, insurance, telecommunications, shipping services, and many more (Omarini, 2020). Links between banks and other entities result in the dynamic development of the area treated as Banking-as-a-Service (BaaS). All of the transformation processes of the banking sectors are leading to significant changes in the bank’s business models. Among other processes, an important one is the development of banking platforms and their growing role in this sector. These changes and processes prompted us to formulate our first research question (RQ):

RQ1) What are the specific types of digital platforms in banking services?

The development of digital platforms in banking is becoming a significant issue (Zachariadis & Ozcan, 2017). One of the critical facets related to these processes is the governance mechanisms. The first important aspect is who is the platform provider (owner). Sometimes, it is a bank, and sometimes the provider is an external entity. While the platform owner’s leading role is crucial, simultaneously unambiguous, and equally important from the platform’s operational perspective are complementors. Despite a strong consensus among scholars regarding complementors as particularly important in markets with network effects such as platforms (Omarini, 2020), most studies with a direct or indirect focus on the complementor role in the ecosystem consider complementors universally and homogenously (Huber et al., 2017; Sironi, 2021). A scientific consensus on distinguishing and classifying complementors is still lacking, although complementors differ significantly in numerous dimensions, including size, experience, financial background, strategic orientation, or motivation. Platform owners need to understand the heterogenous complementor structure in their ecosystem to adapt their governance rules accordingly and ensure the platform’s long-term success (Deilen & Wiesche, 2021). When taking into account a customer-centric approach, it is also necessary to indicate the very important role of customers in banking services and their expectations. Based on such premises, we formulated the second research question (RQ):

RQ2) Who are the partners (owners, complementors, customers) of digital

platforms in banking services, and what are their roles?

Every platform has its structure made by platform owners, complementors and customers. It should be noted, however, that the entire banking system is undergoing profound transformations. The platform participants are interconnected to varying degrees, have different levels of trust, and share information to varying degrees. The participation in a platform may result in further consequences for various entities. Their involvement in the platform may be associated with a different level of governance costs, impacting different co-created values and generating an asymmetry of benefits. Banks, when incorporating financial technology, expect the preservation of customer relations and greater efficiency in their activities. The non-bank entities (FinTech-based companies) want to expand their services and expect more significant participation in the banking market. All of these dynamics may create tensions between different partners and impact the ultimate shape of the platform structure. To examine these processes, we formulated a third research question (RQ):

RQ3) What is the dynamic pattern of behavior among partners stemming from

the tensions between governance costs and co-created value within

platforms in banking services?

Platform governance is a crucial aspect of the platformization of financial services. It embraces the problem of coordinating the relations between different platform participants. Governance of a platform also strongly influences all other aspects of the functioning of the platforms (Adner, 2017; Rietveld & Schilling, 2021). The processes of banking sector platformization, including platform governance, may largely depend on the type of technology used. Among them are blockchain and cloud technologies, which are successfully used to build a new banking sector structure and significantly impact platforms’ development in banking services.

Our study contributes to the literature dedicated to the technology-driven transformation of the financial markets. There are numerous studies related to the impact of technology on the market structure of financial services (Arslanian & Fischer, 2019; Jacobides et al., 2018; Scardovi, 2017; Tanda & Schena, 2019) and the banking industry (Łasak & Gancarczyk, 2022; Rajnak & Puschmann, 2021; Tanda & Schena, 2019; Wewege & Thomsett, 2019). In this article, we focus on banking platforms development, as they are, in our opinion, still poorly researched.

The article provides three contributions to the extant literature on the platform-based transformation of the banking sector. Firstly, we described platform-based banking structures and governance of banking. Secondly, we provided the taxonomy of the digital platforms operating in the banking sector. Thirdly, we elaborated a theoretical, conceptual model of a pattern of behavior mechanisms emerging amongst platform partners. Based on our research, we provided conclusions on the types of platforms shaped by the behavior of the platform participants (owners, complementors, and customers).

The methodology and aims of our research are presented in the second section. The third section specifies the theoretical aspects related to the platforms, which are crucial in the context of our study. In section four, we present the taxonomy of platforms in banking services. Section five contains the conceptualization of behavior among platform partners. Section six presents a discussion and contribution to the theory, whereas in section seven, we present our conclusions.

METHODOLOGY AND AIMS OF THE RESEARCH ANALYSIS

Our research begins with general research questions, and from these general assumptions, we logically deduce what specific implications can be derived. In our approach, we used the desk research method. The first step of the research was a literature review and critical analysis of the current literature. The research questions guided the development of a literature review. This comprehensive analysis provided an initial understanding of the research topic, which allowed the authors to discern existing knowledge gaps. Pre-formulated research questions informed the further literature review. The RQ1 was the driver for the selection of keywords “digital platforms” and “banking services,” whereas RQ2 informed keywords “platform owners,” “complementors,” “banking platform customers,” “banking platform services.” RQ3 triggered keywords including “digital platform governance,” “tensions,” and “paradox theory.” The literature search was performed in the Scopus and WoS databases, where we selected and reviewed 54 publications related to our research questions. We skimmed through the full-text articles to evaluate further the quality and eligibility of the studies and conducted the literature review iteratively. Using the list of references at the end of each article informed about the most critical papers in researched fields and turned out to be the most efficient narrative, literature review strategy. We focused on the most relevant authors in the researched fields (these included Arslanian & Fischer, 2019; Baldwin & Woodard, 2008; Clarke, 2019; Gozman et al., 2018; Jackson, 2017; Langley & Leyshon, 2021; Nicoletti, 2021; Scardovi, 2017; Sironi, 2021; Tanda & Schena, 2019). The literature review informed the research phase on identifying specific types of digital platforms and partners (Table 1). We applied the thought process, which combined analysis and synthesis.

Table 1. Phases of the research procedure

|

Phase |

Information gathering |

Information analysis |

Theorizing mode |

Research question |

|

Studying problems in the context |

Literature review |

Classifications of digital platforms in banking services Identification of banking services which can be offered via digital platforms and platform ecosystems Identification of partners (owners, complementors, customers) of digital platforms |

Inductive analysis Synthesizing |

RQ1 RQ2 |

|

Proposing solutions |

Literature review, coding at the first level, searching for conceptions |

Defining the causal loop diagram |

Analysis Abstracting Synthesizing Idealizing |

RQ3 |

|

Creation of the research framework |

Literature review, coding at a second level according to research questions (RQ2, RQ3), searching for conceptions |

Analysis of the impact of patterns of behaviors of platform participants on the platforms deployability Analytical generalization based on patterns |

Inductive Deductive |

RQ3 |

|

Conceptualization of the solutions |

Coding insights and proposals |

Building insights on our research framework, outlining the future research avenues |

Inductive Deductive |

RQ3 |

In the second step of the research procedure, we proposed a causal loop-diagram research procedure, which is a research system dynamic tool. The Causal Loop is a tool used in modeling system dynamics. Causal loop diagrams emphasize the feedback structure of a system. A causal loop diagram consists of variables connected by arrows denoting the causal influences among the variables. The important feedback loops are also identified in the diagram. Causal links, shown by arrows, relate to variables. Each causal link is assigned a polarity, either positive (+) or negative (-), to indicate how the dependent variables change (Sterman, 2000). We used a causal loop diagram to answer RQ3. In the theorizing process, we applied analysis, synthesizing, abstracting, and idealizing. Synthesizing in the manner of abstracting and idealizing resulted in the causal loop diagram. We employed a synthesis process involving abstraction and idealization, culminating in a causal loop diagram. The transition from an inductive approach (in response to RQ1) to a synthesis-driven methodology facilitated the development of a theoretical framework. This emergent product succinctly encapsulates progress while providing direction and serving as a theoretical reference point, effectively integrating the research outcomes in a coherent, scientifically rigorous manner. Causal loop diagrams, when used with stock and flow diagrams, serve as valuable tools for elucidating intricate relationships within complex systems. These diagrams can be employed to model system dynamics and the dynamics of tensions, offering enhanced clarity regarding sequences, varying degrees of determinacy in relationships, and nuances of pathways and influences. By integrating causal loop diagrams and stock and flow diagrams, researchers and practitioners can better understand the interdependencies and causal mechanisms at play within a given system (Weick, 1995). The conceptualization of the solution leverages abstraction to create a comprehensive understanding that transcends specific temporal, spatial, and individual contexts. This approach aligns with principles of generalization and abstraction that are integral to various scientific disciplines.

Following Merton (1968), we assume that middle-range theorizing is an appropriate approach for understanding platforms phenomena since it aims at integrating theory and practical observations to explain such complex phenomena. In addition to middle-range theorizing, we also employ systems thinking to understand complex phenomena by examining the relationships, feedback loops, and dynamics within a system. Using causal loop diagrams in the research process helps us visualize and analyze the causal relationships among variables and the feedback structure of a system. The paradox perspective can respond to tensions by using the value of case studies, action research, systems approaches, and agent-based models to enable more nuanced insights (Smith & Lewis, 2011). It has been asserted that paradoxical thinking epitomizes systems thinking (Wirsbinski, 2008). Systemic thinking seeks to understand phenomena holistically and elementarily. In contrast, paradoxical thinking is an ontological perspective that appreciates the plurality of phenomena and accepts the notion that underlying explanations require a “both” rather than an “and/or” commitment to understanding (Glassburner et al., 2018).

THE THEORETICAL CONCEPT OF DIGITAL PLATFORMS

Governance

Platform governance can be interpreted as a mechanism affecting the cooperation and coordination of their members (platform participants) and establishing technological standards for connectivity. Connectivity relates to the technological infrastructure through which information is conveyed, and information sharing links to the quality of the information being shared (Brandon-Jones et al., 2014). Platform governance refers to the mechanisms through which a platform owner exerts influence over other participants in the ecosystem (Tiwana et al., 2010; Hein et al., 2020). The platform ecosystem participants typically involve a central actor (platform owner or hub firm) and complementors. The platform owner orchestrates value creation and value appropriation by engaging complementors to operate in the platform ecosystem (Deilen & Wiesche, 2021). Considering platform governance, we refer to the lead firm primarily responsible for the platform as the platform owner (Tiwana, 2014). Platform complementors provide complementary goods to the ecosystem, defined as any other product or service that enhances the attractiveness of the focal product or services, such as add-ons, extensions, or modules. Hence, the success of a platform depends on active complementors who develop innovative complementary goods to stimulate user demand for the platform (Deilen & Wiesche, 2021).

Governance of platform ecosystems is a process of considerable variation and change in practicing ecosystem-wide rules and values. Governance rules mainly include decision-making power and access ownership of the platform system, participation in the ecosystem, and division of labor rules, platform pricing, and value distribution policy (Yiling et al., 2019).

The platform owner facilitates information sharing between autonomous complementors and consumers in an ecosystem (de Reuver et al., 2018). A platform’s governance design encompasses three perspectives: governance by sharing responsibilities and authority, governance by aligning incentives, and governance by sharing stakes (Tiwana et al., 2010). Governance of platform has tangible consequences for co-created value and governance costs. Co-created value is defined as the tangible and intangible benefits resulting from the combination of resources of the partners. Platform owners minimize governance costs early in the partnership by closely following the rules, and impacting co-created value. Over time, some complementors can increasingly attract the platform owners’ attention by demonstrating that the partnership has substantial co-creation potential (Omarini, 2020). Governance costs are the effort borne by the partners arising from planning, adapting, and safeguarding the resources (coordination costs) contributed to the partnership (Huber et al., 2017). They also embrace the costs of transferring the services to the platform and maintaining this platform. They also embrace the costs of employment competencies, costs of time that the individual participants of the platform devote to establish a consensus on the principles of cooperation, costs of platform development, etc. Pricing and revenue sharing has been studied as governance mechanism in platform ecosystems. It refers to payment flows within the platform ecosystem and how they are distributed between the different stakeholders (Schreieck et al., 2016). Researchers agree that platform pricing should follow a divide-and-conquer strategy, meaning that one side of the market is subsidized (divide). In contrast, the other side is priced at a premium to recover losses from the other side (conquer). Even in the absence of profits, platforms are often willing to set very low prices, i.e., predatory pricing. This pricing strategy results in considerable losses for a platform to scale quickly, undercut competitors, and build up market dominance by increasing the platform size (Hermes et al., 2020).

Paradox theory

Paradoxes, by their nature, denote persistent contradictions between interdependent elements. The paradox theory stems from the organizational-research field, which has developed over the last two decades. According to this theory, a paradox is understood as contradictory yet interrelated elements that seem logical in isolation but seem absurd and irrational when they appear simultaneously (Lewis, 2000). Two core characteristics describe a paradox: contradictions and interrelatedness (Schad et al., 2016). This definition emphasizes that the underlying logic for each element may seem rational when dealt with separately but it appears to be inconsistent when contrasted against each other. Thinking in terms of paradox demands that managers accept and work with contradictory elements instead of suppressing one of the elements (Lewis & Smith, 2014). Paradox as a meta-theory offers a powerful lens for management science, providing a deeper understanding of constructs, relationships, and dynamics surrounding organizational tensions, while enriching extant theories and processes of theorizing. Paradox as meta-theory deals with principles of tensions and their management across multiple contexts, theories, methodological approaches, and variables (Lewis & Smith, 2014; Schad et al., 2016).

Paradoxes cause tensions for actors when they try to make sense of them. At the same time, tensions are inherent in every paradox (Smith & Lewis, 2011). Managers should accept rather than deny or suppress the contradictory nature of a paradox and seek to create synergies between the paradoxical elements (Wilhelm & Sydow, 2018). Managing approaches – or responses – to paradoxes; that is, responses are either built on a structural separation of the contradictory elements or the acceptance of the co-existence of these elements and the search for synergies between elements. The synergistic approach is the most favored by paradox researchers but poses high requirements for managers regarding their ability to deal with emotional uncertainties and ambivalence. The synergistic approach thus requires managers to develop a high level of “paradoxical cognition” (Wilhelm & Sydow, 2018).

Tensions in digital platforms

The success of digital industrial platforms largely depends on their ability to attract an active ecosystem of actors. However, motivating actors to join a platform ecosystem is one of the critical challenges in platform establishment, often labeled as the “chicken-or-egg problem” (Tiwana, 2014). Hence, platform governance requires addressing several interdependent tensions, including the need to balance platform openness and control, exerting influence over the quality and range of complements, managing simultaneous collaboration and competition with complementors, and creating ecosystem value while also capturing some of that value (Rietveld & Schilling, 2020). All platform systems exhibit tensions between platform owners and complementors. For multi-sided platforms, the main threat is disintermediation. By replicating or reverse-engineering the platform side of these interfaces, rivals may be able to “clone” the platform itself and compete with it directly (Baldwin & Woodard, 2008). Complementors strive for competitive differentiation, focusing on their portfolio of domain expertise, market mechanisms, relational capital, and sector knowledge to create locally relevant solutions (Saadatman et al., 2019). Managing complementor engagement is rife with contradictions (Wareham et al., 2014). To foster generativity (i.e., evolvability) the independence of complementors, who work autonomously to satisfy customer needs, must be promoted and facilitated. To create and maintain a coherent, shared identity for the platform (i.e., stability), however, complementors’ pursuit of their interests must be balanced with the interests of other players in the ecosystem (Eaton et al., 2015; Eisenmann, 2008; Parker et al., 2016). While there is ample research on the challenge of balancing a platform’s stability with its evolvability (Dattée, Alexy, & Autio, 2018; Tilson, Lyytinen, & Sørensen, 2010), it focuses predominantly on governance mechanisms as the primary means for reconciling these competing demands (Lindgren, Eriksson, & Lyytinen, 2015). Platforms thus need to balance the complementarity and competitiveness among complementors (De Reuver et al., 2018), which implies managing the contradiction between a platform’s evolvability to foster generativity and its stability to enable efficiency and complementors’ value capture (Sarker et al., 2012; Wareham et al., 2014). Tensions in pricing and the provision structure between platform owner and complementor illustrate the asymmetries in the negotiating power between the platform owner and complementor. The imbalances and power asymmetries entail the risk of a loss of trust between a platform owner and complementor. However, trust is a significant factor in the relationship between the platform owner and complementor for the platform’s long-term success. A fair and sustainable governance structure has a significant positive impact on the motivation of complementors to engage on the platform (Deilen & Wiesche 2021).

Digital platforms in financial services

Digital platforms are significant in numerous aspects of social lives. This necessitates the characteristics of the platforms. One example of taxonomy for digital platforms recognizes them on the basis of three perspectives: technological, economic and socio-cultural. It divides technological perspective into owner access, user access, technology access, and pricing mechanism dimensions. Economic outlook can be divided into geographic scope, ownership, control, value proposition, transaction content, transaction type, market orientation, primary revenue source, and platform type dimensions. A socio-cultural perspective is related to user constellation, relationship level, and participation mechanism (Freichel et al., 2011). Another dimension of platforms’ taxonomy is oriented on aspects such as value creation, platform architecture, and actor ecosystem (Abendroth et al., 2021).

The presented taxonomies are important in the context of platform governance and tensions stemming from the governance. They also shed light on the possible platformization of the banking industry. When considering business-oriented dimension, attention should be paid to such aspects as value creation (platform structure, critical activity or interactions), platform participants, revenue model, and the platform value chain (coordination, accessibility, economies of scale, etc.) (Staub et al., 2021). These platform-related characteristics are considered in the context of digital platforms in the banking ecosystem (Gancarczyk & Rodil-Marzábal, 2022; Omarini, 2018).

The digitalization of financial services characterizes the current stage of the development of financial technology. The process is strictly connected with the emergence of the open application programming interfaces (APIs) economy and platform business model development (Omarini, 2020; Scardovi, 2017). It must be highlighted that the meaning of “platform” in banking differs from that in the meaning of the IT world. Banking platforms are treated as facilitators for third parties and their customers (Gozman et al., 2018). Nowadays, however, it is very common that some banking services (e.g., credit) are offered by electronic platforms that are not operated beyond the traditional banking sector (Claessens et al., 2018). The platform business models developed in the last few decades have significantly impacted incumbent financial institutions. The models changed the traditional vertical integration of such institutions as banks into a new, more innovation-centric approach to value creation (Zachariadis & Ozcan, 2017). The future trends predictions highlight that the trend will continue and digital platforms will dominate business and financial institutions in the future. Digital platforms in banking rely on innovative activities and offer many practical solutions for individual consumers and SMEs. One of the most important processes is the move towards a customer-centric approach (Moro-Visconti, Rambaud, & López Pascual, 2020). They are more preferred by customers when compared to traditional brick-and-mortar banks (Moro-Visconti et al., 2020).

Banks or non-banking entities create many bank-based services’ platforms. They organize typical banking/financial activities like payment, lending, or wealth management (Caron, 2018; Sironi, 2021). Traditionally, banks served as gatekeepers for financial services, but nowadays, strong competition has been observed in the area, leading to disaggregation of the traditional banking value chains (Bartolacci et al., 2022; Pollari, 2018). It should be noted that usually, banks lack the innovative capacity to provide digital platforms. For this reason, they need non-banking FinTech business entities for the creation of such platforms (Bhutto et al., 2023). The growth of technology-based banks or non-bank entities offering banking services is based on the contemporary worldwide trend towards financial inclusion (Kanungo & Gupta, 2021). Technology is empowering financial firms to open previously untapped markets. (Chen et al., 2022) highlight that the application of more advanced technology enriched banking services. Payment or lending services are among those that play a key role in this process (Clarke, 2019). The typical platform is multi-sided, linking customers, financial service providers, and stakeholders. Usually, such platforms connect banks, their clients, and FinTechs, creating a financial intermediation ecosystem (Moro-Visconti et al., 2020). FinTechs have the technology that can increase banks’ efficiency.

On the other hand, banks have large customer bases, abundant capital, and legal and regulatory expertise (Pedersen, 2020). There are also platforms based on social contacts (social finance). Such kinds of services emerged in the early 2000s, and lending platforms became one of the most significant players (Clarke, 2019). Currently, consumers spend a lot of their time online on digital devices, and financial institutions are forced to follow their behavior patterns and offer suitable interaction tools. An example is Lending Club – one of the world’s largest peer-to-peer lending platforms (Nicoletti et al., 2017). The global economy is beginning to concentrate around a few large entities, which include companies defined as BigTechs. Among them are names like GAFA (Google, Amazon, Facebook, Apple) and BAT (Baidu, Alibaba, Tencent) (Szpringer, 2020). BigTechs create platforms that provide financial services. The changes show that the crucial aspect of the platformization of the banking industry is who is orchestrating the whole process. In the best scenario, banks should decide whether to create their own digital platform or partner with third-party platform owners (Boot et al., 2017). At the current stage of digital transformation, banks develop collaboration with FinTechs and are transforming their structures into a platform (Stasinakis & Sermpinis, 2020). This is the only solution enabling competitiveness in the future (Murinde et al., 2022). Jackson (2007) predicts that the way to be more competitive in the future is to offer products and services provided by many players instead of one entity(Jackson, 2017).

The entrance of platforms into the banking business is inevitable, and banks must prepare a suitable strategy to defend themselves or cooperate in the platform-based environment (Omarini, 2018). It is essential to consider the possible different roles of banks in the environment. These institutions might be providers of these platforms, but they also can be treated as external participants in platforms created by non-bank institutions. In such cases, platforms might be created by other entities of the services distribution channel or even external, non-financial companies (BigTechs). It is, however, a new process of emerging platforms that connect market participants, bypassing the traditional banking sector. The involvement of the new, non-bank participants may increase the dexterity of the whole service provision process (Kotarba, 2018). Such a situation is possible, especially in these locations, where traditional banks cannot provide banking services to some parts of society (Croxson et al., 2021). The literature highlights that digital platforms (FinTech-based platforms) are not only complementors for traditional banks, but sometimes they also substitute the incumbent financial entities (Bilan et al., 2019).

Banks use platforms to improve their services or services provision. When considering platform structure, they mainly focus on costly, arduous, or repetitive processes (Nicoletti, 2021). The range of banking services that a platform-based model can implement is extensive. There are, however, some determinants of offering services via platforms. The most important is the level of openness to which the platform owner(s) decides. Traditional banks are less willing to set up a comprehensive open banking model, whereas challenger banks quickly accept the platform-based model. However, full-digitalization might be a sub-optimal approach, and banks contrapose volume-oriented product channels with value-oriented banking relationships. The crucial characteristics defining the capabilities to develop the services based on the platform are transparency about data sources, stakeholder incentives, client costs, and ecosystem consequences. The greater intensity of these elements defines a greater possibility of offering banking services in the form of a platform-based business model (Nicoletti, 2021; Sironi, 2021).

Nowadays, blockchain-based and cloud-based platforms are among the fastest-growing platforms in terms of the use of technology. They bind various participants in the distribution of the banking services (examples are presented in Table 2). Both these platforms link internal and external capabilities and generate additional value for the participants and their customers. The main difference between blockchain and cloud technology is that blockchain relies on decentralization (distributed storage), whereas cloud computing leads to centralization (centralized storage) (Farrow, 2020; Hon & Millard, 2018; Zheng & Lu, 2021).

Table 2. Identification of platform owners, complementors and market participants in blockchain and cloud platforms

|

Type of services |

Platform owner |

Complementor(s) |

Market |

|

Example 1. Ethereum – blockchain platform for money and new kinds of applications |

|||

|

Cryptocurrency blockchain platform, banking services |

Private owners: Anthony Di Iorio, Charles Hoskinson, Gavin Wood, Joseph Lubin, Mihai Alisie, Vitalik Buterin |

Commerce and e-commerce: Amazon, Amalto, BNP Paribas, Citigroup, Hewlett-Packard Enterprise, Samsung, Siemens and many more Exchanges: Ox, Kyber Network, Loopring; Stablecoins: MekerDao’s DAI, Circle USDC, Trust Token’s TrueUSD Lending: MakerrDao’s CDPs, Dharma’s lending services, Compound’s borrowing pools Asset management: Melonport’s asset management platform, Compound’s money-market funds, Iconmi’s crypto indices Derivatives: CDX’s, Augur’s various prediction markets |

Retail customers, small and medium-sized enterprises |

|

Example 2. Tink – cloud-based platform as a service |

|||

|

Lending, payments, and many other services – access aggregated financial data, initiate payments, verify account ownership and use many personal finance management tools |

Visa |

Ecolytiq (developer of financial transaction platform), Wealthify (digital investment platform), Kivra (Swedish digital mailbox provider), Lydia (payment FinTech), American Express, Google, Sopra Banking Software, ABN AMRO Bank N.V., commercial banks (BNP Paribas, NatWest, Nordea) |

Big banks, FinTechs and start-ups in Europe. It integrates more than 3,400 banks in 18 European countries |

Source: Own elaboration based on the literature.

The application of blockchain in banking enables a new form of organization of banking services (Kumari & Devi, 2022). Such technology enables connecting consumers and producers directly through the platform, without the need for bank’s participation. Moreover, this technology has many benefits, like alleviating information asymmetry and reducing the risk of specific operations (Mehrotra et al., 2020; Wang et al., 2019). The blockchain-based platform presents decentralized decision-making in which the community around the platform suggests changes to the code and rules of the platform but also decides which of these changes will be implemented (Pereira, Tavalaei, & Ozalp, 2019). An example of such a platform is Ethereum, a blockchain platform that supports smart contracts (van der Merwe, 2021). The platform enables transactions to be confirmed (order or validate) without the traditional participants, like banks or credit card companies (Oliva et al., 2020). It provides such advantages for the customers as anonymity, safety, and time-saving. Moreover, the application of blockchain technology positively stimulates the development of banking services in the context of the emergence of new, non-bank forms of financing, especially small and medium-sized enterprises (SMEs). The research in this area shows that in certain circumstances, the use of blockchain banking platforms gives much better financing opportunities for SMEs than independent finance (Liu et al., 2021). They also improve the efficiency of many banking services offered to retail customers.

The second type of technology that plays a significant role in the modern banking industry and its platformization is cloud technology. Cloud computing refers to the creation of on-demand access to a pool of configurable computing resources such as networks, servers, storage, applications, and services. Cloud technology has experienced rapid growth during the last few years and provides many advantages for incumbent institutions. Cloud-based platforms provide some benefits that blockchain-based platforms do not offer. They allow the combination of data analytics (Big Data) with artificial intelligence. In this way, many services previously provided by banks are automated. Such services are offered via mobile devices (smartphones), making them faster and cheaper than traditional banking services. As Boot et al. (2021) highlighted, the widespread adoption of cloud computing enables large technology firms to create an ecosystem together with banks and other parties. The role of cloud technology as the infrastructure that lowers the entry barriers to the banking sector is significant. It enables the development of new, digital financial products and services that match customer needs and enable banks to cooperate with specialized FinTech firms (Nedelcu et al., 2015). The advantages of this technology come from the fact that this technology enables all collaborating partners to interact effectively, efficiently, and transparently (Nicoletti, 2021; Walker & Morris, 2021). An example of a cloud technology platform is the Swedish platform Tink. It is Europe’s leading open banking platform and enables banks and FinTechs to develop data-driven financial services. The platform is based on cloud technology, and is treated as an ‘infrastructure provider’. Its primary focus is personal financial management aggregation (Teigland et al., 2018). The company collaborates with over 3,400 incumbent banks and has 250 million customers.

Conceptualizing behavior patterns among platform partners

The application of blockchain and cloud technologies in banking provides many benefits for the industry, the non-bank participants on the platform, and their customers. Platform-based business models utilizing the application of blockchain technology reduce transaction costs through standardization and improved transparency (Perscheid et al., 2020). It also improves the efficiency of internal processes (e.g., the cloud-based HRM platforms in banks’ back offices) (Łasak & Gancarczyk, 2022). It is an opportunity for banks to partner with FinTech companies and gain many benefits from such cooperation. Apart from specific economic benefits, like greater efficiency and effectiveness, the platform-based approach creates a new dimension of banking services. It is highlighted in the literature that such a solution enables almost instantly a funnel of innovative value-generating units that accelerate growth (Sironi, 2021).

The current phase of banking services development leads to intense cooperation and competition (coopetition) between different market participants. Diamond et al. (2019) highlight that the strongest competition for banks comes from FinTechs and businesses representing other industries. The coopetition of banks on digital platforms with external partners and between different non-bank actors entails new risks and threats that banks do not experience when offering their services independently (Arslanian & Fischer, 2019). An example is the possible risks of using private data and negative externalities for consumers from the misuse of personal data (Croxson et al., 2021). All of these adverse outcomes of the bank-non-bank cooperation create costs. Among them are included governance costs.

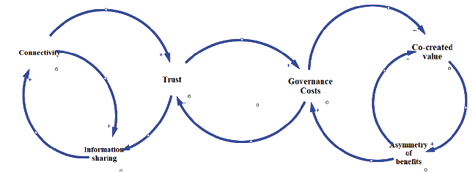

Closer cooperation between bank and non-bank entities leads to greater connectivity between platform participants, complementors, and their customers (market). Figure 1 shows the pattern of behavior mechanisms between different platform participants. It is a conceptual model showing the mutual interactions of various mechanisms within the framework of a typical platform-based model. It shows relations inside platforms between such aspects as connectivity, information sharing and trust, but on the other hand, governance costs, co-created value, and asymmetry of benefits. The platform-based business model is expected to provide greater information symmetry than other structures of business cooperation (Chen et al., 2022; Sironi, 2021). Better connectivity capabilities increase the willingness to share information. If the trust reinforces connectivity, it results in more intensive information sharing and greater efficiency (Chen et al., 2022). Greater connectivity and more significant information sharing results in higher confidence. It is, however, only a theoretical presumption, and it can happen that some participants and complementors strive for exploitation platform interplay to build asymmetrical power for their benefit. The crucial aspect of our research is the right-hand part as shown on Figure 1.

Figure 1. The conceptualization of a pattern of behavior mechanisms emerging amongst platform partners

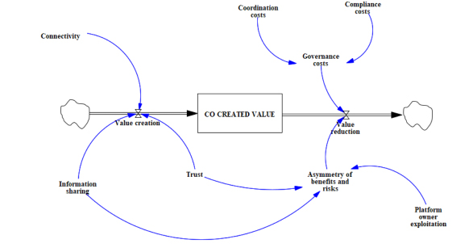

We observe the relations between governance costs, co-created value and the asymmetry of benefits. When governance costs increase, it results in practices that can reduce co-created value. Costs of coordination and compliance lessen the co-created value. A decrease in co-created value can result in practices that increase the asymmetry of benefits and risks, as the complementors need to invest in new capabilities to be compliant. Growing asymmetry of benefits and risks can only reduce the co-created value as complementors’ willingness to participate in a platform declines. If the asymmetry of benefits increases, it can result in the growth of governance costs because of less willingness of complementors to be platform partners, resulting in opportunistic behaviors. These practices can reduce trust, resulting in a lower willingness for information sharing. Connectivity (the technological infrastructure for conveying information) and the desire for information sharing are positively correlated. Better connectivity capabilities increase the willingness for information sharing. If trust reinforces connectivity, it results in greater levels of information sharing. Extended connectivity capabilities, strengthened with greater information sharing, result in higher confidence. However, a reinforcing path is unfolding only until complementors realize that platform owners strive for exploitation of platform interplay to build asymmetrical power for their benefit. The causal loop diagram (Figure 1) was converted into a stock and flow diagram (Figure 2) to better represent the dynamics of a system involving co-created value. This transformation aimed to provide a clearer representation of the interactions and relationships between various elements in the system. In this stock and flow diagram, the central stock is co-created value, which represents the overall value generated through the collaboration of various stakeholders within the system. The stock is influenced by two primary flows: ‘value creation’ and ‘value reduction.’

Figure 2. The conceptual model of value co-creation

According to Figure 2, the value creation process involves stakeholders in the system collectively contributing to the overall co-created value. This process is influenced by several factors, including:

- connectivity (the degree of interaction and communication among stakeholders, which enables value creation);

- information sharing (the sharing of knowledge and resources between stakeholders, facilitating collaborative efforts and value generation);

- trust (the presence of confidence and reliability among stakeholders, promoting a collaborative atmosphere for value creation).

Figure 2 shows that the process can also be opposite, which means value reduction. Value reduction signifies a decrease in co-created value resulting from various costs and negative influences within the system. The following factors impact the value reduction process:

- governance costs (expenses related to managing and coordinating the system, which can diminish overall value);

- coordination costs (costs associated with organizing and aligning stakeholders’ efforts to achieve common objectives, leading to a decrease in co-created value);

- compliance costs (expenses incurred in adhering to regulations and policies, potentially reducing the total value generated within the system);

- platform owner exploitation (instances where a platform owner leverages its position or stakeholders for personal gain, causing a reduction in co-created value).

By converting the causal loop diagram into a stock and flow diagram, we can more effectively comprehend and analyze the intricate interactions between various factors and their impact on co-created value. This improved understanding enables more informed decision-making and system optimization.

Practices sensitive to governance costs affect trust amongst platform partners. Complementors and platform customers show less confidence in platform owners when governance costs rise. If gains in co-created value are weighed against governance costs, the desirability of different co-creation modes can be better assessed. If a platform owner increases the number of connected partners in its network and governance costs can decrease, it can increase trust, which will result in lower relative governance costs. The central idea behind co-created value is that the platform owner and the complementor combine complementary resources in a process that aims at creating value for their joint clients. Variations in governance practices affect co-created value because different approaches entail differences in resource access (Huber et al., 2017).

The conceptual model allows for analyse of the behavior of individual participants of platforms. Despite the numerous benefits that digital platforms create in banking services, some negative aspects stem from tensions among partners. These tensions are different in the case of blockchain-based platforms and cloud-based platforms. It also should be noted that both platforms are being applied to different banking services, meaning that there are different complementors and markets (customers) (Pedersen, 2020). Whereas blockchain-based platforms are suitable for such services as settlement or payment, cloud-based platforms are typical to work with data processing (e.g., regulatory reporting, building new capabilities, etc.). Concerning our conceptual model of a pattern of behavior mechanisms (Figure 1), we elaborated a theoretical decomposition of the tensions between participants of the banking services in both types, namely, blockchain-based and cloud-based platforms.

Blockchain-based platforms

Blockchain enables decentralized decision-making as a governance framework (Wang et al., 2019). The code defines governance rules implemented within smart contracts and executed automatically, minimizing the governance costs (Vella & Gastaldi, 2021). Deployment of smart contracts enables automating most of the work performed by humans, often without consistency, solid logic, and compliance with formally made agreements. Smart contracts replace human decisions with a selection of simple and infallible algorithms that promote the best interests of platform partners. The smart contract permits more disciplined and automated execution of operations (Oliva et al., 2020), reducing reliance on ad-hoc decisions of humans. Another feature of blockchain-based platforms is the transparency of accomplished transactions. Transparency of executed actions provides the same data version for all the platform partners. A decentralized and automated decision-making process reduces information asymmetry and increases trust (Wang et al., 2019; Zavolokina et al., 2020). Connectivity capabilities ensure cryptographically created confidence that contributes to improving information sharing. Blockchain technology enables the machine-to-machine connection, reducing governance costs and offsets human-to-human trust. All participants are equal, and the consensus mechanism is not based on any central regulator.

According to our analysis, blockchain-based platforms offer a higher number of significant advantages to all participants (platform owners, complementors and markets). Offering the automated execution of operations, they provide greater connectivity, information sharing and trust, as well as reducing costs related to opportunism and uncertainty. Blockchain technologies are treated as safer than cloud-based solutions. However, greater safety and higher convenience trigger some costs in the early stages of platform development. Building platforms on the blockchain requires the necessary technological solutions and the newest skills to implement in any technology area. Other kinds of costs, especially coordination costs, grow in the open community (Pereira et al., 2019). Blockchain-based platforms are characterized by a very high coordination threshold for core changes, including social and technical processes, to ensure any changes are secure and widely supported by the community. Such entry raises costs of coordination and costs of creating a new structure.

In the long term, the costs of blockchain platforms are lower, which expands the co-created value. Co-created value embraces the positive consequences for both the platform owners and its partners (complementors). The cooperation provides also greater transparency in ownership records while permitting real-time observation of transfers of shares from one owner to another (Yermack, 2017). The benefits offered by the blockchain platforms are asymmetrical for different participants. Higher governance costs reduce the co-created value and thus create an asymmetry of benefits between the platform owner and its complementors. From the platform owners’ perspective, applying blockchain technology (application of smart contracts) mitigates the risk and reduces the need for intermediaries (financial institutions as complementors). Lower costs of trading and settlement and higher transparency of the transactions create lower benefits for complementors than for platform owners.

Cloud-based platforms

Cloud-based banking refers to deploying banking infrastructure to control cloud-based core banking operations and financial services without dedicated physical servers. One of the cloud-based platforms’ main goals is to enable banking businesses with new tools and techniques. Such platforms host critical applications required for every bank operation. Cloud technology can be implemented in banking on different levels: process, application, platform and infrastructure. The platform (Platforms-as-a-Service, PaaS) offers a cloud-based core banking platform for applications and database development (Malyshev, 2021). In such a solution, the provider (owner) usually delivers a computing platform accessed via web browsers, the operating provider provides a system programming language execution environment, and web servers (Nedelcu et al., 2015). In a private platform, the platform provider can be a bank, whereas in a public platform, it is usually a third-party provider (Hon & Millard, 2018).

One of the advantages of cloud platforms is greater security. Usually, banks use many solutions to their core processes, which need to provide more internet and mobile access to customers. Such solutions are exposed to cyber threats, whereas cloud platforms can offer the same services (processes) in a more secure way (Blazheski, 2016). Moreover, cloud-based technologies provide a platform for application development and cost reduction, and help banks reach out to their customers more effectively. Banking services can be more customer-centric. Cloud and PaaS offer overwhelming financial and technological benefits for customers versus outdated, traditional on-premise technology, as it shifts the cost to build, maintain and sell the software from the customers to vendors and their investors, who finance this in the PaaS scenario by collecting relatively small periodical subscription fees to cover these costs. There are no limits for activities situated in different locations to access banking systems, and the costs of this access are very low. Cloud computing can scale on demand without processing intensive, expensive infrastructure (Awadallah, 2016). A strict connection exists between the platform, platform technology and its management (platform owners). Cloud platforms link former competitors, which raises protection costs for these participants (technological aspects, regulatory requirements, etc.). As a consequence of these changes, the co-created value is lower. On the other hand, a data structure in a cloud platform is unique, and while it can be retrieved, it cannot be simply re-used with a competitive solution. It means that the platform participants are safer, and there is a greater willingness for information sharing and greater connectivity. Undoubtedly, the connectivity in cloud-based platforms is greater than the connectivity between blockchain-based platforms.

Despite the advantages of cloud-based banking platforms, there are also some negative dimensions. Among such negative aspects should be enumerated costs, especially as technical costs might be included, which embrace the adoption of new technologies and configuration of the incumbent solutions. Also, during the use of cloud platforms, technical skills are needed, which causes additional costs (Mahalle te al., 2021). The other challenges of cloud-based platforms embrace the costs of stronger financial regulations and security (data security), difficulties related to the data migration to the cloud-based infrastructure, possible human errors (humans prepare cloud coding), and some other unpredictable circumstances. There can also be a concern that the platform owners have control over data accuracy and privacy. Counterarguments are that today, cloud providers are better equipped against security threats than most of the other solutions (Blazheski, 2016; Pugliese, 2020). Software providers also provide security that can certify any platform behavior that could potentially misuse customers’ data.

DISCUSSION AND CONTRIBUTION TO THEORIZING

Following the aims of our paper, we identified the two most common platforms in banking services, which are blockchain-based and cloud-based platforms. Subsequently, we identified the main participants of digital banking platforms and described the governance processes within the platform-based structures. In the next step, we elaborated the theoretical framework, which presents the dynamic pattern of behavior among partners stemming from the tensions between governance costs and co-created value within platforms in banking services. According to our expectations, this is an important contribution to the extant literature related to the problems of platformization of banking services.

So far, scholars have conducted little research to understand and analyze heterogeneous complementors and customers in the platform ecosystem. Nevertheless, it can be assumed that high power asymmetries can arise in the relationship between complementor and platform owner. In particular, tensions in pricing and the provision structure between platform owner and complementor illustrate the asymmetries in the negotiating power between the platform owner and complementor. The imbalances and power asymmetries entail the risk of a loss of trust between a platform owner and complementor (Deilen & Wiesche, 2021). Platform owners can strengthen trust between complementors, especially through effective governance mechanisms such as intellectual rights protection. This is important, because trust is a significant factor in the relationship between the platform owner and complementor for the platform’s long-term success. A fair and sustainable governance structure has a significant positive impact on the motivation of complementors to engage on the platform (Deilen & Wiesche, 2021).

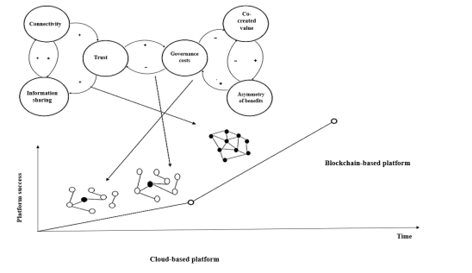

The mechanisms described in our theoretical concept of behavior lead to the main conclusion that the degree of connection between the platform participants depends on the platform type. The blockchain-based platforms lead to greater interconnectedness of platform participants, whereas cloud-based platform participants are less interconnected (Figure 3). Among the factors that increase the coherence of platforms are lower costs, higher simplicity of transactions, and a greater number of transactions. These features characterize blockchain-based platforms. According to our conception, the platform participants are more interconnected in such types of platforms. The other type, cloud-based platform, is characterized by the lower interconnectedness of platform participants. Higher costs of data protection and technology implementation (such platforms usually link different technologies like AI, Big Data, and cloud technology), together with lower numbers of partners, lower transactions and co-created value, and greater asymmetry of benefits, lead to lower coherence of platform participants.

Figure 3. The types of platforms stem from the patterns of behaviors

of platform partners

Though vastly improved from earlier generations, current methods for clearing and settling transactions remain costly with many reconciliations and counterparty risks. Furthermore, many financial products have high transaction costs, and financial inclusion is uneven in many parts of the world (Chen et al., 2022). In particular, the duplicative and time-consuming post-trade processes that banks, brokerages, custodians, and clearing houses undertake to reconcile multiple ledgers represent a huge cost of trust embedded in the existing system. Blockchain technology offers a solution for some of these problems. Though there is a need to carefully explore and consider how the adoption of blockchain technologies and DLTs will affect financial stability, it is also worth exploring how these technologies, less reliant on centralized institutions, might help build a more resilient financial sector.

Apart from clearing and settlement, which is typical in banking activity, numerous transactions are accomplished in the performed bank’s back-office. Among others, here belong the accounting and reporting processes as well as data collection and analytics. Such activities can be accomplished much more efficiently when artificial intelligence and Big Data technologies can be offered as a part of the cloud service. The application of these technologies in a separate way can be much more difficult and costly than as a part of the cloud platform. The main challenge is the decision of what kind of platform, private, public, or hybrid one, should be implemented.

Our research enables us to provide answers to our research questions.

RQ1) What are the specific types of digital platforms in banking services?

The literature has highlighted that Banking as a Platform (BaaP) has become a new model of banking services (Zachariadis & Ozcan, 2017). Digital platforms are leading to a greater openness of banking services and are creating banking ecosystems (Jackson, 2017; Nicoletti et al., 2017; Omarini, 2018). Different types of banking platforms are presented in the extant literature. For example, Sironi (2021) highlights the division into 1) development platforms, 2) transaction platforms, and 3) hybrid platforms. We narrowed the analysis to two types of platforms (blockchain and cloud) and their impact on banking services. In this context we highlighted that blockchain-based and cloud-based platforms are currently the main platforms in banking services.

RQ2) Who are the partners (owners, complementors, customers) of digital

platforms in banking services, and what are their roles?

Platformization is a process triggered by the cooperation between the incumbent institutions and new entrants to the industry (FinTech companies). Khanagha et al. (Khanagha et al., 2022) argue that platforms are sometimes created as a response by incumbent companies to competitors entering the market. According to this approach, platforms are created by banks. In our opinion the reality is more complex. Different types of platforms can be enumerated different roles: platform integrator, platform provider, platform specialist or platform orchestrator (Diamond et al., 2019). Incumbent banks can be both owners and complementors of a platform. They share the roles with other financial and non-financial institutions (FinTech start-ups). The third group of participants is customers of the banking services offered via platforms. We want to highlight that blockchain technology enables greater interdependence of the participants and leads to greater unification of costs and benefits for their participants. Our analysis confirms the suggestion from other research (Pereira et al., 2019) that blockchain-based platforms offer more advantages to customers than other types of platforms in the banking industry.

RQ3) What is the dynamic pattern of behavior among partners stemming from

the tensions between governance costs and co-created value within

platforms in banking services?

The findings develop the conclusions of Huber et al. (2017) regarding tensions between co-created value and governance practices. The process model identifies the self-reinforcing dynamics and necessary conditions that explain how managers can navigate the pressure over time. The prerequisite for platform success is that platform owners should not promise more than they can deliver (Huber et al., 2017). Managers can navigate tensions through acceptance, differentiation, and integration. Through spatial separation, tensions might be addressed by clarifying and segregating individual and corporate levels. Tensions and paradoxes might be resolved through temporal separation by focusing on conflicting goals during different periods. From an integrative perspective, tensions can be resolved by transforming into a more manageable situation, for example, by adding new strategic elements to link oppositional demands. Such a synthesis can also occur on spatial or temporal levels. Identifying creative synergies between contradictory elements is a synthesis that can also occur on spatial or temporal levels. Blockchain-based platforms, as such, provide synergy opportunities for time and space integration.

Conclusion

Our research is focused on the blockchain-based and cloud-based platforms as the most significant types of platforms in the banking industry’s digital transformation. Platformization is a crucial step leading to the creation of new financial ecosystems and the building of a new potential of hybrid cooperation between different market players. We identified the main participants of these platforms and described the governance processes within their structures. Our analysis showed that blockchain-based platforms lead to greater interconnectedness of platform participants, while cloud-based platform participants are less interconnected. The coherence of platforms is influenced by factors such as costs, simplicity of transactions, and the number of transactions. We highlighted that blockchain-based and cloud-based platforms play a significant role in the transformation of the current banking services, but there are still many areas that should be considered for further research, and challenges remain to be resolved to inform about the implication of the platformization of banking services.

From a paradox theory perspective, our research highlights the dynamic pattern of behavior among platform partners, demonstrating that the degree of connection between platform participants depends on the platform type. Tensions between governance costs and co-created value play a crucial role in shaping the interactions among platform participants. Trust is a significant factor in the relationship between the platform owner and complementor for the platform’s long-term success. To manage these tensions, managers can adopt strategies such as acceptance, differentiation, integration, and the identification of creative synergies between contradictory elements.

The critical research problem was to answer the question of whether the use of financial technologies within platforms and the creation of digital platforms lead to the opening or closing of access to these platforms. We also investigated what the conditions for the democratization of platforms (participation of various entities on equal terms) are. In our opinion, blockchain technology provides much greater openness and democratization than cloud technology. Addressing our research questions, we identified blockchain-based and cloud-based platforms as the specific types of digital platforms in banking services, and found that platform partners in banking services include incumbent institutions, FinTech companies, and customers. The roles of these partners vary depending on the platform type, with incumbent banks potentially acting as both owners and complementors. We established that the dynamic behavior pattern among partners in banking services platforms stems from tensions between governance costs and co-created value.

Our findings have important implications for banking institutions and FinTech companies, as the choice of platform type affects their interconnectedness and the distribution of costs and benefits among participants. Blockchain-based platforms offer greater interconnectedness, security, and simplicity of transactions compared to cloud-based platforms, while cloud-based platforms face data protection and technology implementation challenges.

Apart from the abovementioned, we also examined the tensions within the described platforms (between co-created value and governance costs) and answered the question of what to do to remove the indicated problems (practices) in the future. There are different tensions in the platform structure (e.g., cooperation vs. competition, control vs. autonomy, short-term value vs. long-term value creation, stability vs. generativity, etc.). In this context, further research questions arise relating to what should be done to implement the proposed solutions. Among such propositions should be considered the areas related to 1) value realization from platforms and tensions management, 2) development of successful blockchain and cloud-based platforms, 3) relationships amongst platform partners, 4) practice variations in platforms. All of these areas allow us to pose in the future a number of further research questions related to platformization of banking services.

However, our study has limitations, such as focusing on only two types of platforms and not considering other potential platform types in the banking industry. The generalizability of our findings may be limited as a result. Future research could explore the dynamics of other platform types in banking services, investigate the long-term impact of platform choice on banking institutions’ performance, and assess the implications of the platformization of banking services on financial stability and inclusion.

The provided conceptual framework is the first approach to the explanation on how the different platform types can enhance the provision of different banking services. Our attention, however, was not focused on the service provider–customer relations, but on the governance mechanisms inside the platform. We argue that different types of applied technology lead to different solutions and they are more suitable for different types of services. Apart from searching for theoretical problem solving, empirical research is needed in this area. We hope that our research will be continued in other studies devoted to the creation of banking ecosystems and implementation of platform-based solutions.

Acknowledgments

The publication has been supported by a grant from the Faculty of Management and Social Communication under the Strategic Programme Excellence Initiative at Jagiellonian University.

References

Abendroth, J., Riefle, L., & Benz, C. (2021). Opening the black box of digital B2B co-creation platforms: A taxonomy. In F. Ahlemann, R. Schutte, & S. Stieglitz (Eds.), Innovation Through Information Systems (pp. 596-611). Cham: Springer International Publishing.

Adner, R. (2017). Ecosystem as structure: An actionable construct for strategy. Journal of Management, 43(1), 39–58. https://doi.org/10.1177/0149206316678451

Arslanian, H., & Fischer, F. (2019). Fintech and the future of the financial ecosystem. In H. Arslanian, & F. Fischer (Eds.), The Future of Finance: The Impact of FinTech, AI, and Crypto on Financial Services (pp. 201-216). Cham: Springer International Publishing.

Avarmaa, M., Torkkeli, L., Laidroo, L., & Koroleva, E. (2022). The interplay of entrepreneurial ecosystem actors and conditions in FinTech ecosystems: An empirical analysis. Journal of Entrepreneurship, Management and Innovation, 18(4), 79-113. https://doi.org/10.7341/20221843

Awadallah, N. (2016). Usage of cloud computing in banking system. International Journal of Computer Science Issues, 13(1), 49-52. https://doi.org/10.20943/IJCSI-201602-4952

Baldwin, C.Y., & Woodard, C.J. (2008). The architecture of platforms: A unified view. Harvard Business School Finance Working Paper No. 09-034, Harvard Business School, Boston. Retrieved from http://dx.doi.org/10.2139/ssrn.1265155

Bartolacci, F., Cardoni, A., Łasak, P., & Sadkowski, W. (2022). An analytical framework for strategic alliance formation between a cooperative bank and a fintech start-up: An Italian case study. Journal of Entrepreneurship, Management and Innovation, 18(4), 115-156. https://doi.org/10.7341/20221844

Bhutto, S. A., Jamal, Y., & Ullah, S. (2023). FinTech adoption, HR competency potential, service innovation and firm growth in banking sector. Heliyon, 9(3), 1-13. https://doi.org/10.1016/j.heliyon.2023.e13967

Bilan, A., Degryse, H., O’Flynn, K., & Ongena, S. (Eds.). (2019). Banking and Financial Markets: How Banks and Financial Technology Are Reshaping Financial Markets. 1st ed. 2019 edition. Cham: Palgrave Macmillan.

Blazheski, F. (2016). Cloud banking or banking in the clouds? BBVA Research 1. Retrieved from https://www.bbvaresearch.com/wp-content/uploads/2016/04/Cloud_Banking_or_Banking_in_the_Clouds1.pdf

Boot, A., Hoffmann, P., Laeven, L., & Ratnovski, L. (2021). Fintech: What’s old, what’s new? Journal of Financial Stability, 53(100836), 1-36. https://doi.org/10.1016/j.jfs.2020.100836

Brandon-Jones, E., Squire, B., Autry, Ch. W., & Petersen, K. J. (2014). A contingent resource-based perspective of supply chain resilience and robustness. Journal of Supply Chain Management, 50(3), 55–73. https://doi.org/10.1111/jscm.12050

Caron, F. (2018). The evolving payments landscape: Technological innovation in payment systems. It Professional, 20(2), 53–61. https://doi.org/10.1109/MITP.2018.021921651

Chen, S., D’Silva, D., Packer, F., & Tiwari, S. (2022). Virtual banking and beyond. BIS Papers, 120, 1-37. Retrieved from https://www.bis.org/publ/bppdf/bispap120.pdf

Claessens, S., Frost, J., Turner, G., & Zhu, F. (2018). Fintech credit markets around the world: Size, drivers and policy issues. BIS Quarterly Review, September, 1-21. Retrieved from https://www.bis.org/publ/qtrpdf/r_qt1809e.pdf

Clarke, Ch. (2019). Platform lending and the politics of financial infrastructures. Review of International Political Economy, 26(5), 863–885. https://doi.org/10.1080/09692290.2019.1616598

Croxson, K., Frost, J., Gambacorta, L., & Valletti, T. (2021). Platform-based business models and financial inclusion. BIS Working Papers, 986, 1-30. Retrieved from https://www.bis.org/publ/work986.pdf

Dattée, B., Alexy, O., & Autio, E. (2018). Maneuvering in poor visibility: How firms play the ecosystem game when uncertainty is high. Academy of Management Journal, 61(2), 466–498. https://doi.org/10.5465/amj.2015.0869

De Reuver, M., Sørensen, C., & Basole, R.C. (2018). The digital platform: A research agenda. Journal of Information Technology, 33(2), 124–135. https://doi.org/10.1057/s41265-016-0033-3

Deilen, M., & Wiesche, M. (2021). The role of complementors in platform ecosystems. In F. Ahlemann, R., Schütte, & S. Stieglitz (Eds.), Innovation Through Information Systems (pp. 473-488). WI 2021. Lecture Notes in Information Systems and Organisation. Cham: Springer International Publishing. https://doi.org/10.1007/978-3-030-86800-0_33

Diamond, S., Drury, N., Lipp, A., Marshall, A., Ramamurthy, S., & Wagle, L. (2019). The future of banking in the platform economy. Strategy & Leadership, 47(6), 34-42. https://doi.org/10.1108/SL-09-2019-0139

Eaton, B., Elaluf-Calderwood, S., Sørensen, S., & Yoo, Y. (2015). Distributed tuning of boundary resources. MIS Quarterly, 39(1), 217–244. Retrieved from http://eprints.lse.ac.uk/63272/

Eisenmann, T.R. (2008). Managing proprietary and shared platforms. California Management Review, 50(4), 31–53. https://doi.org/10.2307/41166455

European Banking Authority. (2021). Report on the use of digital platforms in the EU banking and payment sector. EBA/REP/2021/26. European Banking Authority, Paris. Retrieved from https://www.eba.europa.eu/sites/default/documents/files/document_library/Publications/Reports/2021/1019865/EBA%20Digital%20platforms%20report%20-%20210921.pdf

Farrow, G.S.D. (2020). Open banking: The rise of the cloud platform. Journal of Payments Strategy & Systems, 14(2), 128–146.

Finken, S., & Finkemeyer, D. (2019). The impact of blockchain on the transaction banking business model. Journal of Digital Banking, 4(1), 19–34.

Freichel, Ch., Fieger, J., & Winkelmann, A. (2021). Developing a taxonomy for digital platforms – A conceptual approach. In Proceedings of the 54th Hawaii International Conference on System Sciences (pp. 5779-5788). Retrieved from http://hdl.handle.net/10125/71321

Gancarczyk, M., & Rodil-Marzábal, O. (2022). Fintech framing ecologies: Conceptual and policy-related implications. Journal of Entrepreneurship, Management and Innovation, 18(4), 7-44. https://doi.org/10.7341/20221841

Glassburner, A. V., Nowicki, D.R., Sauser, B., Randall, W.S., & Dickens, J.M. (2018). Theory of paradox within service-dominant logic. Service Science, 10(2), 111–123. https://doi.org/10.1287/serv.2018.0206

Gozman, D., Hedman, J., & Olsen, K.S. (2018). Open banking: Emergent roles, risks & opportunities. In ECIS 2018 Proceedings Association for Information Systems. AIS Electronic Library (AISeL). Retrieved from https://research.cbs.dk/en/publications/open-banking-emergent-roles-risks-amp-opportunities

Hedman, J., & Henningsson, S. (2015). The new normal: Market cooperation in the mobile payments ecosystem. Electronic Commerce Research and Applications, 14(5), 305–318. https://doi.org/10.1016/j.elerap.2015.03.005

Hein, A., Schreieck, M., Riasanow, T., Setzke, D.S., Wiesche, W., Böhm, M., & Krcmar, H. (2020). Digital platform ecosystems. Electronic Markets, 30(1), 87–98. https://doi.org/10.1007/s12525-019-00377-4

Hermes, S., Pfab, S., Hein, A., Weking, J., Böhm, M., & Krcmar, H. (2020). Digital platforms and market dominance: Insights from a systematic literature review and avenues for future research. Pacific Asia Conference on Information Systems 2020 Proceedings. 42. Dubai, UAE. Retrieved from https://aisel.aisnet.org/pacis2020/42

Hon, W.K., & Millard, Ch. (2018). Banking in the cloud: Part 1 – Banks’ use of cloud services. Computer Law & Security Review, 34(1), 4–24. https://doi.org/10.1016/j.clsr.2017.11.005